Back

Back

Table of Contents

Starting a business often requires significant capital, and debt financing for startups can be a practical solution to secure the funds needed without giving up equity. However, traditional banks have historically been hesitant to lend to startups, particularly after the 2008 financial crisis. According to Biz Journals, this reluctance has only grown in the post-crisis environment, leading many entrepreneurs to explore alternative financing options.

The demand for funding is immense, with 30.7 million small- and medium-sized enterprises (SMEs) in the U.S. as of 2019, collectively employing nearly 60 million people.

This blog will guide you through various debt financing options, from traditional loans to innovative alternatives. Let’s jump right in!

Understanding Debt Financing and Best Crowdfunding Platforms

Debt financing is a method of raising capital through borrowing. Funds are repaid over time with interest.

For startups, understanding what is debt financing is crucial, as it provides a pathway to growth while maintaining ownership. Historically, challenges in lending practices have shaped the way businesses approach borrowing, emphasizing the importance of selecting the right financing options.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

Comparing Debt, Equity, and the Rise of Venture Debt

Startups face critical decisions when it comes to funding their growth, often navigating the trade-offs between taking on debt, raising equity, or using the best crowdfunding platforms.

Equity financing involves selling ownership stakes in the company. Crowdfunding investing allows startups to attract a broad pool of investors without relying on traditional venture capital.

In recent years, a hybrid solution has emerged: venture debt (a form of loan designed for startups with steady revenue).

Venture debt is reshaping startup fundraising. In 2022, US venture-backed tech firms secured a record $29 billion in this form of financing. This milestone illustrates how venture debt’s popularity surged as traditional VC investment slowed. For founders, this means access to large growth capital without equity dilution.

Ultimately, the choice between debt and equity is about balance: preserving ownership versus managing financial obligations. Understanding this dynamic is crucial for startups aiming to scale efficiently while maintaining strategic control.

Understanding the types of startup funding available is essential for entrepreneurs, especially when considering debt financing as a strategic option.

How Debt Financing Works: Mechanics and Repayment Structures

Debt financing operates through a structured process involving the principal amount borrowed, interest rates, and repayment terms. At its core, the borrower agrees to repay the lender over a specified period, with interest serving as the cost of borrowing. The debt financing def lies in its ability to provide businesses with immediate capital without diluting ownership.

Interest rates, a critical component, are influenced by factors such as the borrower’s creditworthiness and broader macroeconomic conditions. For instance, insights from the Federal Reserve highlight how central bank policies and economic trends impact borrowing costs. A company with strong financial health and a high credit score typically secures lower interest rates, while startups or businesses with limited credit history may face higher costs.

Repayment structures vary widely. Some lenders offer flexible terms, while others require fixed monthly payments. For SaaS companies, financing amounts often correlate with their Monthly Recurring Revenue (MRR; the consistent income a SaaS company makes each month). MRR is the steady income generated monthly from subscriptions. Lenders may offer loans 3-5 times the startup’s MRR, enabling predictable repayments.

Understanding these mechanics is essential for businesses aiming to optimize their funding strategies. By evaluating creditworthiness and staying informed about economic trends, companies can secure favorable terms and manage repayment effectively.

Exploring Debt Financing and Best Crowdfunding Platforms for Startups

Finding the right funding solution is a critical step for startups aiming to scale their operations. In addition to debt financing, the best crowdfunding platforms provide startups with alternative ways to raise capital.

Among alternative debt options, revenue-based financing is gaining momentum. By 2027, the revenue-based financing market is projected to reach $42.35 billion. This expansion reflects startups’ increasing preference for flexible repayment structures. Founders should monitor this trend when evaluating modern financing avenues.

- Evaluate credit score

- Choose lender type

- Compare repayment terms

- Review collateral requirements

Alternative lenders and the best crowdfunding platforms have emerged, offering more flexible terms and faster approval processes.

