Table of Contents

Mobility startups are quietly rewriting how the world moves. From next gen EV fleets and micro mobility platforms to AI driven logistics, smart infrastructure and urban air mobility, this ecosystem is turning transportation into a software and data problem, not just a hardware one.

Recent funding cycles show how fast capital is catching up. Global mobility investment has jumped by roughly 10 billion dollars in a single year, lifting total funding to about 54 billion dollars. That kind of spike signals clear investor conviction and a flood of new entrants competing for larger, more complex rounds.

Sustainability pressure, crowded cities and rapid tech convergence are pulling money into the sector, but they also create brutal filters on who actually gets funded. As investor interest rebounds and public incentives shift, founders now have to navigate a fundraising environment that is multi dimensional, data heavy and unforgiving of fuzzy stories.

This blog aims to provide actionable insights and strategies tailored to mobility startups, addressing the unique hurdles they face in attracting investors.

Let’s jump right in to explore practical approaches, integrated platform features, and innovative solutions for successful fundraising in this evolving landscape.

A Sector on the Move: Fundraising for Mobility Startups

Since 2010, investors have funneled almost US$950 billion into about 3,800 future-mobility startups. This sustained capital flow underpins ongoing breakthroughs and reflects investor confidence in sector resilience. Mobility startups can secure funding by combining strong ESG credentials, clear business models, and leveraging new capital sources such as VCs, CVCs, and government grants.

