Table of Contents

Investors who consistently source high-quality founders from incubators and accelerators don’t just show up on demo day, they build relationships with program managers, map their thesis to specific programs, and run a disciplined triage and follow-up process that converts signal into meetings and diligence.

To find promising startups, target programs aligning with your investment thesis, engage early with founders, and use structured follow-up methods.

Startup accelerators play an increasingly pivotal role in early-stage growth. As of 2024, accelerator graduates’ survival rate is 23% higher than other new businesses. This performance advantage underscores why outreach to such programs is essential for investors aiming for sustained returns.

This guide explains how incubators and accelerators differ, how to target the right programs, what to watch for in cohorts and demo days, how to run fast follow-ups, and how to measure ROI from this channel across a quarter.

How to Find Startups Through Accelerators vs. Incubators

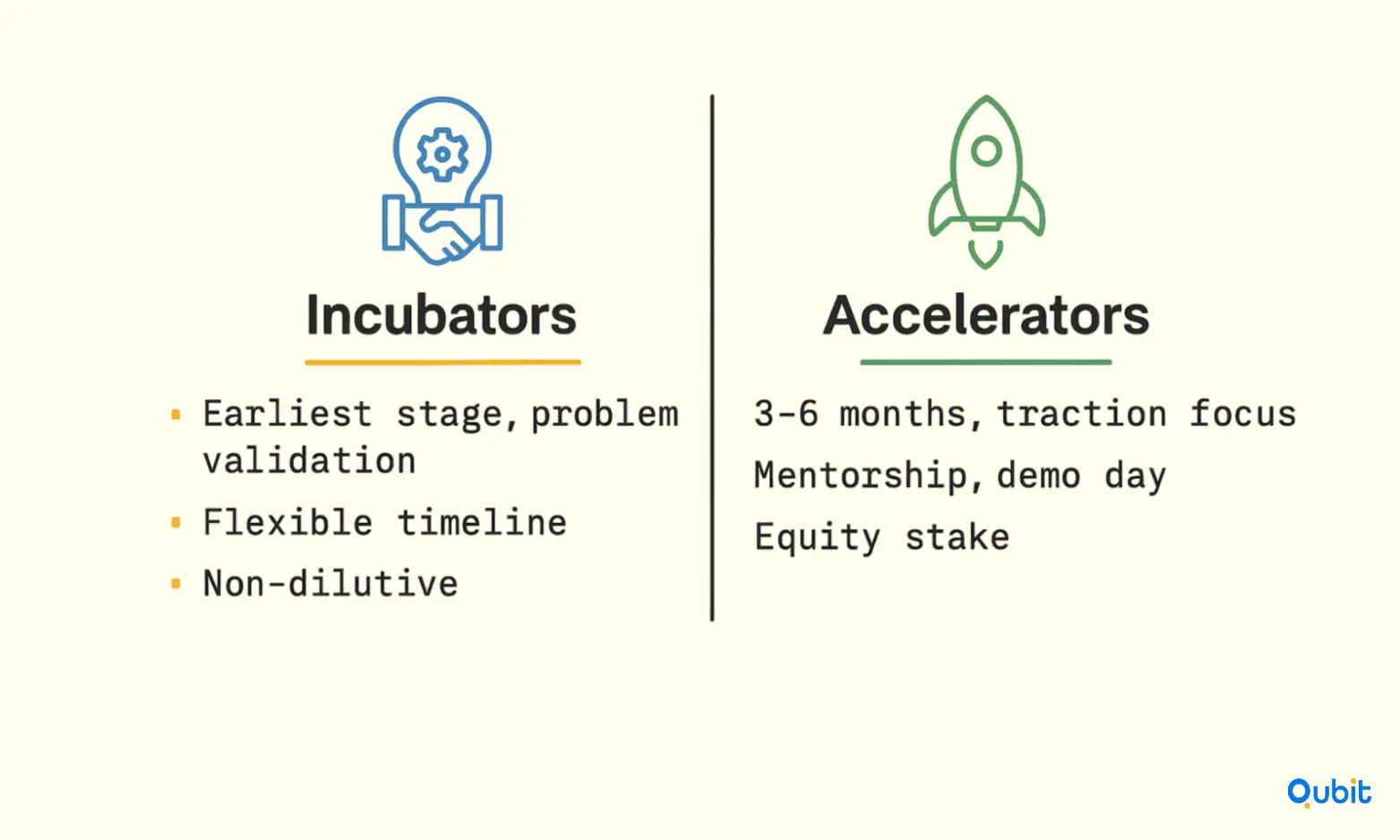

Incubators support pre-product teams. Accelerators support product-ready teams with set program length. While both an incubator for startups and an accelerator support founders, there are key differences that affect how investors should approach them:

- Incubators focus on the earliest startup stages. Sometimes, this work begins before a product exists. They emphasize problem validation, early product development, and business model shaping over a flexible timeline. Funding is less common, and the model may be Non-dilutive (no equity taken from founders) programs.

- Accelerators are structured and time-bound, typically 3–6 months. They admit teams with a product and some traction, deliver intensive mentorship, and typically end in a demo day or investor showcase. Many also invest a small seed amount in exchange for equity.

Practical implication: Investors seeking earlier discovery of technical or research-driven teams will benefit from incubator relationships, while those focused on ready-to-scale companies should prioritize accelerator cohorts and demo-day funnels. Your investment approach gains broader context through insights on how to do startup outreach for investors, which align with the wider tactics used in startup outreach.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

Targeting the Right Programs

To maximize how to find startups through accelerators, align your thesis with the right programs by stage, sector, and geography. Build a short list of 10–20 startup incubators or accelerator programs that repeatedly graduate on-thesis companies and maintain a consistent cadence of communication with their directors. Prioritize:

