Back

Back

Table of Contents

Financial stress testing for startups means simulating extreme but realistic scenarios to see how your business holds up when things go wrong. Instead of relying on a single, “business-as-usual” forecast, you deliberately ask, “What if revenue drops hard? What if costs spike? What if fundraising takes twice as long?”

This helps you find weak spots, test your assumptions, and build real resilience into your financial plan. In short, a normal forecast gives you a target. This guide on stress testing gives you a survival map with contingency routes for when the journey gets bumpy.

What Is Financial Stress Testing (and Why It Matters)?

Financial stress testing is essentially advanced scenario planning focused on downside scenarios. It involves modeling severe “what-if” situations, e.g. a steep revenue drop, a funding delay, or a cost spike, and checking their impact on your cash flow, burn rate, and overall runway. The key is that scenarios should be extreme yet realistic (push the limits of bad outcomes without becoming implausible). By doing this, startups can see where they’d hit breaking points and prepare fixes in advance.

How Financial Stress Training Different from Standard Forecasting?

A typical financial forecast or budget usually projects one outcome (often an optimistic base case). Stress testing, in contrast, explores multiple outcomes, especially negative ones, to ensure you’re ready for surprises. Standard forecasts can lull teams into a false sense of security; stress tests force you to ask hard questions and plan for crises.

In practice, startups often build at least three scenarios in their model: a base case, an upside (best-case), and a downside (worst-case). Stress testing emphasizes the downside and even a “severe downside” scenario beyond your normal worst case.

This way, you’re not just hoping for the best, you’re planning for the worst while still aiming for success. As one startup finance guide puts it, scenario analysis complements regular forecasting by providing a structured way to evaluate risks and adapt strategies, ensuring resilience in volatile markets.

Why Does Stress Testing Matter For Startups?

Startups operate with tight resources and high uncertainty, a single unexpected hit can threaten survival. Stress testing helps you avoid nasty surprises by revealing how much stress your finances can take before breaking. It prompts you to line up contingency plans (e.g. expense cuts, bridge funding) ahead of time instead of scrambling in panic.

It also makes your financial model more realistic and robust. Founders are naturally optimistic, but a good model isn’t just a rosy vision, it’s a tool to understand reality. Running downside scenarios “forces you to consider all the different routes your business might take, good or bad, so that you can plan accordingly. Investors and boards appreciate this level of foresight.

Presenting only an optimistic case can hurt credibility if you miss targets, whereas showing you’ve war-gamed multiple outcomes demonstrates prudence and strategic thinking. In short, stress testing turns planning into preparation: it’s not about predicting doom, but about knowing how you’d respond if challenges hit.

Key Areas to Test

- Formula Logic

Errors in formulas can lead to cascading inaccuracies throughout the model. Systematic checks ensure that calculations for retained earnings, net income, and dividends are accurate. - Assumption Variability

Testing assumptions under different scenarios reveals how sensitive the model is to changes. For instance, altering revenue growth rates or expense forecasts can highlight vulnerabilities that might otherwise go unnoticed. - Balance Sheet Consistency

Ensuring that balance sheet components add up correctly is another vital step.

Enhancing Model Reliability

A well-tested financial model not only improves internal decision-making but also builds confidence among stakeholders. Most leading institutions embrace this discipline. According to McKinsey & Company, 75% of financial institutions now integrate Artificial Intelligence into financial modeling frameworks. This trend signals widespread recognition of the value in modern stress testing.

Financial professionals who emphasize stress testing can create reliable, resilient models, leading to stronger stakeholder collaboration and improved results. Choosing the best financial forecasting software for startups enhances the accuracy of projections, a critical step before conducting stress tests to ensure resilience.

Early-Stage Startup Stress Testing (Pre-seed, Seed, Series A)

In the early stage, stress testing is mainly about not running out of money before you prove anything. You have limited historical data, your revenue is uncertain (or non-existent), and most of your spend is going into product and early GTM experiments.

Here, stress tests should zoom in on runway, timing, and survival. For example:

- What if revenue starts 6–9 months later than planned?

