Table of Contents

Startup fundraising has a new default, and it’s called the SAFE. In Q4 2024, nearly 90% of pre-seed rounds used SAFEs, while convertible notes barely showed up at 9%. That shift is not a trend. It’s a reset. If you’re raising early capital today, you are almost certainly negotiating a SAFE, whether you like it or not.

But here’s the catch. Not all SAFEs work the same way. Pre-money and post-money SAFEs look similar on the surface, yet they calculate ownership and dilution very differently. Many founders sign them without fully understanding how much equity they are giving away, or how future rounds will amplify the impact. That confusion can quietly reshape cap tables long after the check clears.

This guide breaks down pre-money versus post-money SAFEs in plain terms, showing how each structure affects dilution, investor ownership, and future fundraising dynamics. By the end, you’ll know exactly what you’re agreeing to before you sign.

How SAFEs Started and How They Changed

SAFEs did not start out complicated. The original versions were pre-money SAFEs, where investor conversion was calculated based on the company’s valuation before new money came in. Simple on paper, but messy in practice.

As more investors joined and rounds stacked up, founders often struggled to predict how much ownership they were really giving away. Dilution was happening, but not always in obvious ways. This lack of clarity created tension on both sides of the table.

That problem led to the rise of the post-money SAFE. Instead of guessing outcomes, this structure clearly defines an investor’s ownership after the SAFE converts. Investors know exactly what percentage they will own, and founders get a clearer view of how much dilution they are locking in upfront.

Dilution simply means your ownership percentage goes down when new capital enters the company. The structure of the SAFE determines how predictable that drop will be.

As startup ecosystems matured, SAFEs spread quickly beyond Silicon Valley. Founders in the UK, Singapore, and other global hubs adopted them for one main reason: speed with fewer legal headaches. Their flexibility made them the go-to instrument for early-stage fundraising.

What founders should always do before choosing a SAFE

- Model dilution under both pre-money and post-money structures

- Understand what investors care about most

- Compare outcomes across future funding scenarios

- Choose the SAFE that supports your long-term growth plan

For example, raising $200,000 on a pre-money SAFE can result in very different dilution after a $2 million Series A compared to a post-money SAFE. The difference often surprises founders who did not model it in advance.

SAFEs shape more than just the first check. They influence founder ownership, investor returns, and how future rounds unfold. Understanding how they evolved helps founders choose the structure that protects them over the long run.

Exploring the differences in SAFE agreements is set against the wider context presented in types of startup funding, which examines various financial strategies available to startups. By understanding these foundational concepts, founders can make informed decisions that align with their long-term goals.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

What Makes SAFEs Work: Core Features and Mechanics

SAFEs, short for Simple Agreements for Future Equity, exist for one reason: to make early-stage fundraising faster and less painful. Instead of negotiating a valuation upfront, founders raise capital now and issue equity later, usually at the next priced round.

At their core, SAFEs convert into shares during a qualifying financing event, most commonly a Series A. When that happens, SAFE investors receive equity on more favorable terms than new investors, rewarding them for taking early risk.

There are two main structures founders need to understand: pre-money SAFEs and post-money SAFEs. The difference between them determines how ownership and dilution are calculated once conversion happens.

Most SAFEs include a discount rate, typically between 10% and 25%. This discount lets SAFE investors convert at a lower price per share than incoming investors. For example, if a Series A sets the share price at $1.00, a 20% discount allows SAFE holders to convert at $0.80 per share.

Many SAFEs also include a valuation cap, either pre-money or post-money. The cap sets a maximum company valuation at which the SAFE can convert, protecting investors if the company’s valuation jumps significantly before the next round.

Put simply, the valuation structure determines how much equity is issued, the discount sets the conversion advantage, and the cap limits the upside price. Together, these mechanics shape how dilution plays out for founders and investors alike.