If you're wondering how to find investors or accelerator programs for tech startups, focus on university-linked programs with strong spinout or IP commercialization track records, where the program team is motivated to help investors and founders connect.

- Sector-aligned accelerators for startups (e.g., fintech, healthtech, climate) whose programming and mentors match the buyers and regulatory realities of the thesis.

- Regionally strong ecosystems (e.g., Europe via Dealroom-tracked hubs) where accelerators partner with corporates and public bodies for pilot access and market entry.

- University-linked incubators and corporate incubators that mature research-to-venture commercialization or spin-outs, often with distinct IP and regulatory depth.

| Criteria | Example Questions to Ask |

|---|---|

| Stage Fit | Does this program recruit teams pre-product or post-revenue? |

| Sector Alignment | What share of your cohorts matches my investment thesis? |

| Geographic Reach | Where do most founders you serve operate? |

| Alumni Outcomes | How many portfolio companies closed significant rounds post-program? |

| Post-Program Value | Do you maintain an alumni network with ongoing investor introductions? |

A working map should cover stage fit (incubator vs. accelerator), program length/cadence (rolling vs. 3–6 months), funding model (equity vs. fee vs. non-dilutive), demo-day format (in-person vs. virtual), and post-program alumni engagement (introductions, office hours, partner showcases). For instance, a review of startup databases naturally includes investor tips for startup demo days, which enriches the narrative with practical examples from industry events.

Global programs drive competitive selection. In 2024, AWS Generative AI Accelerator cohort chose 80 startups from 4,700+ applications across 129 countries. This scale reflects both the diversity and intensity of modern accelerator pipelines.

Building Relationships with Program Teams

Program managers and Entrepreneurs in Residence (EIRs) are critical partners: they know which teams are execution-ready, which need time, and which are quietly outperforming. Offer specific value that aligns with your thesis:

- Host short workshops on pricing, enterprise security posture, or pilot-to-paid conversions (aligned to your sectors).

- Volunteer for targeted office hours before demo day (screened for your thesis fit) to help founders problem-solve and to identify high-signal teams early.

- Share a transparent “what we invest in” rubric, stage, check size, reserves, buyer context, so program staff route the right founders your way.

