Table of Contents

Private credit and private equity represent two distinct avenues for alternative investments, each offering unique opportunities and risks. While private equity focuses on acquiring ownership stakes in companies, private credit revolves around debt-based financing. Understanding these differences is crucial for investors aiming to align their strategies with their financial goals.

The rapid evolution of private markets is evidenced by recent asset growth. Private credit asset class totaled nearly $2 trillion by the end of 2023, roughly ten times larger than in 2009. This massive expansion spotlights why comparing strategies is essential for today's investors.

This article explores the core contrasts between private credit and private equity, helping investors make informed decisions. Let’s dive into the specifics and uncover actionable insights.

Private Credit vs Private Equity: What You Need to Know

Both asset classes are gaining substantial traction. U.S. private equity deal value increased 19.3% from 2023, reaching $838.5 billion in 2024, with deal count up 12.8% to 8,473. This signals robust ongoing institutional interest.

Private credit and private equity are different approaches to alternative investing. Each has unique characteristics and objectives.The difference between private equity and private credit lies in their investment structure and risk profiles.

The Private credit funds provide direct lending solutions, offering investors predictable returns and flexible investment options. This section explores private credit vs private equity, highlighting key differences for investors

For those already familiar with equity-focused funding methods, a closer look at venture capital vs private equity reveals detailed distinctions that supplement your understanding of how varied investment strategies operate.

The Rise of Hybrid Credit-Equity Strategies

Building on these distinctions, some investment platforms now offer hybrid strategies that blend private credit and private equity elements. These approaches allow investors to access both debt and equity exposures within a single structure, potentially enhancing diversification and risk-adjusted returns. However, hybrid models can introduce complexity, including conflicts of interest and increased opacity. Understanding these integrated strategies is essential for investors seeking to navigate the evolving alternative investment landscape.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

How Assets and Debt Instruments Shape Investments

Private equity focuses on acquiring ownership stakes in companies. It aims for long-term growth through strategic management and operational improvements.

Whereas, private credit emphasizes structured loans and debt instruments, offering investors predictable income streams and reduced exposure to market volatility. Private debt is a key component of alternative investing, offering stable returns and lower volatility. Private equity loans may be used to finance acquisitions or support portfolio company growth.

Private equity thrives on growth potential, often targeting high-growth, privately-owned companies. For instance, over $300 million in invested capital has been deployed to fuel strategic growth for private ventures seeking flexible debt solutions. Meanwhile, private credit prioritizes stability, relying on structured repayment schedules to deliver consistent returns.

Some investors also compare private equity versus investment banking when evaluating asset allocation strategies. Understanding the dynamics of private credit vs private equity allows investors to align their portfolios with their risk tolerance and financial aspirations, whether they seek steady income or transformative growth.

Recent growth in private debt is reshaping investment choices. Private credit is the fastest-growing segment of asset management, with a compound annual growth rate of 20% from 2017 to 2022. This rapid expansion demonstrates how asset allocation priorities are shifting.

Private Credit vs Private Equity: Returns, Risks, and Ownership

Comparing private credit vs private equity helps investors understand returns, risks, and ownership differences.

Understanding the dynamics of private credit vs private equity requires a closer look at how returns are generated, the associated risks, and the ownership structures involved. Each investment type offers distinct advantages and challenges, making them suitable for different investor profiles.

A key difference between private equity and private credit is how returns are generated and the risks involved.

Returns: Predictability vs Performance

Private credit returns are built on predictable interest payments and fee structures. Investors typically receive steady income from loans provided to businesses, with historical yields averaging around 10.1% over the last fifteen years, according to the AAM Report. This consistency appeals to those seeking reliable cash flow.

Private credit risks include borrower defaults and market volatility, which investors must carefully assess.

Private equity, on the other hand, relies heavily on company performance, operational improvements, and successful exit events, such as mergers or acquisitions. Returns can be substantial but are inherently tied to the growth and profitability of the underlying business.

Recent interest rate shifts have amplified private credit's relative return. Private credit investors now benefit from floating yields enhanced by 200–300 basis points compared to the previous decade. This positions private credit as even more attractive for predictable income.

Risk Profiles: Stability vs Volatility

The risks in private credit primarily revolve around liquidity and economic cycles. Borrowers may face challenges during downturns, potentially impacting repayment schedules. However, the structured nature of loans often mitigates extreme losses.

