Table of Contents

Government and sovereign investments quietly shape how money moves around the world. From sovereign wealth funds to sovereign gold bonds, these vehicles help governments stabilize their economies, earn returns, and fund long-term priorities like infrastructure, pensions, and strategic reserves. But alongside the upside, they also carry real risks—from geopolitical shocks to interest-rate swings and volatile markets.

In recent years, their influence has exploded. Sovereign wealth funds (SWFs) alone have become some of the biggest power brokers in global finance. As of mid-2025, more than 100 SWFs collectively manage an estimated $13–14 trillion in assets, up from around $11.6 trillion in 2022, capital that can move markets when it shifts.

This blog breaks down how these investments work, why they matter, and where the fault lines lie. We’ll look at the benefits governments are chasing, the risks they must constantly manage, and the strategies they use to balance stability, returns, and public accountability. Let’s jump in.

What do We Mean By Government and Sovereign Investments?

When people say “government money” or “sovereign capital,” they usually mean one or more of these:

- Government venture funds / schemes

National or state programs that invest directly in startups or VC funds, often to support innovation, jobs, or strategic sectors. - Sovereign Wealth Funds (SWFs)

State-owned investment funds that invest a country’s reserves (often from commodities or FX surpluses) into assets like stocks, bonds, real estate, infrastructure, and private equity. - Development finance institutions & public banks

Government-backed lenders/investors focused on development, infrastructure, and climate or social outcomes.

These investors now control trillions of dollars and are increasingly active in venture, private equity, and direct company stakes. A review of types of investors in startups reveals how distinct investor profiles influence your assessment of risk and benefit in sovereign investments, providing a broader context within the evolving funding landscape.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

What Is Sovereign Gold Bonds (SGBs)?

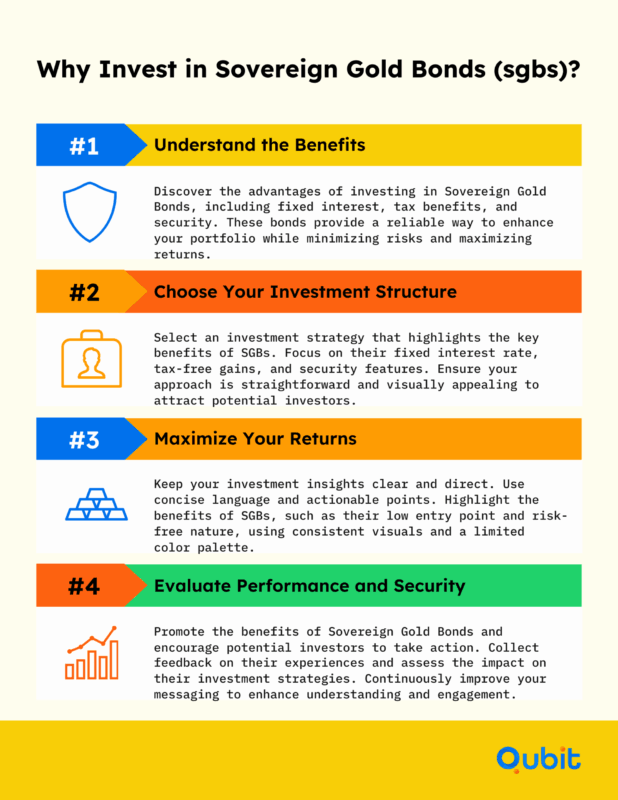

Issued by the Reserve Bank of India (RBI) on behalf of the government, these bonds are denominated in grams of gold. They provide a secure, paper-based alternative to traditional gold investments.

One of the standout features of SGBs is their fixed interest rate of 2.5% per annum, paid semi-annually. This makes them an attractive choice for investors looking for steady returns alongside potential capital appreciation. Additionally, SGBs eliminate the risks and costs associated with storing physical gold, such as theft or storage fees, while still allowing investors to benefit from gold price trends.