- What if you only hit 30–50% of your expected revenue ramp?

- What if salaries, marketing, or tech costs end up 20–30% higher than budgeted?

For each scenario, you’re asking:

- How many months of runway do we have?

- Do we still reach key milestones (MVP, PMF, early traction) before we run out of cash?

- Do we need to cut burn, slow hiring, or start fundraising earlier?

A simple but powerful exercise: build base-case, best-case, and worst-case tabs in your spreadsheet. In the worst case, push out the first meaningful revenue and delay the next funding round by a few quarters. If that version has you dying in 8 months instead of the 18 you had in mind, that’s your signal to:

- Trim “nice-to-have” expenses now

- Explore a smaller bridge round

- Renegotiate timelines with contractors or vendors

Early-stage stress testing is about avoiding nasty surprises. You’re not trying to be perfectly accurate; you’re trying to make sure a delay in revenue or funding doesn’t quietly kill the company while you’re heads-down building.

Growth-Stage Startup Stress Testing (Post-Series A/B and Beyond)

At the growth stage, you’ve usually proven the model, have meaningful revenue, and are scaling across markets, products, or teams. Stress testing here is less about “Do we survive next year?” and more about “Can we keep scaling if headwinds hit?”

You’ll typically have a more detailed model with:

- Multiple revenue streams or geos

- Bigger teams and budgets

- Possibly debt, covenants, or more complex investor expectations

Growth-stage stress tests should look at scaling risks and external shocks, such as:

- What if we double headcount and expand into a new region, but revenue comes in 25–30% below plan?

- What if a major customer churns or a competitor forces price cuts?

- What if CAC rises or churn doubles, how does that hit runway, margins, or debt covenants?

Here you’re using stress tests to:

- Check whether you still have 18–24 months of runway in a downside case

- See how sensitive your model is to key KPIs (CAC, LTV, gross margin, churn, sales cycle)

- Decide when to pull back (hiring freeze, opex cuts) or when you can safely lean in

Many later-stage teams formalize “trigger plans,” for example:

If MRR growth drops below X% for Y months, freeze hiring and cut marketing by Z%.

Because you now have a larger org and a board, stress testing also becomes a communication tool. Sharing downside scenarios and clear response plans with leadership and investors aligns everyone on what happens if the market turns or a big deal falls through, no panic, just playbook.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

Proven Methodologies for Financial Stress Testing

Understanding how financial stress testing helps models respond to adverse conditions is critical for risk management. Each method assesses how models respond to different scenarios.

1. Scenario Analysis: Testing Hypothetical Conditions

Scenario analysis is about asking, “What happens to our numbers if the world tilts against us?” You take your financial model and test it under severe but plausible conditions, like recessions, market crashes, or industry-specific shocks, to see where it breaks.

By simulating these downside situations, you can spot weak points in revenue, costs, liquidity, or leverage. That, in turn, helps you design stronger risk controls, contingency plans, and capital buffers before those events hit.

Regulators use the same approach at a much larger scale. For example, a proposed 2026 stress scenario includes a sharp rise in unemployment plus steep drops in housing and commercial real estate values, benchmarks like these help shape what “serious enough” looks like when you design your own scenarios.

2. Sensitivity Analysis: Examining Variable Impacts

Sensitivity analysis focuses on the effects of individual variable changes on a financial model. By altering one factor at a time, such as interest rates or inflation, this approach highlights the specific elements that have the most significant impact on performance. It’s particularly useful for pinpointing areas of concern and refining model parameters to enhance accuracy.

3. Reverse Stress Testing: Defining Failure Points

Reverse stress testing flips the traditional approach by identifying conditions that would lead to model failure. Instead of starting with plausible scenarios, this method works backward to determine the thresholds at which a financial system becomes unsustainable. This proactive approach helps organizations understand their limits and prioritize safeguards against catastrophic risks.

The Role of Dynamic Financial Models in Stress Testing

Building on these methodologies, dynamic financial models allow rapid adjustments to inputs for instant scenario assessment. This flexibility enables real-time stress testing, helping organizations respond quickly to changing conditions. Dynamic models support more frequent and varied scenario analysis, improving risk preparedness. Adopting this approach ensures your stress testing remains relevant as market factors evolve.