It’s no surprise SAFEs have become the default. In a recent year, they accounted for 64% of seed rounds, far ahead of priced equity at 27% and convertible notes at 10%. Their simplicity hides real consequences, which is exactly why understanding the mechanics matters before signing.

SAFEs vs. Convertible Notes vs. Pre-Money vs Post-Money SAFEs

When comparing SAFEs (Simple Agreements for Future Equity) and convertible notes, the distinctions often come down to simplicity versus structure. SAFEs are designed as straightforward agreements that avoid the complexities of interest accrual and repayment obligations.

Convertible notes are debt instruments with maturity dates and interest rates. These affect cash flow and planning. Recent data spotlights this shift. In Q4 2024, only 9% of pre-seed rounds used convertible notes, while 90% relied on SAFEs. This preference underscores how simplicity shapes funding instrument selection.

One of the most significant differences lies in repayment. Convertible notes require repayment if they don’t convert into equity by the maturity date, potentially creating financial strain for startups. SAFEs, on the other hand, eliminate this obligation, offering founders a more flexible option. Additionally, convertible notes accrue interest over time, which adds to the total amount owed upon conversion or repayment. SAFEs bypass this entirely, making them a cleaner choice for startups focused on equity financing.

The absence of a maturity date in SAFEs further simplifies the process. Convertible notes demand careful attention to deadlines, which can lead to renegotiations or complications if the startup hasn’t raised sufficient funds by the maturity date. SAFEs remove this pressure, allowing startups to focus on growth without looming deadlines.

A closer look at pre- and post-money SAFE terms resonates with the comparative insights found in equity vs debt financing, which analyzes different funding dynamics. This comparison highlights why SAFEs have gained popularity among early-stage startups seeking streamlined funding solutions.

Understanding these differences is crucial for founders aiming to balance investor relations with operational flexibility. While convertible notes offer structured terms, SAFEs provide simplicity, making them an attractive option for startups prioritizing ease and scalability.

How to Choose Between Pre-Money vs Post-Money SAFEs

Current industry data reveals how critical thoughtful scenario planning is. Average pre-seed, pre-money valuations stand at $5.7M, with median slightly lower at $5.3M. Founders modeling SAFE impacts can use these benchmarks to estimate ownership and dilution outcomes more accurately.

Selecting the right SAFE (Simple Agreement for Future Equity) structure requires a careful balance between founder dilution, investor transparency, and long-term funding goals. The decision between pre-money and post-money SAFEs hinges on detailed financial modeling and scenario analysis.

Understanding pre-money vs post-money SAFEs is essential for making an informed choice.

Pre-money SAFEs calculate investor ownership before the valuation of new funding rounds, which can obscure dilution outcomes for founders. Conversely, post-money SAFEs provide greater clarity by factoring in all prior investments, making it easier to predict dilution but potentially increasing founder equity loss. Founders should prioritize rigorous scenario modeling to understand how each structure impacts their equity stake and aligns with future financing needs.

Additionally, investor expectations play a crucial role. Transparent structures like post-money SAFEs may appeal to investors seeking clarity, while pre-money SAFEs might suit those comfortable with less immediate precision. Understanding the subtleties of SAFE agreements aligns with strategies described in balancing equity and debt financing, where managing varied funding approaches is examined.

Managing Pro Rata Rights in SAFE Agreements

This distinction extends to pro rata rights, which allow investors to maintain their ownership in future rounds. Pre-money SAFEs typically grant these rights by default, while post-money SAFEs require a separate side letter to secure them. Founders should clarify pro rata arrangements early to avoid misunderstandings and ensure investor confidence.

Ultimately, the right SAFE structure depends on your startup’s growth trajectory and funding strategy. By analyzing potential dilution outcomes and aligning with investor priorities, founders can make informed decisions that support both immediate and long-term goals.