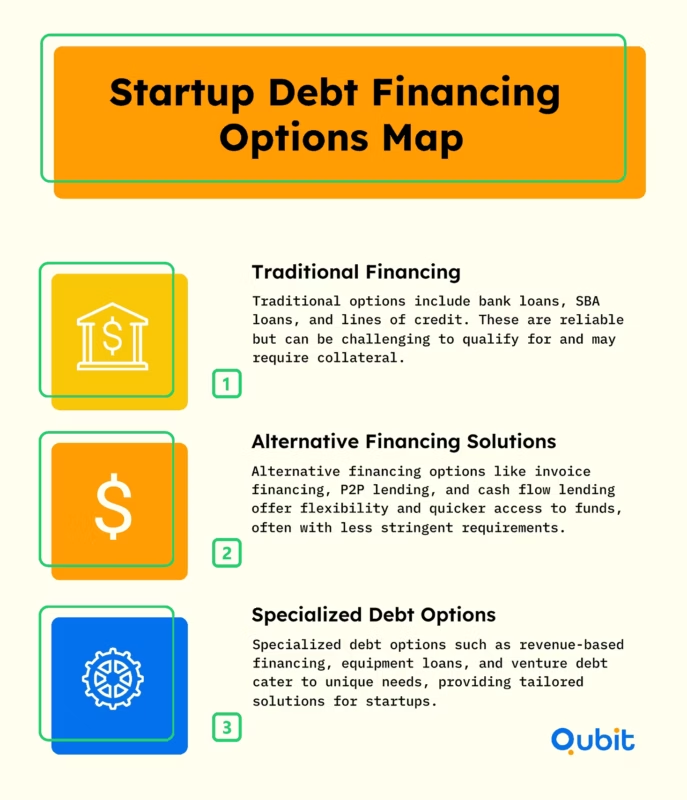

Alternative Financing Models

- Cash Flow Lending

Startups without substantial collateral can explore cash flow lending. This model evaluates a business’s cash flow rather than its assets to determine loan eligibility. - Peer-to-Peer (P2P) Lending

Emerging platforms for Peer-to-Peer (P2P) lending offer startups a direct way to secure funding from individual investors. This method is often faster and less restrictive than traditional loans. - Invoice Financing

Invoice financing allows startups to unlock working capital tied up in unpaid invoices. Typically, this method advances 70–95% of the invoice value, providing immediate liquidity to cover operational costs.

If a payment is missed, lenders may impose penalties or call in the entire loan. Early-stage startups should model worst-case cash flow to avoid surprises.

Debt-Based Crowdfunding for Startup Financing

Building on alternative financing models, debt-based crowdfunding enables startups to raise capital directly from individual lenders online. This approach bypasses traditional banks, allowing founders to access funds through platforms that pool small loans from many backers. Debt crowdfunding typically involves fixed repayment terms and interest rates, with platforms facilitating loan agreements and payments. For startups, this model can provide flexible funding and broaden access to investors, especially when conventional lending is unavailable.

Choosing the Right Debt Crowdfunding Platform

- Evaluate platform reputation and transparency to ensure lender protection and reliable fund disbursement for your campaign.

- Compare platform fees, repayment terms, and eligibility criteria to match your startup’s financial requirements and capacity.

- Assess platform community size and engagement tools to maximize campaign visibility and attract diverse backers.

Crowdfunding for Startups: A Flexible Alternative

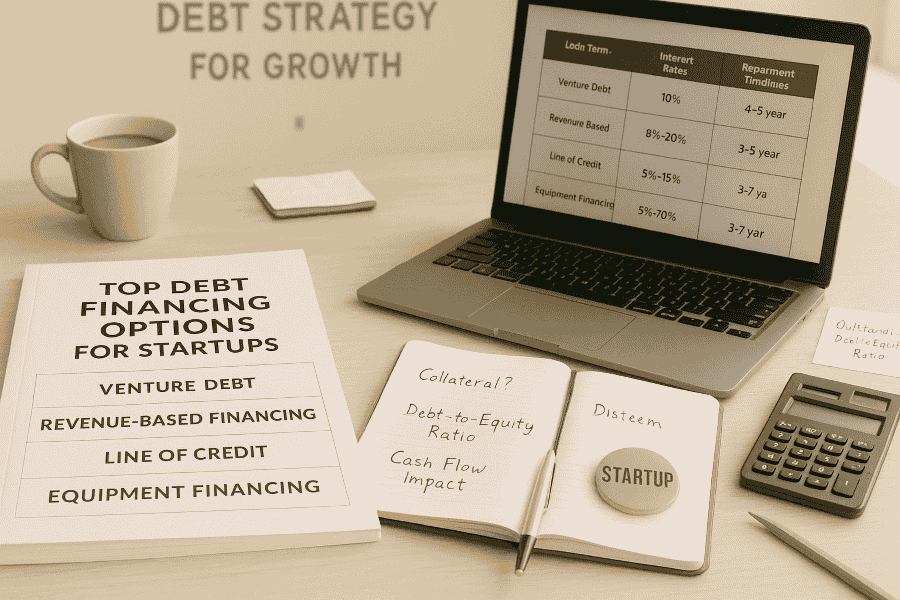

Specialized Debt Financing Options

- Revenue-Based Financing

Revenue-based financing ties repayments to a percentage of monthly revenue, making it a flexible option for startups with fluctuating income. This model ensures that repayments align with the business’s performance, reducing financial strain during slower months. - Equipment Financing