Regulatory Compliance as a Driver for Stress Testing

Beyond internal risk management, regulatory frameworks often mandate rigorous stress testing for financial institutions. Standards such as Basel IV and Dodd-Frank require banks to demonstrate model resilience under adverse scenarios. Meeting these requirements ensures compliance and protects organizations from regulatory penalties. Incorporating mandated stress tests strengthens both governance and stakeholder confidence.

Each methodology serves a distinct purpose, offering a comprehensive view of a model’s resilience. While scenario analysis prepares for external disruptions, sensitivity analysis refines internal variables, and reverse stress testing ensures preparedness for worst-case outcomes. Together, these techniques form a robust framework for financial stress testing.

These methodologies empower businesses to refine their risk management processes and develop models that can withstand volatility.

Best Practices for Effective Financial Stress Testing

Financial stress testing is a critical tool for assessing an organization’s resilience under adverse conditions. To ensure credible, actionable results, adopt proven practices. Here are seven strategies to enhance the effectiveness of stress tests.

1. Define Clear Objectives

A well-defined purpose sets the foundation for a successful financial stress testing process for startups. Whether the goal is to evaluate liquidity, capital adequacy, or operational risks, clarity ensures the testing aligns with organizational priorities. This step also helps stakeholders understand the relevance of the outcomes.

2. Focus on Realistic Scenarios

Selecting scenarios that reflect plausible economic or market conditions is crucial. Unrealistic or overly optimistic assumptions can undermine the reliability of the results. For example, incorporating historical data from past financial crises can provide valuable insights into potential vulnerabilities.

3. Incorporate Advanced Technology

Modern tools and software streamline the stress testing process, enabling more accurate simulations and faster analysis. Solutions like Deluxe Payment Exchange+ can enhance operational efficiency by eliminating manual processes and offering secure payment options. Integrating such technologies into financial workflows ensures better preparedness for stress scenarios.

4. Regularly Update Testing Scenarios

Economic conditions and market dynamics evolve rapidly. Regularly revisiting and updating stress testing scenarios ensures they remain relevant and reflect current risks. This practice helps organizations stay ahead of emerging threats.

5. Engage Cross-Functional Teams

Effective stress testing requires collaboration across departments, including finance, risk management, and operations. Diverse perspectives enrich the process, ensuring comprehensive coverage of potential risks.

6. Validate Results Thoroughly

Validation is essential to confirm the accuracy and reliability of stress testing outcomes. Using independent reviews or external audits can strengthen confidence in the results and highlight areas for improvement.

7. Translate Insights into Action

The ultimate goal of financial stress testing is to drive actionable strategies. Organizations must use the insights gained to refine risk management frameworks, enhance decision-making, and strengthen overall resilience.

Implementing these best practices helps businesses conduct financial stress tests that provide valuable insights, ensuring long-term stability and growth.

Building a 3-Scenario Financial Model (Base, Downside, Severe Downside)

To run proper stress tests, you need more than a single “best guess” forecast. Instead of one static spreadsheet, build a financial model that can switch between at least three scenarios:

- Base

- Downside

- Severe Downside

(You can add an Upside/Best Case too, but here we’re focused on the downside view.)

1. Define Your Base Case

Your Base Case is the “most likely” plan – your normal forecast or budget.

It should reflect:

- Your expected revenue growth

- Planned hiring and operating costs

- Your target fundraising plan

Example: “Grow sales 100% this year and raise $5M at year-end.”

Get this clear and agreed with your leadership/investors. Every other scenario is just a version of this plan with different assumptions.

2. Define Downside and Severe Downside

Next, define two tougher versions of reality:

- Downside – things go wrong, but not disastrously

- Severe Downside – the “keeps you up at night” case

Example for annual revenue:

- Base: $1M

- Downside: $600k (40% shortfall)

- Severe: $300k (70% shortfall)

Downside should feel uncomfortable but plausible. Severe should feel unlikely but not impossible (say ~5–10% probability). You can use the worst historical quarters in your industry, prior crises, or COVID-style shocks as a reference point.