Investors can hold SGBs in certificate form or as dematerialized assets (electronic form not requiring paper certificates), making them easy to manage and transfer.

Whether you’re a seasoned investor or new to gold-based assets, Sovereign Gold Bonds provide a reliable and efficient way to tap into the value of gold without the hassle of physical possession.

How Sovereign Gold Bonds Can Benefit You?

Sovereign Gold Bonds (SGBs) offer a unique blend of security, affordability, and strategic advantages for family office relationship management, especially for investors seeking exposure to gold.

One of the standout benefits of SGBs is their fixed annual interest payments, typically around 2.5% per annum, disbursed semi-annually. This feature ensures a steady income stream alongside the potential appreciation of gold prices.

Unlike physical gold, SGBs eliminate storage concerns by being issued in paper or dematerialized formats, providing enhanced security and convenience. This makes them an ideal choice for those who want to invest in gold without the risks associated with theft or damage.

Tax benefits further amplify the appeal of SGBs. Investors enjoy capital gains tax exemptions if the bonds are held until maturity, and there is no Tax Deducted at Source (TDS) on the interest earned. These advantages position SGBs as a tax-efficient investment option for long-term wealth creation.

Additionally, SGBs offer an affordable entry point into gold investments, allowing individuals to diversify their portfolios without the need for large upfront costs. By allocating 10%-20% of your portfolio to gold through SGBs, you can achieve strategic asset allocation that helps stabilize your investments during market volatility.

SGBs are not just an investment in gold, they are a smart, secure, and tax-efficient way to grow your wealth.

What Are the Drawbacks of Sovereign Gold Bonds?

Sovereign Gold Bonds (SGBs) offer a unique investment avenue, but they come with certain limitations that investors should carefully consider. One of the most notable challenges is the extended maturity period of eight years, which can limit flexibility. While early redemption is allowed after five years, the lack of liquidity before full maturity may deter those seeking short-term financial gains.

Another drawback lies in the restricted issuance windows. SGBs are only available during specific periods announced by the government, which can make it difficult for investors to align their purchase with favorable market conditions. This limited availability often leads to missed opportunities for timely investments.

Additionally, the risk of capital loss is a concern. If gold prices fall below the initial purchase price at maturity, investors may face financial setbacks despite the interest earned during the bond’s tenure. This volatility underscores the importance of assessing market trends before committing to SGBs.

For a deeper understanding of regulatory and compliance challenges tied to sovereign investments, explore the discussion on legal issues with sovereign investments.

What Key Terms Should You Know Before Investing in SGBs?

While SGBs have undeniable benefits, these drawbacks highlight the need for a well-rounded investment strategy that accounts for potential risks.

Sovereign Gold Bonds (SGBs) offer a unique opportunity for investors seeking to diversify their portfolios with gold-backed instruments. Before committing to this investment, it’s essential to evaluate several factors to ensure it aligns with your financial goals.

1. Fixed Income Benefits

One of the standout features of SGBs is the fixed annual interest rate, typically around 2.5%. This provides a steady income stream alongside the potential appreciation of gold prices. Unlike physical gold, SGBs eliminate storage costs and risks, making them a more secure option for long-term investors.

2. Tax Advantages

SGBs come with attractive tax benefits. While the interest earned is taxable, the capital gains upon maturity are exempt from tax, offering significant savings for investors. Additionally, early redemption after the fifth year allows partial liquidity while retaining tax exemptions on gains.

3. Liquidity Considerations

Although SGBs can be traded on stock exchanges, their liquidity is often limited compared to other financial instruments. Investors should assess their ability to hold the bonds until maturity, as premature selling may result in lower returns due to market fluctuations.

4. Ideal Investor Profile

SGBs are best suited for individuals with a long-term investment horizon, moderate risk tolerance, and an interest in gold investment strategy. They serve as a hedge against inflation and currency fluctuations, making them a strategic addition to a diversified portfolio.

What Makes Sovereign Wealth Funds So Powerful?

