Table of Contents

Securing funding is often a pivotal challenge for FinTech startups, especially when balancing growth ambitions with equity preservation. Revenue-based financing (RBF) has emerged as a compelling alternative to traditional funding models, offering founders a non-dilutive way to scale their businesses. Unlike equity financing, RBF allows startups to repay investors through a percentage of their monthly revenue, aligning repayment with business performance.

A comprehensive perspective emerges as you consider fintech fundraising strategies and opportunities, which situates revenue-based financing within a wider array of fundraising models for FinTech startups. This approach empowers founders to explore diverse funding avenues while maintaining control over their vision.

In this blog, we’ll explore whether RBF is the right fit for your FinTech startup, diving into its mechanisms, benefits, and potential drawbacks.

What Is Revenue Based Financing

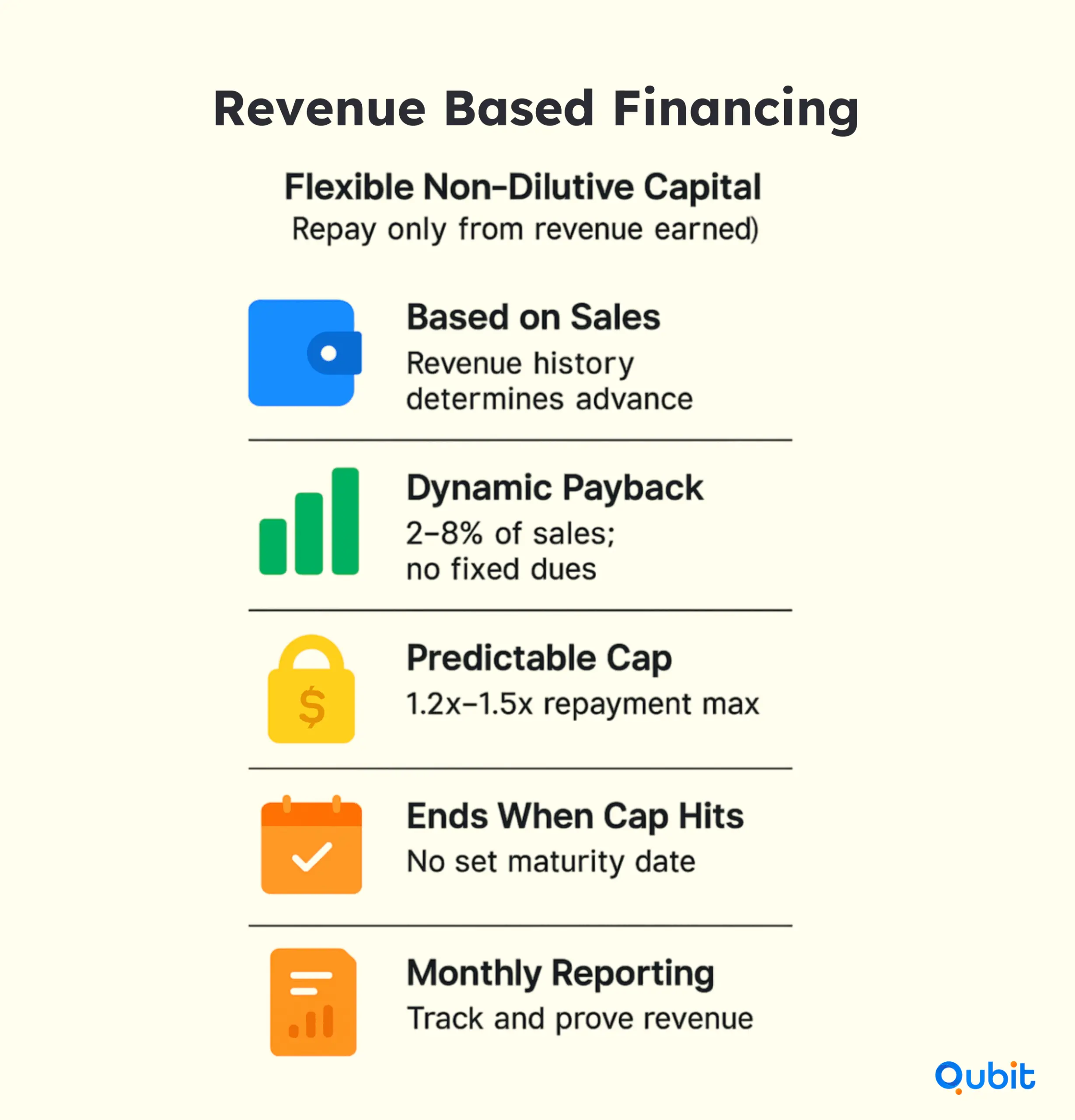

Revenue based financing gives you an upfront capital advance in exchange for a fixed percentage of future sales. There is no set interest rate. You repay more when revenue is high and less when it dips. You retain full ownership. Unlike equity rounds, you avoid share price negotiations. Unlike term loans, you sidestep fixed repayment schedules.

