- Convertible Securities and Instruments Overview

- Understanding the Key Terms of a Convertible Notes

- Comprehensive Overview of SAFE Instruments

- Comparative Analysis: SAFEs vs Convertible Notes

- Guidance and Best Practices for Usage

- Tax Implications of Convertible Instruments

- Valuation Impact and Financing Considerations

- Conclusion

- Key Takeaways

For startups seeking flexible financing options, convertible debt and SAFE (Simple Agreement for Future Equity) notes are often at the forefront of consideration. These tools offer a way to secure funding without immediately setting a company valuation, making them particularly appealing during early-stage growth or uncertain market conditions. Understanding the nuances of convertible note vs SAFE is critical, as each comes with unique structures, benefits, and potential trade-offs.

Startups often explore various types of startup funding before deciding on the appropriate financial strategy tailored to their unique needs. In this blog, we'll break down the mechanics of convertible debt and SAFE notes, compare their features, and explore their relevance in startup financing. Let’s dive in!

Convertible Securities and Instruments Overview

Startups often face the challenge of acquiring funding while avoiding the complexities of immediate valuation. Convertible securities offer an ideal solution, providing the flexibility needed to raise capital without assigning a definitive worth to the company. These instruments bridge the gap between early-stage funding and formal equity issuance, making them a popular choice in the startup ecosystem.

Convertible securities function by granting investors a debt or equity-like instrument that can later convert into shares of the company. This conversion typically occurs during a subsequent financing round or upon meeting predefined conditions. Two common types of convertible securities are convertible notes and SAFEs (Simple Agreements for Future Equity).

Convertible Notes Explained

A convertible note begins as a loan to the company, accruing interest until it converts into equity. This conversion usually happens during a qualifying financing event, at a discount or with a valuation cap that benefits the early investor. To understand the foundational aspects of convertible notes, including their mechanics and investor considerations, refer to the Toptal Note, which outlines their flexibility as financing tools.

SAFEs: A Simpler Alternative

SAFEs, are agreements designed to simplify the fundraising process. Unlike convertible notes, SAFEs do not accrue interest or act as debt. They provide investors with the right to receive equity at a future date, typically when the startup raises a priced round. The absence of repayment obligations makes SAFEs attractive to founders, especially during early-stage funding.

Convertible securities allow startups to delay the challenges of immediate valuation while raising capital efficiently. However, understanding the differences between these instruments is crucial before deciding which suits your business goals. Comparing equity vs debt financing provides essential insights into broader funding structures and can clarify how convertible securities fit into your long-term strategy.

By grasping the mechanics of SAFEs and convertible notes, founders and investors can align their funding strategies with growth objectives while safeguarding their interests.

Understanding the Key Terms of a Convertible Notes

Convertible notes offer a unique blend of debt and equity, making them a popular choice for startup fundraising. These instruments start as loans, accumulating interest, before transforming into equity during a qualifying financing event. Understanding the mechanics and nuances of convertible notes is key to assessing their suitability for your funding strategy. Let’s explore their structure, terms, and advantages.

Mechanics of Convertible Notes

Convertible notes are structured as short-term debt that converts into equity. This transformation typically occurs during a qualifying financing round when a startup raises additional funds. Until conversion, the note accrues interest—a feature that compensates early investors for the risks involved. Interestingly, statistics show that 36% of pre-seed convertible notes carry interest rates exceeding 8%, reflecting the heightened risk of investing in early-stage companies.

Key terms like the valuation cap, discount rate, and interest rate define the financial dynamics of a convertible note. The valuation cap sets a maximum price for conversion, ensuring early investors benefit from future growth. Meanwhile, the discount rate rewards investors by allowing them to purchase equity below the market price during the conversion event.

Pros and Cons

Convertible notes offer simplicity and flexibility. They allow startups to raise funds quickly without negotiating a fixed valuation upfront. However, they also come with potential downsides. High-interest rates—reported in 47% to 66% of convertible notes with ≥8% interest—can impose significant financial burdens, especially for early-stage companies. Furthermore, the lack of immediate equity ownership may deter some investors who prefer more control from the outset.

When comparing convertible notes to other funding options, founders often evaluate the difference between SAFE and convertible note agreements. SAFE (Simple Agreement for Future Equity) eliminates interest and maturity, offering a more straightforward route to equity.

Convertible notes remain a dynamic tool for startups seeking to balance immediate financing with long-term growth opportunities.