Sovereign wealth funds (SWFs) are among the most influential financial entities in the global economy. These state-owned investment funds are fueled by excess reserves or surpluses from national budgets, often derived from commodities like oil or gas, or trade surpluses. Their ability to channel these resources into diverse asset classes makes them indispensable for countries seeking economic stability and growth.

Understanding their vast impact requires context. In 2024, total assets of investment funds reached a record €50.7 trillion. This scale highlights how institutional investors, including SWFs, shape capital markets and global finance. For governments, such asset totals provide significant leverage and strategic flexibility.

For family office relationship management, understanding how sovereign wealth funds channel resources into diverse asset classes is essential for strategic collaboration.

One of the defining strengths of SWFs lies in their role as stabilizers during economic turbulence. By investing in a broad range of assets, such as equities, bonds, real estate, and even startups, SWFs help nations diversify income sources and reduce reliance on volatile industries. For instance, Kuwait’s KIA, one of the oldest and most prominent SWFs, exemplifies how these funds can safeguard national wealth while pursuing long-term growth strategies.

Beyond economic stabilization, SWFs are pivotal in balancing domestic fiscal policies with global investment strategies. Their ability to act as financial buffers during crises, such as bank rescues or economic downturns, underscores their importance in maintaining national economic health. This intervention capability, often referred to as “SWF intervention,” highlights their strategic value in addressing both immediate and long-term financial challenges.

The rising prominence of SWFs as institutional players is reshaping global financial markets. Their investments not only influence market trends but also open doors for large-scale opportunities, including funding innovative startups. An exploration into startups funded by sovereign wealth funds presents tangible examples of how public investment can translate into effective financial outcomes, complementing your review of associated benefits and challenges.

The Origin and Expansion of Sovereign Wealth Funds

Sovereign wealth funds (SWFs) trace their origins to the mid-20th century, with the Kuwait Investment Authority (KIA) established in 1953 as the first of its kind. Initially created to manage surplus oil revenues, SWFs have undergone remarkable transformation over the decades, expanding their scope and influence in global finance.

From Modest Beginnings to Trillion-Dollar Powerhouses

From their modest beginnings, SWFs have grown exponentially in both number and asset size. Today, these state-sponsored investments collectively manage over $11 trillion in assets, a significant leap from $6.7 trillion in 2014. This growth reflects their increasingly strategic role in stabilizing economies, funding infrastructure, and diversifying national wealth.

Evolution Through Time and Sectoral Shifts

Historical data highlights the pivotal role SWFs have played in shaping global markets. Norway’s Government Pension Fund Global (GPFG), for instance, stands as the largest SWF, managing $1.4 trillion in assets as of 2023. Meanwhile, investment patterns have shifted over time, with SWFs diversifying beyond technology into sectors like finance and energy, adapting to changing market dynamics.

What Is the Difference Between Commodity and Non-Commodity SWFs?

Sovereign Wealth Funds (SWFs) are typically classified based on their revenue sources, shaping their investment strategies and risk profiles. Commodity sovereign funds, for instance, are primarily financed through revenues from natural resources like oil, gas, or minerals. These funds often aim to stabilize economies reliant on volatile resource markets, while also preserving wealth for future generations.

On the other hand, non-commodity sovereign funds derive their capital from foreign exchange surpluses, often accumulated through trade imbalances or currency reserves. Countries with robust export-driven economies, such as China, frequently utilize these funds to diversify their investments globally. For example, China’s Belt & Road Investments have deployed $1.24 trillion to bolster international infrastructure and trade networks.

The distinction between these two types of SWFs significantly impacts their risk tolerance and investment focus. Commodity funds tend to adopt conservative strategies to mitigate resource price fluctuations, whereas non-commodity funds often pursue aggressive growth opportunities in global markets. Understanding these differences is crucial for evaluating how SWFs contribute to economic stability and long-term growth.

By analyzing the revenue sources and strategic priorities of SWFs, investors and policymakers can better assess their role in shaping global financial landscapes.