Key Mechanics

- Advance Amount: Calculated on your historical and projected revenue. Lenders often use a multiple of trailing twelve‐month revenue.

- Repayment Rate: Typically 2 percent to 8 percent of monthly or weekly sales. You choose a rate that balances runway and cash flow.

- Repayment Cap: Commonly 1.2 times to 1.5 times the advance. You know your maximum obligation up front.

- Term Flexibility: The deal ends once you hit the cap. There is no fixed maturity date, but most deals conclude within 3–5 years.

- Covenants and Reporting: Providers may require regular revenue reporting and minimum performance thresholds.

These mechanics align your lender’s return with your success. You pay more when you win. You have breathing room when growth slows. A closer look at fintech debt financing options underscores how traditional loan-based methods compare with revenue-sharing models, providing a balanced view of funding alternatives.

Advantages of Revenue-Based Financing for a FinTech Startup

Flexible Cost Structure

Revenue based financing adapts to your cash flow. When sales spike, you repay faster and reduce term length. In slow months, your minimum payment shrinks. This flexibility softens revenue swings common in seasonal or transaction-driven FinTech models.

No Equity Dilution

You keep your cap table clean. You avoid share sales to investors or board seats. That preserves long-term value for founders and early employees. It also prevents outside influence on day-to-day decisions.

Speed of Access

Deals often close in weeks instead of months. Providers use automated underwriting and digital reporting. You bypass lengthy investor due diligence and multiple pitch rounds. Fast access means you can capitalize on time-sensitive opportunities, such as market expansions or new product launches.

Aligned Incentives

Your success is their success. Since repayments scale with revenue, providers have a stake in your growth. They may offer guidance or connections to help you hit milestones and unlock better terms in future rounds.

Market Growth and Adoption

The global revenue based financing market reached $7.3 billion in 2024 and is projected to expand to $528 billion by 2033 at a 60.9 percent CAGR (Grand View Research 2024). Specialized firms now serve varied segments, from payments platforms to lending marketplaces.

Potential Drawbacks and Risks of RBF

Higher Cost of Capital

Effective repayment caps of 1.2 to 1.5 times translate into annualized costs that often exceed traditional term loans. For example, a cap of 1.3 times over three years corresponds to an approximate internal rate of return of 15 to 20 percent. You must weigh this against faster access and no dilution.

Dependence on Revenue Consistency

If your revenue is volatile or unpredictable, repayment periods can stretch indefinitely. That may lock you into higher total costs and hamper runway extension. Providers typically require a history of stable sales, ideally 6–12 months of recurring revenue.

Provider Scrutiny and Covenants

You must agree to regular reporting, such as monthly revenue statements. Some providers impose minimum revenue thresholds or reserves held in escrow. You could face penalties or higher repayment rates if you miss targets.

Limited Applicability

Early-stage FinTechs without recurring revenue or product-market fit may not qualify. Providers focus on models with predictable transaction volumes and clear unit economics. If you are still testing pricing or user acquisition channels, grants or equity rounds may be better suited.

Assessing Fit: Is RBF Right for Your FinTech Startup?

Fit by Business Stage

- Pre-Revenue or Prototype Phase: You lack the track record most revenue based providers require. Consider grants or angel investors to validate product market fit first.

- Early Recurring Revenue: If you have consistent subscription fees, transaction fees, or processing volumes, you can match repayment rates to cash flow. RBF can extend your runway without dilution.

- High-Growth Scale-Up: When you need tens of millions to finance marketing or new verticals, revenue based caps may become expensive. Private credit or equity rounds could offer larger tickets at comparable cost.

Key Decision Criteria

- Revenue Visibility: Do you have at least 6 months of stable sales data? Lenders seek predictability.

- Cost Comparison: Calculate the implied interest rate of the repayment cap. Compare to bank loans, lines of credit, or equity cost.

- Cash Flow Impact: Model your worst-case payment scenario. Ensure you can cover expenses in a low-revenue month.

- Runway Extension: Decide how many months of runway you need. Choose a cap and repayment rate that align with your burn and growth milestones.

- Provider Expertise: Does the lender understand FinTech revenue cycles? Look for firms specializing in payment volume, loan origination, or subscription models.

Answering these questions gives you clarity on fit. If your metrics and needs align, revenue based financing can be a smart bridge to your next equity round or sustainable growth phase.

Prepar Your Startup to Secure Revenue Based Financing

Selecting the Right Provider

Seek lenders with deep FinTech expertise. They will value your unique revenue streams—payment processing fees, lending interest income, or subscription charges. Leading providers include GetVantage, Lighter Capital, and Pipe, each focusing on different size segments and geographies. In India, GetVantage backed over 750 startups in FY 24 with non dilutive capital.

Building a Compelling Pitch

- Monthly and Annual Revenue Trends: Present clear charts of recurring revenue and transaction volumes. Highlight growth rates and customer retention.