Comprehensive Overview of SAFE Instruments

SAFE agreements, short for Simple Agreements for Future Equity, have gained significant popularity among startups. They offer a straightforward and founder-friendly alternative to complex financing methods like convertible notes. Unlike debt instruments, SAFEs are purely equity-based, meaning they do not include interest accrual or maturity dates. This eliminates repayment obligations, allowing founders to focus on growth without the looming pressure of deadlines.

One of the most appealing aspects of SAFEs is their simplicity. They are easy to draft and execute, making them particularly attractive for early-stage companies. For those looking to start a SAFE fundraising process, resources such as Safe Setup provide clear instructions on how to initiate this process.

What sets SAFEs apart from convertible notes is their structure. While convertible notes are technically debt instruments, SAFEs operate exclusively as equity agreements. Convertible notes come with interest rates and maturity dates, adding layers of complexity that founders must manage. Understanding the differences—often simplified as safe vs convertible note—is crucial for startups seeking funding options that align with their long-term vision.

Despite their simplicity, SAFEs are not without nuances. Achieving the right balance between equity and debt financing can unlock sustainable growth while preserving ownership stakes. Founders can explore broader strategies for balancing equity and debt financing to better understand how SAFEs fit into a diversified capital structure.

In summary, SAFE agreements streamline the fundraising process, offering founders equity-based terms without the complications of traditional debt instruments. Their flexibility and simplicity make them a preferred choice for startups navigating early-stage funding challenges.

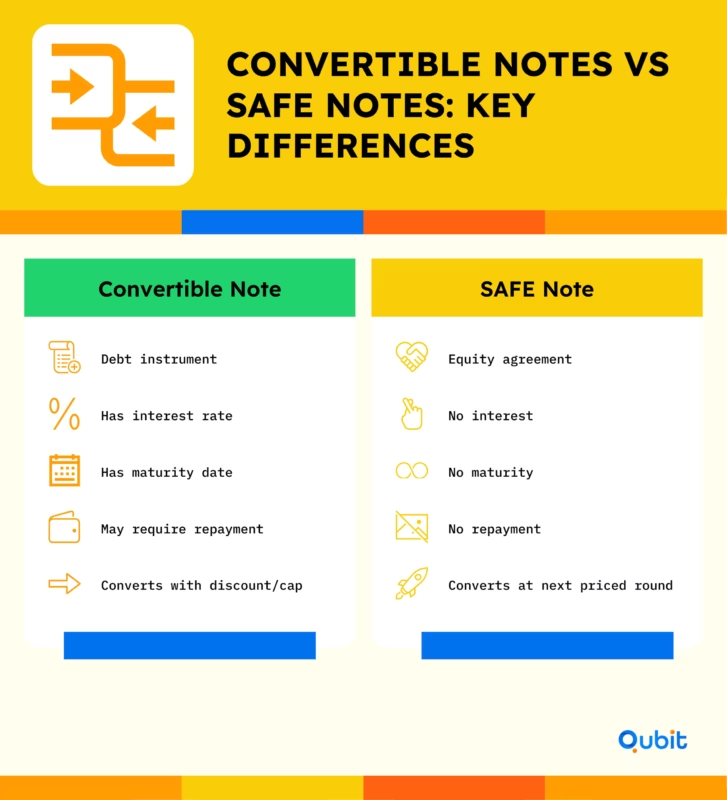

Comparative Analysis: SAFEs vs Convertible Notes

Understanding the differences between SAFEs (Simple Agreements for Future Equity) and convertible notes is essential for startups seeking early-stage funding. While both instruments offer a pathway to delayed equity issuance, their structural nuances set them apart. Here’s a detailed comparison:

Key Structural Differences

- Interest Accrual

Convertible notes accrue interest over time, typically ranging from 4% to 8% annually. This interest adds to the principal investment, increasing the eventual conversion amount. SAFEs, on the other hand, do not accrue interest, making them simpler and potentially less expensive for startups. - Maturity Dates

Convertible notes come with defined maturity dates, creating a repayment obligation if the note doesn’t convert into equity within the specified timeframe. SAFEs lack maturity dates, removing the pressure of repayment and offering greater flexibility to startups. - Conversion Mechanics

While both SAFEs and convertible notes convert into equity during subsequent funding rounds, notes generally require a triggering event, such as reaching a valuation cap or discount. SAFEs streamline this process, automatically converting into equity upon qualifying rounds without additional financial obligations.

Market Trends: SAFEs Leading the Way

Data indicates that SAFEs are 5x more common than convertible notes in specific startup ecosystems. This shift reflects their growing appeal due to simplicity and reduced financial strain, particularly for early-stage companies.