This “give first” posture compounds trust and ensures your outreach after demo day is welcomed rather than generic.

How Programs Select Startups (and Why That Matters)

Understanding selection criteria helps predict cohort quality and match diligence to program signals. Common filters include business model viability (credible path to revenue), uniqueness of product/insight, team capability, and market demand, assessed through applications, interviews, and due diligence stages.

Selection rigor drives result quality. In 2025, Financial Health Network exit rate reached 52.63%, the highest among U.S. accelerators. This extraordinary performance links directly to transparent, disciplined selection methods.

An accelerator program also optimizes for scalability and speed, given the short program timeline.

Engaging During the Program

Many investors overlook mid-program engagement opportunities, which can deliver higher ROI than demo day alone.

Useful touchpoints:

- Private mid-program check-ins: Invite selected founders for informal 1:1s to discuss progress and challenges

- Thematic pitch sessions: Participate in smaller, sector-themed pitch nights or workshops

- Beta customer connections: Offer introductions to potential customers in your network while the founder is refining their GTM motion

Direct involvement helps you assess execution quality and market feedback in real time, not just through a polished final pitch.

Engage Mid-Program Where Learning Is Highest

The highest-fidelity signals appear during the messy middle of a program, not at polished endpoints. Join mentor sessions and office hours to watch how teams frame problems, handle objections, and prioritize tradeoffs. Short, structured 1:1s, 10 to 15 minutes with a clear prompt, reveal whether founders are learning from customer conversations, converging on a wedge, and sequencing milestones realistically. Offering a single design-partner intro or a lightweight compliance checklist at this stage provides practical value and creates a natural reason to check back in two weeks, turning casual interest into a momentum thread grounded in progress rather than pitch polish.

Leveraging Alumni Networks for Persistent Deal Flow

Building on mid-program engagement, investors should actively tap alumni networks for ongoing deal flow. Alumni often become repeat founders, advisors, or connectors, providing access to new opportunities and market insights. Maintaining relationships with alumni enables investors to identify “now ready” companies that may not have been a fit during the initial cohort. This approach ensures a continuous pipeline of high-quality startups and strengthens long-term founder support.

Use Cohort Pipelines and Alumni Networks as Persistent Deal Flow

Think beyond a single batch. Maintain a living tracker of current cohorts and alumni by program, tagged by sector, stage, geography, and buyer context, with short notes on traction and next catalysts. Revisit this tracker monthly to identify companies that have crossed from “too early” to “on-thesis now.” Alumni ecosystems are especially strong sources of second looks and quiet risers who skipped demo day or matured post-program. A recurring office-hours slot for alumni, narrowly scoped to the thesis, keeps a steady stream of relevant founders in view without event-driven spikes.

Treat Demo Day as a Triage Moment, Not the Strategy

Demo day is useful, but it isn’t the strategy. Arrive with a pre-sorted shortlist and a simple, consistent rubric for fit and urgency so follow-ups are decisive and respectful. The real edge is the groundwork laid before the event and the disciplined follow-through after it. Keep asks small and specific in the first 24 hours, one artifact or a 15–20 minute call with a named objective, so founders can respond quickly while handling broader interest.

Calibrate Diligence to Program Rigor and Segment Reality

Programs vary widely in screening depth and mentor quality; adjust the evidence bar accordingly. University-linked incubators and corporate accelerators often have stronger technical or regulatory scaffolding but slower commercial cycles; sector-specialist accelerators may show faster GTM proof with clearer access to buyers.

This diligence process requires investors to look beyond program brand reputation and focus on cohort quality. Overreliance on brand can lead to missed opportunities or misjudged risk, as not all cohorts deliver consistent results. Evaluating actual founder progress and program outcomes ensures more accurate investment decisions. Prioritizing substance over brand helps avoid common pitfalls in sourcing high-potential startups.

In regulated markets, diligence should focus early on validation pathways, standards participation, and procurement hurdles; in workflow SaaS, prioritize proof of repeatable adoption and clear time-to-value in the buyer’s process. Align what is asked and when to the program’s context so diligence is efficient and fair.