How Sovereign Wealth Funds Approach Investments

Sovereign Wealth Funds (SWFs) employ diverse strategies to manage their portfolios, reflecting their unique objectives and risk tolerances. These funds typically invest across a broad spectrum of asset classes, including government bonds, equities, and real estate. Such investments provide stability and long-term growth, aligning with the funds’ mandate to preserve wealth for future generations.

In recent years, SWFs have increasingly turned to alternative investments, such as hedge funds and private equity, to enhance returns and diversify risk. These asset classes offer opportunities for higher yields, albeit with greater complexity and risk. The shift toward alternatives highlights the evolving nature of SWF investment strategies, as funds adapt to changing market dynamics and economic conditions.

Investment approaches among SWFs vary significantly. Some funds adopt a passive strategy, focusing on stable, low-risk assets, while others take a more active role, directly managing investments to capitalize on market opportunities. This flexibility enables SWFs to balance their dual objectives of wealth preservation and growth effectively.

Modern investment strategies must consider risk and liquidity. The Liquidity Coverage Ratio (LCR) ensures institutions maintain high-quality liquid assets for 30-day stress periods. This regulatory standard is reshaping portfolio construction and risk readiness across sovereign entities.

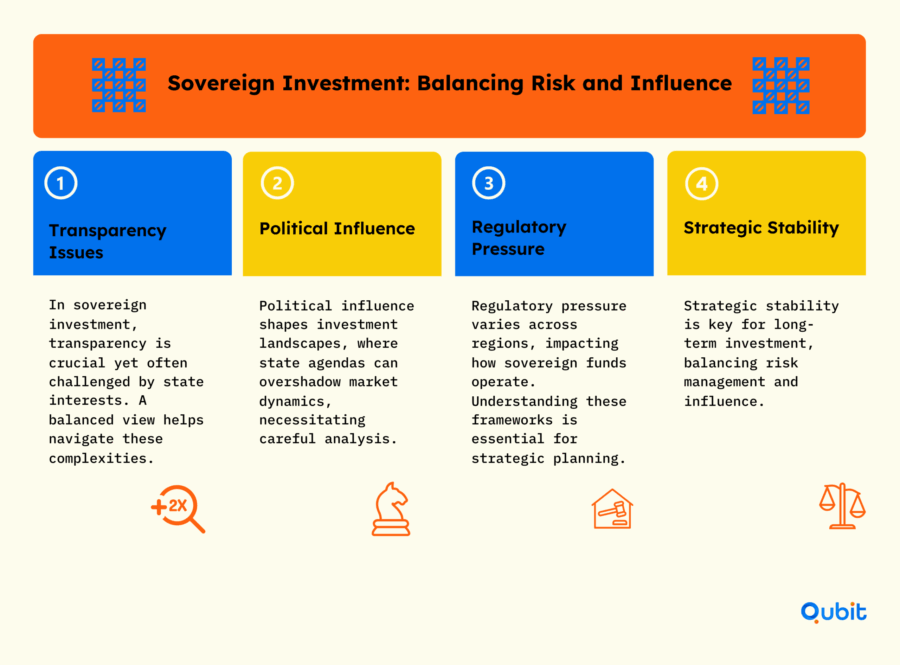

Why Is There a Global Debate Around Sovereign Investments?

Sovereign Wealth Funds (SWFs) have sparked widespread discussion on their role in international markets, particularly regarding transparency, political influence, and regulatory challenges. Family office relationship management is increasingly relevant in navigating these complexities.

Transparency remains a critical issue, as many SWFs are perceived to lack clear reporting standards, raising questions about their objectives and accountability. Political motivations further complicate the conversation, with critics arguing that sovereign investments may prioritize geopolitical interests over market stability. This scrutiny intensifies in cross-border contexts, where regulatory frameworks are under pressure to ensure market integrity without stifling investment opportunities.