Private equity carries higher volatility, with risks including bankruptcy of portfolio companies or dilution of ownership stakes. While the potential for high returns exists, investors must be prepared for the possibility of significant losses.

A direct comparison of private credit vs private equity reveals important differences in returns and risk profiles.

Ownership: Non-Equity vs Influence

Ownership is a defining factor in distinguishing these investment types. Private credit investors do not hold equity in the companies they lend to, limiting their influence over business decisions. Conversely, private equity investors acquire substantial ownership stakes, granting them a say in strategic decisions and the ability to drive operational changes.

Both private credit and private equity cater to unique investment goals, balancing returns, risks, and ownership dynamics.

Holding Periods and Tax Impacts You Should Know

Private equity investments often stand out due to their longer holding periods, typically averaging a 5.6-year median, which can significantly influence investor tax planning. These extended durations allow gains to be taxed at favorable long-term capital gains rates, offering an attractive advantage for investors seeking tax efficiency.

In contrast, private credit investments are generally held for shorter durations. While this provides quicker liquidity, the returns are taxed at ordinary income rates, which can result in higher tax liabilities. For investors weighing their options, understanding these tax implications is crucial to aligning investment strategies with financial goals.

Private debt investments may also be subject to ordinary income tax rates, affecting net returns.

Highlighting how a 5.6-year median holding period may influence investor tax planning underscores the importance of considering both the duration and tax treatment of investments. By carefully evaluating these factors, investors can make informed decisions that optimize their portfolios for both growth and tax efficiency.

Liquidity preferences are evolving fast. 60–80% of European sponsors’ M&A activity in 2025 was funded by private credit, favoring deals with shorter holding periods and rapid turnover over traditional private equity strategies.

Breaking Down Fee Structures in Private Investing

Fee structures in private investing vary significantly between private equity and private credit, shaping how investors and fund managers share returns. Private equity commonly adopts the “2 and 20” model, where fund managers charge a 2% annual management fee and retain 20% of the profits as performance fees. This structure incentivizes managers to maximize returns but can lead to higher costs for investors.

Private credit, on the other hand, offers more flexibility in fee arrangements. These may include flat fees or performance-based models tailored to specific investment strategies. For example, some private credit funds charge a fixed management fee without performance incentives, while others align fees with portfolio outcomes.

Private credit's popularity and flexible fee arrangements are reflected in fundraising trends. H1 2025 private credit fundraising reached $124 billion, already outpacing the full-year total in 2024. These surges reinforce the ongoing shift toward adaptable fund structures.

Discussion is further enriched by top private equity firms, which presents contemporary examples of industry leaders in the private equity landscape. Understanding these fee models is essential for investors seeking to balance cost and performance in private investing.

Where Your Investments Fit in the Capital Structure

Private equity and private credit play distinct roles within a company’s capital structure, each offering unique benefits to investors. Private equity primarily resides in the equity portion, where investors acquire ownership stakes in businesses. This approach often involves using borrowed capital to enhance potential returns, making it a high-risk, high-reward strategy.

Private equity lenders often structure debt to complement equity investments, balancing risk and return. On the other hand, private credit operates exclusively within the debt component of the capital structure. Investors in private credit provide loans or financing to businesses, generating predictable income streams through interest payments. Unlike equity investments, private credit focuses on stability and lower risk, appealing to those seeking consistent returns.

Late-stage plans need fuel without losing the steering wheel. Growth equity funding explains how minority checks work, what “use of proceeds” investors expect, and where control terms usually land

How to Source and Originate Winning Deals

Deal sourcing is the backbone of successful investment strategies, but the methods vary significantly between private equity and private credit. Private equity firms often rely on personal networks and referrals to identify opportunities, emphasizing the value of established relationships. In contrast, private credit is increasingly turning to technology platforms to streamline origination methods and uncover smaller, niche deals that might otherwise go unnoticed.

For those assessing smaller deals, it’s essential to focus on clear financial metrics and operational transparency. Technology platforms can provide valuable insights into these aspects, enabling investors to make informed decisions. An alternative perspective is provided in the pros and cons of friends and family funding, offering a comparison of more informal capital sources with other structured funding methods.