Key question to ask for each:

“If this scenario happens, how does the business stay alive and what changes do we make?”

3. Set Up a Scenario Toggle in Your Model

In Excel or Google Sheets, create a simple scenario control panel:

- List your key assumptions in rows:

- Revenue growth %

- Pricing

- Unit costs

- Headcount and hiring plan

- Marketing spend, etc.

- Add three columns: Base, Downside, Severe Downside

Then:

- Create one “Scenario” cell (e.g. 1 = Base, 2 = Downside, 3 = Severe)

- Use formulas like

CHOOSEorINDEXso the rest of your model pulls the correct column based on that scenario number

Result:

- Change one cell → your full P&L, cash flow, and dashboards instantly switch to that scenario

- You can see cash balance, runway, and key metrics under each case without rebuilding the model

This effectively turns your spreadsheet into a simple scenario dashboard.

4. Model the Financial Statements Under Each Scenario

Your scenario assumptions should flow cleanly into your financials, not just sit in a separate table. At minimum, link them into:

- Income Statement (P&L)

- Cash Flow

- Ideally, Balance Sheet (or simplified working capital)

Examples:

- Revenue should depend on scenario-driven inputs (e.g. sales growth %, new customers, ARPU).

- Headcount and salary costs should reflect different hiring plans (e.g. hiring freeze in the Severe case).

- Marketing spend, software, contractors, and other Opex lines should all reference the scenario columns.

Pull these into a summary tab that shows side-by-side:

- Revenue

- Burn rate

- Year-end cash

- Runway (months of cash left)

- EBITDA or net income

Bonus: add a chart that shows cash balance over time for Base vs. Downside vs. Severe. Visually seeing how quickly cash falls in the worst cases is often more powerful than raw numbers.

5. Incorporate Multi-Variable Changes (Not Just One Slider)

A scenario is not “change one number and call it a day.” Real-world shocks hit multiple levers at once. Each scenario should be a bundle of assumptions, for example:

Downside scenario might include:

- Sales growth 50% lower

- Hiring slowed or partially frozen

- Marketing spend cut 20%

- No salary raises

- Customers paying 15 days later than usual

Severe Downside might stack further:

- Sales 70% lower

- Full hiring freeze

- Temporary price cuts (lower gross margin)

- Customers paying 30+ days later

- Deeper reductions in discretionary spend

If it gets too complex, focus on the 3–5 biggest drivers for your business:

- SaaS: new MRR growth, churn, CAC, gross margin

- E-commerce: traffic, conversion rate, average order value, cost of goods

Get those right per scenario instead of obsessing over minor line items.

6. Attach Clear Contingency Plans to Each Scenario

A 3-scenario model is useless if it doesn’t drive action. For each downside scenario, decide what you’d actually do:

- If Severe Downside shows cash going negative in 9 months, what’s the move?

- Lay off X% of staff?

- Freeze hiring?

- Cut marketing by Y%?

- Draw on a credit line?

- Raise an internal bridge?

Turn these into if–then rules, for example:

- “IF revenue < $X by Q3, THEN execute Cost Plan A.”

- “IF runway < 9 months, THEN halt new hiring and cut paid marketing 30%.”

Your model can also calculate how big each move needs to be:

- “We need to cut $500k in annual expenses to get back to 18 months of runway in Downside.”

- “In Severe, we need either $1M extra capital or $1M in cuts.”

Document these playbooks so you’re not improvising in a panic if numbers start tracking to the downside.

7. Review and Update Scenarios Regularly

This is not a “build once and forget” exercise. As real data comes in:

- Compare actuals vs. Base and Downside

- Adjust assumptions if you’re consistently above or below your plan

- Retire outdated scenarios and create new ones as the business evolves

Good habits:

- Early stage: refresh scenarios every 1–3 months, model 12–18 months ahead

- Growth stage: extend horizon to 2–3+ years (even with more aggregated assumptions)

If you start consistently outperforming, yesterday’s Best Case might become today’s Base Case. If things worsen, yesterday’s Downside might become the new Base. Keep the model “alive.”