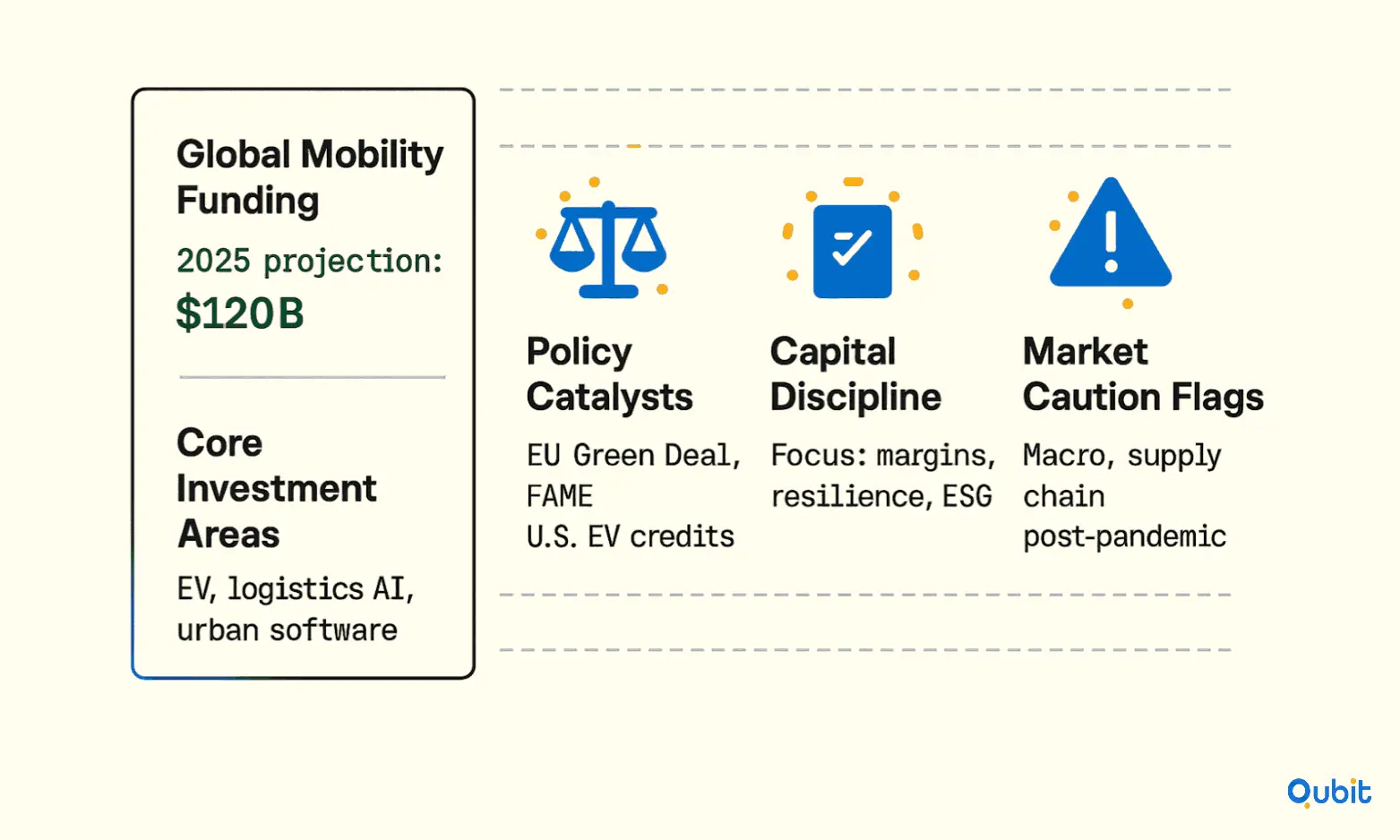

Global investment in mobility startups is projected to top $120 billion in 2025. This surge is led by large funding rounds in EV, logistics AI, and related platforms.

Major Investment Drivers

For those analyzing macro-level funding dynamics, a comprehensive analysis of sector funding dynamics is enriched when you consider mobility VC funding trends, which offer insights into evolving investment patterns.

Shifting Investor Priorities

The era of easy money for “growth at all costs” is over. Today’s VCs and CVCs want:

- Sustainable unit economics: asset utilization, customer payback, fleet churn, and lifetime value

- Clear regulatory and compliance roadmaps

- Proprietary data or platform moats (e.g., networked vehicles, unique routing or mapping IP)

- Evidence of “government as customer or partner”

- Pathways to resilience in supply, workforce, and infrastructure

A detailed assessment of investment behavior is complemented by discussions on mobility VC risk appetite, which sheds light on shifts in investor preferences toward established platforms.

The Role of Sustainability, ESG, and Social Impact in Modern Fundraising

As governments, cities, and global investors double down on decarbonization and social equity, evidence-based ESG credentials are now a fundraising prerequisite, especially in mobility. Most investors now require startups to report on ESG factors as part of standard diligence. This includes lifecycle emissions, labor practices, and accessibility. Additional requirements may include auditor verification and compliance documentation.

Grants and Impact-Linked Capital:

Startups that can quantify their positive impact, lowering emissions per passenger-mile, improving accessibility for disabled or low-income users, or supporting workforce diversity, are better positioned for non-dilutive grants, concessionary loans, and blended finance (public-private) structures. Highlight case studies, impact dashboards, or letters from advocacy groups as social proof.

Brand Advantage:

Demonstrable ESG and community outcomes can also create moat effects, winning city contracts, derisking partnerships with corporates or agencies, and winning over both end-users and potential acquirers concerned with reputational risk.

Capital Sources for Mobility Startups: What’s Changed in 2025

Fundraising for mobility startups in 2025 involves navigating new capital sources and investor expectations.

1. Venture Capital: New Hot Spots and Realities

Mobility-specialist VCs, climate tech funds, and generalist growth funds are back in force, but with sharper focus:

- Stage-Specific Dynamics: Pre-seed and seed rounds see average raises of $1–4M, with larger initial checks for hardware-heavy ventures ($5M+ not uncommon if IP is strong). Series A often centers on $8–25M, with global funds (e.g., Eclipse, Trucks VC, Energy Impact Partners) looking for proven pilots and data flywheels.

- Focus Sectors: EV infrastructure, shared micromobility, fleet SaaS, e-bike manufacturing, commercial AV (autonomous vehicles), logistics AI, battery recycling, and “mobility as a service” (MaaS) platforms attract the most capital.

- Investor Sweet Spot: Traction, paying users, city contracts, data partnerships, or logistics customers, matters as much as tech. Fundable pitches connect immediate pain (traffic, emissions, cost) to recurring, scalable markets.

2. Corporate Venture Capital (CVC): Strategic is the New King

OEMs (Original Equipment Manufacturers), utilities, telcos, and energy giants are doubling down on CVC arms:

- What They Want: Strategic alignment—how does a startup bolster their ecosystem, services, or platform? Ford, Hyundai, Shell, Siemens, and SoftBank, among others, now lead or syndicate rounds.

- Upside: Access to infrastructure, distribution, manufacturing, regulatory relationships, and government ties.