Applying the Four Cs Framework in Private Credit

- Capital: Assess the borrower’s financial strength and equity base to determine their ability to withstand financial stress.

- Capacity: Evaluate the borrower’s cash flow and earnings to ensure they can meet ongoing debt obligations reliably.

- Collateral: Review the quality and value of assets pledged to secure the loan, which can mitigate potential losses.

- Conditions: Consider the broader economic environment and industry trends that may impact the borrower’s repayment prospects.

By combining traditional networking with modern tools, investors can expand their reach and improve the quality of their deal flow, ensuring a competitive edge in the market.

What Your Investment Team Needs to Succeed

Success in private equity and private credit demands distinct skill sets tailored to their unique challenges. Private equity teams thrive on strategic vision, leadership, and advanced financial modeling. These professionals must identify growth opportunities, optimize operations, and drive value creation across portfolio companies.

Conversely, private credit teams focus on risk assessment and credit analysis. Their expertise lies in evaluating borrower profiles, structuring debt solutions, and mitigating risks in complex financial landscapes. Precision and diligence are critical to ensuring sustainable returns while safeguarding capital.

Building an investment team equipped with these specialized skills ensures adaptability and resilience in dynamic markets. Whether your focus is equity or credit, aligning expertise with strategic goals is the cornerstone of long-term success.

Comparing Career Paths in Private Equity and Private Credit

| Aspect | Private Equity | Private Credit |

|---|---|---|

| Work-life balance | Longer hours, high intensity | More predictable, balanced schedule |

| Skill emphasis | Strategic management, financial modeling | Credit analysis, risk assessment |

| Career mobility | Broader exit opportunities | Specialized credit-focused roles |

How to Manage Your Portfolio Like a Pro

Effective portfolio management requires tailored strategies depending on the asset class. For private equity, active management is the cornerstone of success. It involves driving operational improvements, optimizing business processes, and preparing for lucrative exit strategies. On the other hand, private credit management emphasizes vigilance. Strategic monitoring of borrower performance ensures timely repayments and minimizes risks.

While private equity thrives on growth-oriented interventions, private credit relies on consistent oversight to safeguard investments. Both approaches demand expertise, but their focus areas differ significantly. Understanding these distinctions is key to managing your portfolio like a professional.

Whether you're enhancing operational efficiency or monitoring borrower metrics, mastering these strategies can elevate your portfolio's performance.

The Latest Market Trends Backed by Data

Private equity and private credit markets are evolving rapidly, driven by technological advancements and increasing investor interest. According to the Zion Report, the US private equity market was valued at $416.15 billion in 2023 and is projected to reach $1,055.94 billion by 2032. This growth highlights the sector’s expanding appeal and underscores the importance of data-driven insights in investment strategies.

Private credit, too, is experiencing remarkable expansion. As noted in the KPMG Survey, the asset class has matured significantly, with $1.6 trillion in assets under management. Projections suggest investments in private credit could surpass $3.5 trillion by 2028, reflecting its growing institutional appeal and demand for alternative income streams.

Private credit consistently leads sector growth. Assets under management in private debt surged to EUR 510 billion by December, with an average growth rate of 21.5% over six months. This trend illustrates the velocity of change in alternative lending.

Technology is reshaping these markets. Private equity firms increasingly rely on data analytics to enhance decision-making processes, while private credit investors are adopting machine learning techniques to refine underwriting and risk assessment. This shift toward technology integration is enabling investors to uncover opportunities and mitigate risks with greater precision.

As these asset classes continue to expand, the role of advanced analytics and machine learning will remain pivotal in driving smarter, more informed investment decisions.

Private Credit in Action: Real Case Studies

Private credit strategies often shine brightest when applied to real-world scenarios. Below, we explore three compelling case studies that demonstrate the versatility and impact of private credit solutions, including direct lending, distressed debt restructuring, and mezzanine financing.

Direct Lending: Fueling Growth for a Mid-Market Tech Company

A mid-market technology firm faced a critical growth juncture but lacked access to traditional financing options. Through a direct lending arrangement, the company secured a $15 million loan at a 10% interest rate. This infusion of capital enabled the business to expand operations and invest in new product development, ultimately driving a 25% increase in revenue. This case highlights how this direct lending arrangement offered both capital and flexibility at a crucial growth stage.