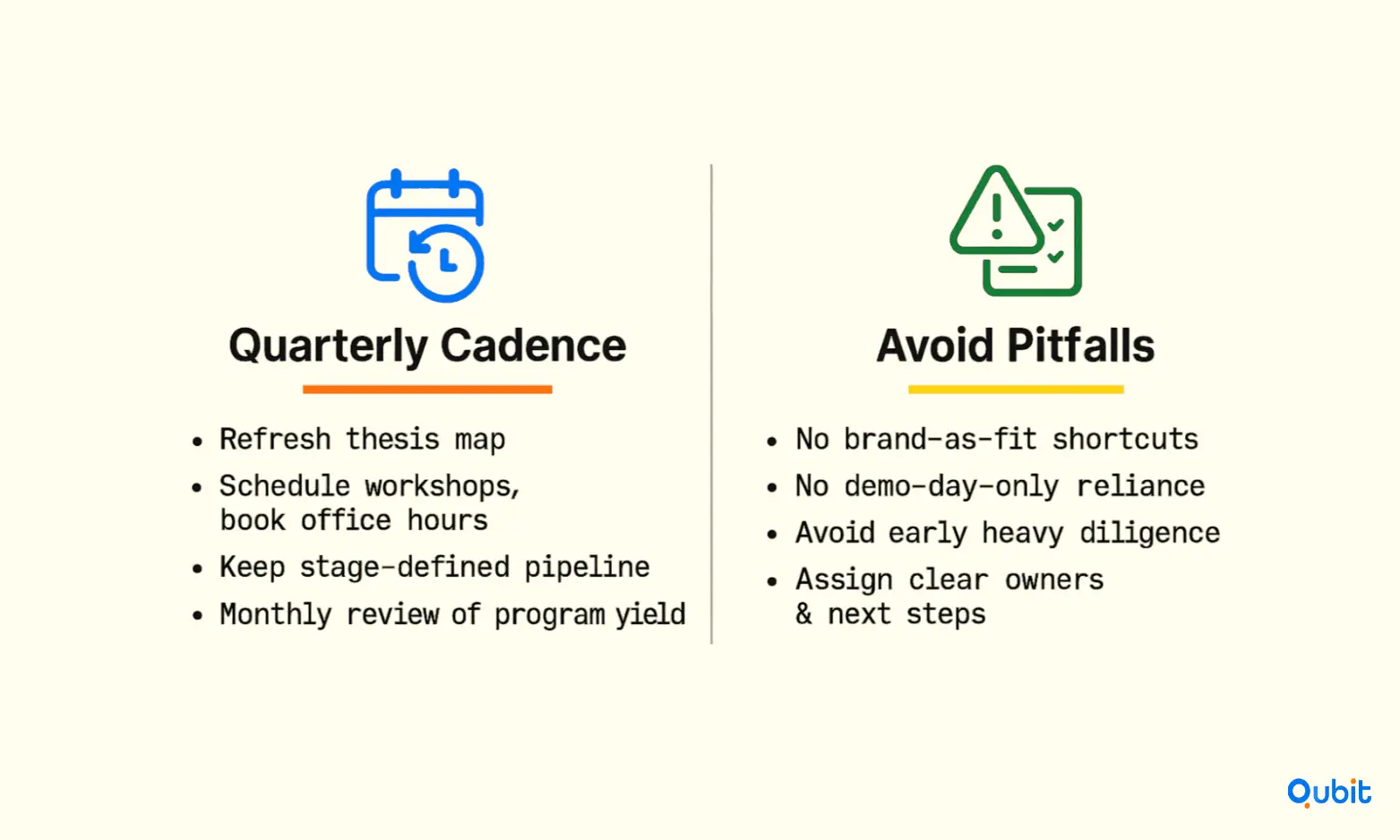

Operationalize Follow-Through Across a Quarter

When considering how to find startups through accelerators, remember that sustained results come from an operating cadence, not heroics.