Startups requiring significant capital for machinery or tools can consider equipment financing. Here, the purchased equipment itself serves as collateral, simplifying the qualification process.

For founders exploring advanced strategies, convertible debt vs SAFE notes (Simple Agreement for Future Equity; a form of startup financing) offer flexibility.

However, the fixed repayment terms associated with debt financing can strain cash flow, especially for startups in their early stages. Missing a repayment can lead to penalties or damage to creditworthiness, making it a high-stakes decision.

To illustrate, CoreWeave, an AI cloud infrastructure company, secured a $7.5 billion debt financing facility in May 2024. This substantial funding, led by Blackstone and Magnetar, was aimed at expanding their high-performance computing capabilities to meet the growing demand for AI infrastructure.

Similarly, Stripe, a leading fintech company, raised $600 million in a funding round in March 2021, achieving a $95 billion valuation. This capital was intended to support their European expansion and reinforce their enterprise leadership, demonstrating how strategic financing can fuel growth while maintaining control.

Striking the right balance between debt and equity is essential for sustainable growth. As highlighted in our article on balancing equity and debt financing, startups must carefully assess their financial strategies to avoid over-leveraging or losing control.

By understanding both the benefits and risks, startups can make informed decisions about whether debt financing aligns with their long-term goals.

Navigating the Debt Financing Application Process and Interest Rates

Securing debt financing means understanding the steps involved and preparing thoroughly to meet lender expectations. Start by organizing detailed financial statements, including balance sheets, income statements, and cash flow projections. These documents provide lenders with a clear picture of your business's financial health and repayment capacity.

Next, familiarize yourself with the criteria lenders use to evaluate applications. This often includes credit scores, debt-to-income ratios, and business performance metrics. Knowing these benchmarks helps you identify areas to strengthen before applying.

Alternatively, crowdfunding for startups can provide funding without the need for complex applications. Interest rates play a crucial role in determining the affordability of a loan. To assess feasible ranges, use resources like Loan Rates, which provide benchmark data on average small business loan interest rates. Comparing these trends ensures you’re not overpaying for financing and helps you negotiate better terms.

Preparation and research are key to securing favorable debt financing. By aligning your financial profile with lender expectations and understanding market interest rates, you can position your business for success.

Conclusion

Understanding the diverse landscape of debt financing and crowdfunding investing is essential for startups aiming to scale effectively. Throughout this blog, we’ve explored key strategies, from traditional loans to innovative funding options, emphasizing the importance of tailoring financial solutions to your business needs. Preparing comprehensive financial documentation and evaluating various funding avenues can significantly enhance your chances of securing the right support.

If you’re ready to take the next step in identifying investors or exploring the best crowdfunding platforms for your startup, we’re here to help. At Qubit Capital, our Investor Discovery and Mapping service is designed to connect you with the right opportunities. Let’s get started on building a stronger financial foundation for your startup’s success.

Key Takeaway

Debt financing offers startups a non-dilutive funding option with potential tax benefits.

- The best crowdfunding platforms also provide flexible funding without equity dilution.

A range of options exist, from traditional bank loans to alternative and specialized financing models.

Venture debt has emerged as a critical tool for later-stage startups, fueling significant growth.

Understanding repayment structures and key terminology is essential for effective debt management.

Proper financial preparation is crucial for successfully securing debt financing.

Need numbers investors trust?

Clean assumptions, realistic projections, and a structure that holds up in diligence.

- Forecasts, unit economics, and scenario planning

- Valuation-ready outputs investors can review fast

- Clear structure so you can update it easily

Frequently asked Questions

What are the best crowdfunding platforms for startups?

Top crowdfunding platforms for startups include Kickstarter, Indiegogo, and SeedInvest. Each offers unique features and funding models for business growth.