Why This Matters

A 3-scenario model turns your financials from a static prediction into a decision tool.

- Base Case = what you’re aiming for

- Downside = the “likely pain” case you should be ready to manage

- Severe Downside = your crash test that shows where things break and what you’ll do

You don’t build this to feel good; you build it to know where the floor is—and how you’ll react before you hit it.

Decoding Financial Model Stress Testing: Trends and Challenges

Stress testing is a cornerstone of good financial modeling. It shows if your predictions can handle different conditions and builds confidence among stakeholders.

Validation Checks:

- Systematically review assumptions, inputs, and outputs.

- Cross-check with historical data or industry benchmarks to catch errors early.

A layered approach makes stress tests even stronger. This means using different tests like scenario analysis, sensitivity testing, and extreme case simulations. Each test looks at the model from a unique angle, which reinforces its overall accuracy.

Regular stress testing helps validate your assumptions and uncovers hidden risks. With a clear, structured process, your financial models become both accurate and resilient, ready to face uncertainty head-on.

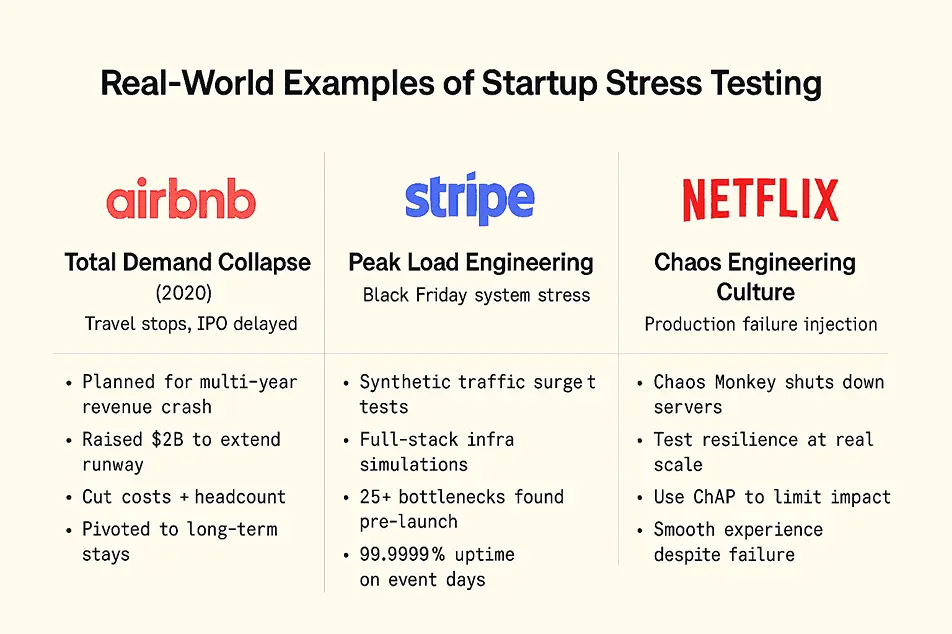

Real-World Examples of Startup Stress Testing

1. Airbnb – Stress-Testing the Business Model in a Total Demand Collapse

When COVID-19 hit in early 2020, Airbnb went from “about to IPO” to “zero travel, near-zero revenue” in a few weeks. Global travel restrictions caused bookings to collapse and forced the company to rethink its entire cost structure and growth story.

Airbnb’s leadership effectively ran a massive real-world stress test on its business model:

- Downside scenarios: Management worked from the assumption that travel might be depressed for years, not months. They focused on survival under worst-case revenue scenarios, not optimistic rebounds.

- Cash and runway first: The company raised roughly $2 billion in new financing to extend runway and give itself room to make painful but strategic decisions.

- Aggressive cost resets: Airbnb cut marketing spend, paused non-core initiatives, and reduced headcount to bring fixed costs in line with its new, stressed revenue base.

- Micro-pivot inside the stress test: As part of its scenarios, Airbnb leaned into domestic, longer-term stays (remote workers, relocations) instead of purely short city breaks, effectively testing a new demand mix while the old one was broken.