For instance, some SWFs are shifting their focus from large technology holdings to more stable financial assets, reflecting a strategic realignment in response to evolving market conditions. This trend underscores the importance of balancing investment transparency with adaptability in global markets.

An analysis of micro vcs and super angels provides a contrasting perspective on early-stage funding alternatives, enriching your comparison with the dynamics of sovereign and government-led investments. As these debates continue to shape market perceptions, understanding the nuances of sovereign investments becomes essential for stakeholders worldwide.

How Are Sovereign Wealth Funds Used?

A big part of their appeal is stability. SWFs are designed as “patient capital”: they don’t usually have short-term liabilities and can keep investing when others panic. During the 2008–09 financial crisis, several SWFs injected equity into Western banks to help steady the system. After the 2022 market rout, they did it again in a different way, instead of retreating, SWFs deployed a record $257.5 billion across 743 deals, with Singapore’s GIC alone spending $39 billion on 72 transactions while many private investors hit pause. That counter-cyclical behaviour is exactly why they’re seen as long-term shock absorbers.

At the same time, sovereign investors are being used as strategic tools. Around a quarter of SWFs now have explicit domestic development mandates, backing sectors tied to national priorities – energy, defense, advanced manufacturing, and climate. In 2023, SWFs invested a record $9.7 billion in “green” sectors across 40 deals, with more than two-thirds of funds now saying they align their portfolios with sustainability goals. From Mubadala and QIA financing clean energy and infrastructure in markets like India, to Singapore’s GIC and Temasek backing high-growth tech globally, sovereign capital is quietly steering the energy transition and innovation agenda.

There are clear success stories. Norway’s Government Pension Fund Global, at about $1.8 trillion in assets, earned a record profit of $222 billion in 2024 and now generates more income than the country’s petroleum sector. Gulf giants like ADIA, QIA, and Saudi Arabia’s PIF have turned oil and gas surpluses into global portfolios worth hundreds of billions (or more than a trillion, in PIF’s case), while also financing mega-projects at home. But there’s a darker side too: scandals like Malaysia’s 1MDB, governance failures at funds such as Kazakhstan’s Samruk-Kazyna, politically driven bailouts, and rising scrutiny from regimes like CFIUS and the EU’s FDI screening system show how quickly sovereign investment can run into geopolitics, misallocation, and controversy.

Conclusion

Government and sovereign investments sit at a powerful but complicated intersection of public policy, capital markets, and innovation. From Sovereign Gold Bonds to trillion-dollar wealth funds, they can stabilize economies, unlock liquidity, and create long-term partnership opportunities for founders, family offices, and institutional investors.

At the same time, long lock-ins, liquidity gaps, governance questions, and political or regulatory risk mean this capital must be approached with intention, not blind optimism. The real advantage goes to investors who understand how these instruments work, how they are regulated, and where they sit alongside private VCs, micro VCs, and super angels in the broader funding stack. Treated thoughtfully, sovereign capital becomes not a shortcut, but a durable pillar of a resilient portfolio.

If you’re looking to develop a compelling pitch deck that effectively communicates the risks and benefits of sovereign investments, we at Qubit can help elevate your strategy. Check out our Fundraising Assistance Services today!

Key Takeaway

Sovereign gold bonds offer fixed interest rates and tax benefits but face liquidity challenges.

Investors must weigh SGB benefits against long maturity periods and potential capital loss.

Sovereign wealth funds diversify national reserves and stabilize economies with varied asset allocations.

Historical trends reveal significant growth and strategic shifts in SWF management.

A balanced analysis of both instruments enables informed, data-driven investment decisions.

Find startups worth your time.

Curated startup opportunities matched to your thesis and investment criteria.

- Deal flow filtered by sector, stage, and fit

- Research and context included with every opportunity

- Less noise. More relevant deal flow.

Frequently asked Questions

How do Sovereign Wealth Funds stabilize national economies?

Sovereign Wealth Funds stabilize economies by investing in diverse assets. This reduces reliance on single revenue streams and cushions against market volatility.