Quarterly Planning

Set clear objectives at the start of each quarter by identifying which accelerators and programs align with your investment thesis. Define specific targets around deal flow volume, engagement benchmarks, and partnership goals. Assign ownership across your team and establish measurable outcomes so that planning translates directly into consistent, repeatable action throughout the quarter.

Pipeline Management

Keep a simple, stage-defined pipeline for incubator deal sourcing and program-sourced companies with dedicated owners and SLAs so promising threads don't die in private inboxes. Track each opportunity from initial contact through to due diligence, ensuring visibility across the team and preventing high-potential leads from slipping through the cracks during busy periods.

Monthly Reviews

Revisit your pipeline and engagement data monthly to assess what is working and what needs adjustment. Evaluate which programs are yielding on-thesis conversations, which outreach efforts are generating the strongest engagement, and where deepening activity next quarter will deliver the greatest return on your time and resources.

- Which programs yield on-thesis conversations?

- Which offers generate the best engagement?

- Where should you deepen activity next quarter?

What To Avoid

Common failure modes are predictable: treating program brands as proxies for fit; relying on demo day to do the work of relationship building; asking for heavy diligence artifacts too early; and letting interest cool because there is no owner or time-boxed next step. Each of these erodes credibility and reduces the likelihood of competitive allocations when the company raises.

How Accelerators and Incubators Create Investable Startups

1. Corporate Accelerator with Paid Pilots

Some corporate-run accelerators are structured around executing paid pilots rather than generic mentorship. In these programs, corporates present specific problem statements, startups are matched to those needs, and pilots are resourced with clear success criteria on both sides. This compresses the timeline from introduction to real customer validation, giving participating startups credible proof of product-market fit that accelerates both fundraising and commercial traction post-program.

2. University Spinout Ecosystems

University incubators paired with dedicated spinout funds have significantly increased both the volume and quality of investable companies. When universities launch backing funds alongside their incubator programs, the number of spinouts can grow dramatically, from single digits to dozens annually. This model creates a consistent, thesis-aligned pipeline of deep-tech ventures, often culminating in meaningful exits and public listings over time.

3. Investor Approach to Both Models

Investors targeting near-term commercial evidence should prioritise accelerators that commit to scoped, resourced pilots with defined outcomes. For deep-tech and research-led ventures, building direct relationships with university tech-transfer teams and incubator leads provides early access to strong pipelines before companies enter broad fundraising rounds, improving deal flow quality across the board.

Conclusion

Finding strong startups through incubators and accelerators is not about chasing logos or showing up on demo day with a full inbox and no plan. The real advantage comes from treating programs as long-term sourcing partners, engaging founders early, and running a repeatable operating cadence across quarters.

Investors who align their thesis to the right programs, contribute value during the program, and follow up with discipline consistently see higher signal and better conversion into diligence. Incubators unlock earlier technical insight, accelerators surface execution-ready teams, and alumni networks extend value well beyond a single cohort.

When relationships, timing, and process work together, accelerators stop being events and start becoming durable deal flow engines.

Now is the time to act on these insights. If you're looking to secure the right investors, our Investor Outreach service at Qubit Capital can connect you with promising leads. Let’s take your demo day strategy to the next level.

Key Takeaways

- Target programs by thesis, buyer context, and alumni outcomes—not brand alone.

- Build real relationships with program staff through specific, founder-helpful offers.

- Engage mid-program to observe learning velocity and wedge formation.

- Maintain a living tracker for cohorts and alumni to catch “now ready” windows.

- Treat demo day as triage; the edge is pre-work and disciplined follow-up.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Find startups worth your time.

Curated startup opportunities matched to your thesis and investment criteria.

- Deal flow filtered by sector, stage, and fit

- Research and context included with every opportunity

- Less noise. More relevant deal flow.

Frequently asked Questions

How do you align investment thesis with startup incubator programs?

Align your investment thesis with startup incubator programs by prioritizing those that match your sector, stage, and geography focus. This ensures higher quality and relevant deal flow.