The result: by treating COVID as a stress-test scenario rather than a temporary blip, Airbnb preserved cash, rebuilt a leaner model, and still managed to go public in a much stronger, more disciplined shape.

Takeaway for founders: Run brutal downside scenarios (e.g., “what if revenue drops 70–80% for 12–18 months?”). Then actually adjust headcount, burn, and priorities as if that scenario might be real. If the storm never gets that bad, you’ve just over-prepared.

2. Stripe – Load-Testing for Black Friday Like a Financial Heart Stress Test

Payment infrastructure company Stripe treats Black Friday and Cyber Monday as an annual stress test of its entire stack. On these days, Stripe has reported handling peak loads above 20,000 requests per second and processing more than $3 billion in transactions per day.

To avoid even seconds of downtime, Stripe doesn’t just hope for the best, it systematically stress-tests its systems in advance:

- Synthetic traffic surges: Engineers ramp up artificial traffic to simulate Black Friday–level load and beyond, probing how the system behaves near its limits.

- Full-stack stress tests: Rather than testing isolated services, Stripe load-tests the entire infrastructure “from top to bottom” – network, databases, payment APIs, and monitoring.

- Issue hunting under pressure: Before the real event, the team identifies and fixes dozens of bottlenecks and anomalies that only appear at extreme scale. In one reported period, they found and resolved around 25 such issues ahead of Black Friday.

Because of this discipline, Stripe has achieved reported uptimes of 99.9999% (“six nines”) on some of the busiest e-commerce days of the year, essentially seconds of downtime across an entire year.

Takeaway for founders: Don’t wait for your first big launch or press hit to discover your breaking point. Recreate “funding-announcement day” or “Product Hunt day” traffic in a controlled test and see what dies first: the database, the API, or your runway.

3. Netflix – Deliberately Breaking Things with Chaos Engineering

Netflix turned stress testing into a culture. Instead of waiting for outages, they intentionally cause failures in production using tools like Chaos Monkey, part of their “Simian Army.”

Here’s how their stress testing works in practice:

- Random failure injection: Chaos Monkey randomly shuts down server instances inside Netflix’s production environment. Engineers are forced to design services that keep working even when key components disappear without warning.

- Hypothesis-driven experiments: Netflix starts with a hypothesis like “if this service fails, users should still be able to stream.” Chaos tools then test whether that resilience actually holds at real scale.

- Controlled blast radius: Newer tools like ChAP (Chaos Automation Platform) run experiments on a small fraction of traffic, measuring impact before rolling anything wider, so the “stress test” doesn’t turn into a full-blown disaster.

Chaos engineering is basically permanent stress testing of a live system. Netflix uses it to ensure that when a data center, microservice, or dependency fails, customers still see a smooth experience instead of a spinning wheel.

Takeaway for founders: You don’t need full chaos engineering on day one, but you do need to simulate bad things: API timeouts, database node loss, key vendor down, or a third-party service failing. If your app or operations fall apart in a simulation, they’ll definitely fall apart in front of users.

Core Stress Testing Scenarios to Model

So what should you actually stress test? Every startup is different, but there are a handful of “must-have” scenarios almost everyone should model.

1. Revenue Shortfalls

Core question: “What if our sales are much lower than forecast?”

Model versions where:

- Revenue or growth is 30–50% lower than your base case for the next few quarters.

- A key customer churns or a big deal slips by 6–12 months.

- Revenue flatlines or even shrinks for a period.

Focus on:

- How fast cash burn accelerates.

- How many months of runway you have if revenue stalls.

- When you’d literally run out of money (your “floor”).

If the downside shows you hitting that floor too soon, you know you need to cut costs, adjust hiring, or find extra cash options.

2. Fundraising Delays or Droughts

Core question: “What if we can’t raise when we think we can?”

Model scenarios where:

- The next round closes 6–12 months later than planned.

- You raise less money or on tougher terms.

- You get no external funding for 18–24 months.

Then ask:

- Can we survive purely on current cash + revenue?