Guidance and Best Practices for Usage

Choosing between SAFEs and convertible notes depends on the unique circumstances of your startup. SAFEs are often preferred when simplicity and speed are priorities, while convertible notes are ideal for scenarios involving interest accrual or specific maturity dates. Understanding the convertible note meaning is critical to determining which option aligns with your fundraising goals.

To streamline decision-making, practical tools can make a significant difference. Use the Get started calculator to simulate various valuation caps and discount rates, helping you gauge potential dilution effects. Additionally, the Download checklist ensures that no critical steps are overlooked during the fundraising process, offering a comprehensive guide for both SAFEs and notes.

When implementing either instrument, follow a step-by-step strategy. Begin by clarifying your funding requirements and timeline. Next, consult the checklist to verify essential legal and financial considerations. Finally, use modeling tools to optimize your terms and validate key metrics.

By combining these actionable practices with the right resources, startups can create a structured and efficient fundraising process tailored to their needs.

Tax Implications of Convertible Instruments

Tax treatment varies significantly between convertible notes and SAFEs, and understanding these differences is crucial for investors and companies. SAFEs (Simple Agreements for Future Equity) are classified as non-debt instruments. Upon conversion into equity, the gains are typically treated as capital gains, which often results in a lower tax rate compared to ordinary income. This structure appeals to those seeking favorable long-term tax positioning.

In contrast, convertible notes operate as debt instruments until conversion. Investors may benefit from interest deductions, reducing taxable income during the note’s active period. However, the interest earned is taxed as ordinary income, which is generally subject to higher rates compared to capital gains. These contrasting tax implications highlight the importance of considering the financial and tax consequences when choosing between a SAFE and a convertible note.

To define convertible notes further, they are debt agreements that convert into equity at a later date, typically triggered by specific events such as funding rounds or valuation thresholds. This dual nature—initial debt followed by equity conversion—adds complexity to their tax treatment, making professional advice essential for informed decision-making.

Investors and founders alike should evaluate the tax outcomes of each structure to align with their financial strategies and compliance requirements.

Valuation Impact and Financing Considerations

Equity dilution and investor returns hinge on key factors such as valuation caps, discount rates, and conversion terms. Startups often grapple with balancing ownership retention while securing the capital needed for growth.

A valuation cap example illustrates how a lower cap, like $1M in an early-stage convertible agreement, can significantly enhance an investor's equity stake upon conversion. For founders, this can mean higher dilution if the company’s valuation exceeds the cap at the time of conversion. Discount rates also play a role, granting investors a preferential price on future equity, further influencing ownership percentages.

Conversion terms dictate when and how these instruments convert into equity, directly affecting the equity pool and investor returns. Founders must carefully assess these terms to avoid excessive dilution while ensuring investors see fair returns.

Understanding the differences between convertible note vs SAFE agreements is critical, as each impacts valuation and financing outcomes differently. SAFE agreements typically simplify the process but may lack the structured repayment terms found in convertible notes. By aligning these mechanisms with the company’s long-term goals, founders can strike the right balance between growth funding and ownership preservation.

Conclusion

When choosing between convertible notes and SAFE notes, understanding the nuances is critical. Both funding instruments offer unique benefits, but their practicality depends on key aspects like tax implications, valuation caps, and conversion mechanisms. By carefully analyzing these terms, founders can align funding strategies with their long-term goals.

It’s equally important to approach these decisions from a data-driven perspective. Evaluate factors such as dilution, timing, and investor expectations to ensure optimal outcomes for your startup. Whether you're seeking simplicity or flexibility, the right choice can significantly impact your growth trajectory.

If you're ready to secure the right capital for your startup, we at Qubit Capital offer expert Fundraising Assistance to guide you through every step. Let us help you navigate the complexities of startup financing, so you can focus on building your vision.

Key Takeaways

- Convertible debt and SAFE notes each present unique advantages, depending on your funding stage and goals.

- Convertible notes accumulate interest and include defined maturity, offering investor protections.

- SAFEs provide a simpler, faster route to equity without debt-related obligations.

- Key terms such as valuation caps, discounts, and conversion effects are critical to understanding overall impact.

- Leveraging expert tools and Qubit Capital’s services can streamline your funding strategy.

Frequently asked Questions

What is the main difference between a SAFE and a convertible note?

A SAFE is a simple agreement for future equity with no interest or maturity date, while a convertible note is a debt instrument that accrues interest and must convert or be repaid by a set date.