- Customer Metrics: Share user retention rates, average revenue per user, and churn percentages. These metrics signal stability.

- Use of Funds: Specify how the capital will drive incremental revenue—whether through marketing campaigns, product launches, or geographic expansion.

- Financial Projections: Provide best-case and worst-case scenarios for repayment timelines at various revenue outcomes.

- Risk Mitigation Plans: Explain how you will manage lean periods, such as setting revenue reserves or adjusting repayment rates.

Documentation and Covenants

Prepare audited financial statements if available. Have your bank statements, payment processor reports, and accounting records ready. Expect lenders to require monthly revenue updates and compliance with covenant thresholds.

Integrating Revenue Based Financing into Your Capital Strategy

Combining Multiple Funding Sources

A blended capital stack increases resilience and extends runway:

- Early Grants and Competitions: Leverage non dilutive grants from bodies like the Small Business Administration’s PRIME program, which awarded $7 million in 2024 (Small Business Administration 2024).

- Revenue Based Financing: Bridge the gap between seed and Series A without dilution.

- Private Credit Lines: For larger ticket sizes, asset backed facilities can fund loan growth or receivables.

- Equity Rounds: Reserve equity financing for strategic partners and large scaling needs.

Best Practices for Monitoring and Repayment

- Automate Reporting: Integrate your revenue dashboards with lender portals to minimize manual work.

- Maintain Cash Reserves: Hold a buffer equal to one month of average repayments. This prevents covenant breaches in low-revenue cycles.

- Review Cap Utilization: Track how much of your repayment cap remains. That gives insight into remaining obligations and runway.

- Plan Exit Strategies: Align repayment completion with equity milestones or refinancing events.

Scenario Planning

Run quarterly simulations of revenue, repayment, and runway under different growth rates. Use these insights to adjust your repayment rate or negotiate cap extensions.

Recurring Revenue in FinTech

Consider a FinTech company with a monthly recurring revenue (MRR) of €500,000. This business secures €500,000 in funding through an RBF agreement, committing to repay the capital via a 10% revenue share. As the company maintains steady revenue growth, it successfully completes repayment within 12 months.

This scenario demonstrates the adaptability of RBF. Instead of fixed monthly payments, the repayment fluctuates based on actual revenue, ensuring the company retains financial flexibility during slower months. Investors, on the other hand, benefit from transparency, as they monitor key financial metrics like MRR to assess repayment timelines.

Accelerated Growth Through RBF

Another example involves a SaaS startup aiming to scale operations without diluting ownership. With €500,000 in MRR, the founders raise €500,000 through RBF. Thanks to consistent revenue increases, the repayment period is shortened, allowing the company to reinvest profits into growth initiatives.

This case highlights how RBF empowers founders to retain equity while accessing capital. Unlike traditional loans, where repayment schedules are rigid, RBF aligns with the company’s performance, fostering a win-win scenario for both parties.

Comparing RBF to Non-Repayable Funding

For a broader perspective, it’s worth contrasting RBF with non-repayable funding options like fintech government grants. While grants provide financial support without repayment obligations, they often come with stringent eligibility criteria and limited scalability. RBF, by contrast, offers a scalable solution tailored to revenue-generating businesses, making it a preferred choice for founders seeking growth capital without sacrificing ownership.

These examples underscore the versatility of revenue-based financing. By tying repayments to revenue, RBF ensures businesses can manage cash flow effectively while scaling operations.

Consideration of fintech strategic partnerships funding highlights collaborative financial strategies that serve as an alternate approach, enriching your exploration of financing methods alongside revenue-based models.

Conclusion

Revenue based financing can be a powerful tool for your FinTech startup. It offers flexible repayments, no equity dilution, and fast access to capital. It aligns costs with performance and brings lenders into your growth journey. However, it carries higher effective costs and demands stable revenue data.

You must weigh trade-offs around runway extension, cash flow impact, and reporting requirements. By assessing fit, preparing detailed financial models, and choosing a specialized provider, you can leverage revenue based financing as a strategic bridge. Integrate it thoughtfully into a blended capital stack to power your next growth phase while preserving ownership and control.

If you’re looking to use RBF without choking cash flow, at Qubit we understand payback caps, seasonality swings, and lender covenants. Pressure-test your model with our fintech fundraising assistance and design a blended stack that preserves ownership.

Key Takeaways

- Revenue-based financing offers a non-dilutive funding opportunity for FinTech startups.

- Repayments adjust in line with actual revenue, ensuring flexible cash flow management.

- Eligibility hinges on steady recurring revenue and strong product-market fit.

- Different design options cater to varied revenue scenarios.

- RBF stands out when compared with traditional debt and equity financing methods.

Frequently asked Questions

What is revenue-based financing in fintech?

Revenue-based financing is a funding model where businesses receive capital in exchange for a percentage of their future revenue. Unlike traditional loans, this approach doesn’t require fixed monthly payments or equity dilution.