Distressed Debt Turnaround: Revitalizing a Manufacturing Company

Distressed debt can often be transformed into opportunity with the right approach. A manufacturing company’s $50 million debt was acquired at a 40% discount, allowing investors to step in and restructure operations. Following the turnaround, the debt was revalued at $60 million, showcasing how proactive restructuring can rapidly boost the underlying value of distressed assets.

Mezzanine Financing: A Catalyst for Expansion

Mezzanine financing, a mix of debt and equity, provides capital for expansion while minimizing ownership dilution. Private credit investment offers flexibility and tailored solutions for businesses in need of non-traditional financing.

For additional insights into practical collaboration considerations, explore our article on working with private equity pros and cons, which examines both the strengths and limitations of partnering with private equity investors.

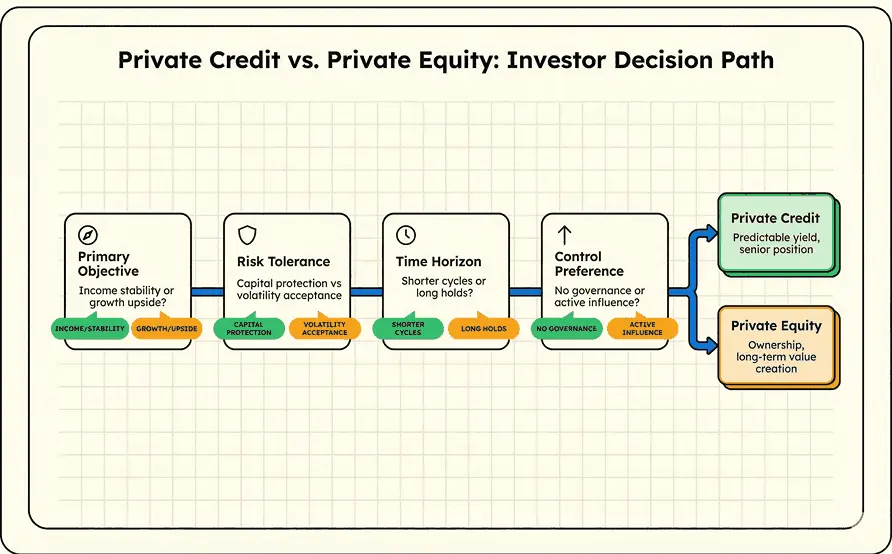

Choosing Between Private Credit vs Private Equity

Selecting between private credit and private equity requires a clear understanding of your investment goals and constraints. Each option offers distinct advantages and challenges, making it essential to evaluate key factors such as eligibility, risk tolerance, expected returns, and holding periods.

- Define goals

- Assess risk

- Review holding period

- Check eligibility

- Research returns/tax impacts

Investors may also weigh private equity versus investment banking when considering their options.

Conclusion

Understanding the nuances between private credit and private equity is essential for making informed investment decisions. Throughout this blog, we’ve explored the distinct benefits and risks associated with each, highlighting their unique roles in portfolio diversification and growth strategies. Recognizing these differences empowers investors to align their choices with financial goals and risk tolerance.

As you evaluate these opportunities, remember that actionable insights are the foundation of successful investments. Whether you’re drawn to the steady income potential of private credit or the high-growth prospects of private equity, a clear strategy is key.

If you're ready to capitalize on these insights, we at Qubit Capital can assist you through our Strategic Acquisition service. Connect with us and explore tailored solutions for your investment journey.

Key Takeaways

- The main difference between private equity and private credit is their approach to investment and risk.

- Private credit focuses on debt-based investing with predictable interest income.

- Private credit meaning centers on providing alternative financing and steady income for investors.

- Private equity relies on ownership stakes for long-term growth and value creation.

- Distinct differences exist in risk profiles, fee structures, and tax implications.

- Investment holding periods and capital structure positioning greatly impact overall returns.

- Market trends highlight the growing importance of technology and data analytics in both sectors.

Find startups worth your time.

Curated startup opportunities matched to your thesis and investment criteria.

- Deal flow filtered by sector, stage, and fit

- Research and context included with every opportunity

- Less noise. More relevant deal flow.

Frequently asked Questions

What are the main risks in private credit vs private equity?

Private credit risks include default and liquidity, while private equity faces market, operational, and valuation risks. Understanding these is key for investors.