Risks of Mixing SAFE Types and Convertible Notes

Building on the importance of selecting a single SAFE structure, founders should avoid mixing pre-money and post-money SAFEs or combining SAFEs with convertible notes. This approach introduces complex conversion mechanics that can create significant ownership variances and disputes among stakeholders. Detailed scenario modeling and legal counsel become essential when multiple instruments are involved. Clear communication and cap table transparency help prevent misunderstandings and protect both founder and investor interests.

Why This Decision Matters

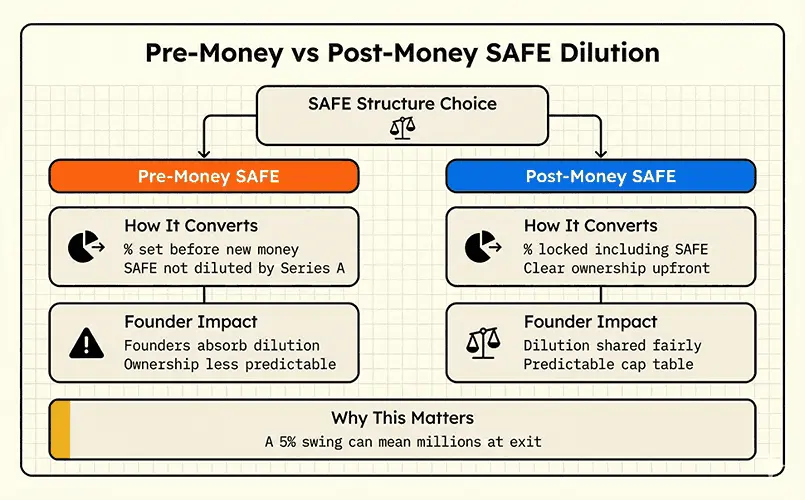

You're raising $500K on a SAFE with a $5M valuation cap. An investor asks: "Is this pre-money or post-money?"

Your answer determines whether you'll own 82% or 77% of your company after your Series A. That 5% difference on a $50M exit? That's $2.5 million.

Most founders sign SAFEs without fully understanding this distinction. Let's fix that.

The Core Difference (With Math)

Let's say you raise $500K on a $5M cap SAFE, then do a Series A at $10M valuation, raising $2M.

Pre-money SAFE:

- SAFE converts to 10% ($500K ÷ $5M)

- Series A investors get 20% of the NEW total ($2M ÷ $10M)

- You end up with: ~72%

Post-money SAFE:

- SAFE converts to 10% of everything including itself

- Series A dilutes everyone proportionally

- You end up with: ~77%

The key: with pre-money, SAFE holders don't get diluted by the Series A. With post-money, they do—just like founders.

Why Pre-Money Dilutes You Twice

Think of it this way: pre-money SAFEs act like they were always part of your cap table. When new money comes in, only you and your co-founders get diluted.

Post-money SAFEs lock in their percentage at conversion. When Series A happens, everyone shares the dilution equally, founders and SAFE holders alike.

This might sound like a small technicality. It's not. The math compounds quickly, especially if you raise multiple SAFEs.

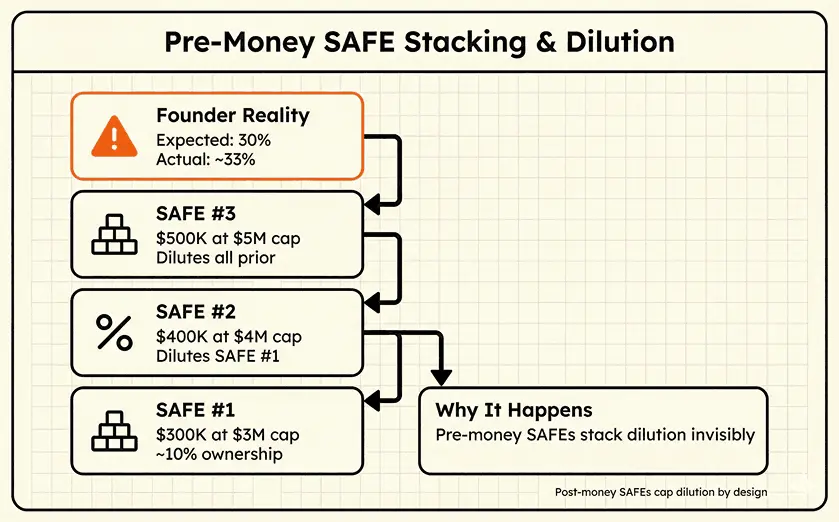

The Stacking Problem

Here's where pre-money SAFEs get dangerous: raise three of them, and each one dilutes all the previous ones.