- What happens if we freeze hiring, cut marketing, or switch to “profitability mode”?

- Do we need backup options like venture debt, a bridge round, or deeper cuts?

This is uncomfortable but essential. Many startups die not because the business is bad, but because they assumed fundraising would be easy and on time.

3. Unexpected Cost Increases

Core question: “What if our costs suddenly jump?”

Pick your major cost drivers and push them up:

- Supplier / manufacturing costs

- Cloud and infrastructure spend

- Salaries and benefits

- Paid marketing / ad costs

Example scenarios:

- Cloud or supplier costs rise by 20–30%.

- Ad performance drops, so CAC goes up and ROAS goes down.

- Gross margin falls by 5–10 percentage points.

Look at:

- Whether you stay above breakeven or plunge into deep losses.

- How sensitive your runway is to margin drops.

- Which trigger points you should define (e.g. “If gross margin < X%, freeze non-essential spend”).

This protects you from “cost creep” quietly wrecking your unit economics.

4. Customer Churn or Demand Slumps

Core question: “What if customers leave faster or buy less?”

Especially critical for SaaS and subscription models. Try:

- Doubling your monthly churn (e.g. from 2% → 4–5%).

- Slowing new customer acquisition to near zero for a few months.

- Lowering expansion / upsell assumptions.

Then examine:

- What happens to MRR / ARR and cash flow.

- Whether you can still cover fixed costs.

- How badly net revenue retention suffers.

Use this to pre-plan retention moves—discounts, better onboarding, success outreach—if you see churn ticking up in real life.

5. Macroeconomic or Market Shocks

Core question: “What if the whole environment turns against us?”

Think recession, pandemic, regulatory change, or a major industry shock. Combine multiple hits, such as:

- Revenue down 40%+.

- Customers paying slower (hurting cash collection).

- Fundraising effectively frozen.

- Costs up due to inflation, FX, or supply chain issues.

This is your “black swan” or severe downside case. It’s low probability but high impact—and the one that separates “we’ll be fine” from “we need to move now” if something big breaks.

6. Combining Scenarios and Setting Boundaries

Real crises rarely arrive one variable at a time. A recession might mean:

- Lower sales

- Higher churn

- Cost pressure

- Tougher fundraising

You don’t need to model every permutation, but you do need a coherent set of scenarios, for example:

- Base Case: Your planned numbers.

- Downside Case: ~50% of target growth, some churn increase, minor cost pressure.

- Severe Downside Case: Revenue flat or falling for a period, churn up, funding delayed, costs rising.

Each scenario should tell a logical story, not random changes. The goal isn’t to predict the future perfectly, but to know your resilience range, where your model holds, where it breaks, and what actions you’ll take before you hit the wall.

Conclusion

The insights gained from finance stress testing should not remain isolated. Instead, integrate these findings into your broader strategic planning to enhance long-term resilience. For example, if a stress test reveals vulnerabilities in cash flow during a downturn, consider revising your financial projections or exploring alternative revenue streams. Knowing how to create a financial model for investors lays the foundation for attracting investors, and stress testing ensures these models remain resilient under varying market conditions.

Ultimately, stress testing is more than a diagnostic tool, it’s a proactive measure to safeguard your financial stability. At Qubit Capital, we specialize in financial model creation. Contact us today to explore how we can support your financial planning and resilience strategies.

Key Takeaways

- Regular financial stress testing is essential to build resilient financial models.

- Advanced methodologies like scenario, sensitivity, and reverse stress testing offer deep risk insights.

- Realistic scenarios and systematic error checks are critical for accurate models.

- Continuous review and integration of findings enhance financial planning.

- Leveraging expert services at Qubit Capital can elevate your financial strategy.

Need numbers investors trust?

Clean assumptions, realistic projections, and a structure that holds up in diligence.

- Forecasts, unit economics, and scenario planning

- Valuation-ready outputs investors can review fast

- Clear structure so you can update it easily

Frequently asked Questions

What are the proven methodologies for financial stress testing?

Common methodologies include scenario analysis, sensitivity testing, and reverse stress testing. These approaches help identify vulnerabilities in financial models.