Example:

- SAFE 1: $300K at $3M cap (10%)

- SAFE 2: $400K at $4M cap (10%)

- SAFE 3: $500K at $5M cap (10%)

You might think you've given away 30%. With pre-money SAFEs, it's actually closer to 33% because each new SAFE dilutes the earlier ones. With post-money, you'd give away exactly 30%.

This "stacking" problem has caught many founders off-guard. Post-money SAFEs solved this by making dilution predictable and capped.

To explore alternative financing options, check out our article on types of debt financing for startups, which offers insights into debt-focused fundraising strategies.

What to Do If Your SAFE Doesn’t Convert

When a SAFE (Simple Agreement for Future Equity) fails to convert, investors may encounter complex scenarios that impact their financial expectations. Without a conversion event, the investment remains unconverted, potentially leaving investors in a precarious position during liquidation.

To mitigate risks, some SAFE agreements include provisions for redemption rights, allowing investors to negotiate repayment under specific conditions. While these measures can reduce losses, they don’t eliminate the inherent uncertainty tied to unconverted SAFEs. This underscores the importance of carefully structuring SAFE agreements to address potential outcomes.

What Investors Think

Early-stage investors often preferred pre-money SAFEs because the economics were better for them. They'd convert at the cap, then watch their percentage grow as the company raised more money. Post-money SAFEs changed that. Now investors' percentages are locked in, they share in future dilution just like founders do.

Y Combinator switched to recommending post-money SAFEs in 2018, and they've become the standard. Most investors now expect them. If someone pushes for pre-money in 2026, ask why.

How to Decide

Use post-money if:

- You're raising multiple SAFEs or notes

- You want certainty about maximum dilution

- You're following current market standards (most likely scenario)

Pre-money might make sense if:

- A single investor insists and the economics still work for you

- You're doing one small bridge with a friendly angel who helped early

Reality check: Unless you have a compelling reason otherwise, use post-money. It's cleaner, fairer, and what most lawyers and investors expect today.

Conclusion

SAFEs may look simple, but the structure you choose quietly determines how much of your company you actually keep. Pre-money and post-money SAFEs do not just change math on paper. They shape dilution, investor dynamics, and how confident you feel walking into future rounds. Founders who model scenarios early avoid surprises later, while those who rush often pay for it at Series A. Understanding these mechanics is no longer optional. It is part of responsible fundraising in today’s market.

If you’re navigating SAFEs, dilution, or early-round structuring, this is the moment to slow down and get it right. Qubit Capital’s fundraising consulting services help founders model outcomes, pressure-test SAFE terms, and approach investors with clarity and confidence. A few informed decisions now can protect years of equity later.

Key Takeaways

- Pre-money and post-money SAFEs calculate dilution differently, and that difference compounds significantly as you raise multiple rounds over time.

- Post-money SAFEs offer clearer ownership visibility, making dilution predictable for founders and easier to explain to investors.

- Mixing SAFE types or combining SAFEs with convertible notes increases cap table complexity and raises the risk of future disputes.

- Most investors now expect post-money SAFEs, and pushing back on structure without modeling can cost founders millions at exit.

- Scenario planning before signing any SAFE is the only reliable way to protect long-term founder ownership.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Frequently asked Questions

What is a pre-money SAFE?

A pre-money SAFE bases conversion on valuation before new investments, affecting how much equity investors receive.