- Risk: CVC money can come with IP restrictions, exclusivity, or “right of first refusal” clauses; negotiate carefully to avoid limiting future growth or partnership options.

3. Government and Non-Dilutive Funding: Cash Without Equity

National and municipal governments, spurred by climate policy and urbanization, are opening checkbooks for:

- Pilot grants (e.g., smart scooter schemes in Paris or India’s electric bus pilots)

- Tax credits and rebates (for fleets, charging deployments, R&D)

- Zero-interest loans or guarantees (battery innovation, supply chain localization)

How to win: Position yourself as solving regulatory pain points (emissions, congestion, last-mile delivery, multimodal access), build city relationships early, and be ready for robust compliance and reporting.

4. Family Offices, Project Finance, and Alternative Capital

Ultra-high-net-worth families and infrastructure/project capital providers increasingly back hardware-heavy mobility startups.

- Family offices are more patient and often values-driven; approach as strategic partners.

- Project finance is key as ventures mature (charging networks, battery gigafactories, fleet scaling).

- Revenue-based financing and asset leasing are on the rise; these can be smart for capital-intensive, hard-asset mobility plays with predictable utilization.

5. Accelerators, Challenges, and Open Innovation

Top accelerators (e.g., Urban-X, Techstars Mobility, Plug and Play, Y Combinator) offer not just funding, but customer access and piloting environments. Innovation challenges from automakers, cities, and infrastructure players can yield both cash and credibility.

Tip: Even if equity-free, participation can be resource-intensive; prioritize programs that offer real customer pilots, data, or partnerships over generic mentorship.

To ensure readiness for investor scrutiny, refer to the mobility startup investor due diligence checklist, which outlines key aspects of financial and legal preparedness.

Leveraging Investor Matching Platforms for Fundraising Success

Building on these capital sources, founders should leverage investor matching platforms to streamline fundraising. These platforms allow startups to filter investors by stage, sector, and geography, improving outreach efficiency. Using targeted profiles increases the likelihood of securing capital from investors aligned with mobility innovation. This approach helps founders avoid wasted effort and accelerates connections with strategic partners.

To demonstrate ecosystem vibrancy, Europe’s largest mobility startup platform now reaches 1,300 members. This network effect strengthens collaboration and amplifies capital access opportunities for founders.

Fundraising Stages and Milestone Planning for Mobility Startups

Stage 1: Pre-Seed & Seed

Hallmarks:

- Prototype demonstrated or pilot underway

- 2–10 FTE team, with clear domain expertise (engineering, policy, logistics)

- First city, customer, or B2B discovery underway

Capital Sources:

- Micro-VCs, angels, mobility vertical specialists, university funds, government startup grants

Key Metrics:

- MVP, first fleet or pilot data

- LOIs (letters of intent) from municipalities or commercial users

- Early evidence of unit economics: cost per mile, downtime, acquisition cost, utilization

- IP filings, unique supplier or data agreements

Stage 2: Series A

Hallmarks:

- Multiple pilots or geographies; first revenues

- Strong partnerships (city, OEM, infrastructure)

- Defined regulatory/compliance plan

Capital Sources:

- Sector-focused VCs (Eclipse, Trucks, Autotech Ventures)

- Corporate investors (OEMs/energy/utilities)

- Government-backed growth programs

Key Metrics:

- Fleet/data scale (thousands of rides, vehicles, packages, or users)

- Retention, recurring revenue, fleet utilization

- Cost and margin trends, path to profitability per unit

- City/end-customer testimonials

Stage 3: Series B & Beyond

Hallmarks:

- Multi-market, multi-modal deployment; “platform” status

- Integration with smart city or logistics networks

- Clear hardware, software, and service verticals

Capital Sources:

- Global growth VCs, sovereign funds, late-stage CVC, cross-border funds

- Project finance for infrastructure (batteries, depots, gigafactories)

- M&A interest from Big Tech, OEMs, or logistics giants

Key Metrics:

- Revenue >$10M, annualized; robust gross margins or clear path

- Unit economics scale with growth

- CRM, maintenance, data, or software platform cross-sell/upsell metrics

- ESG compliance documentation (emissions reductions, accessibility, safety)

Challenges Specific to Early-Stage Startups

Early-stage startups in the mobility sector now face a far tougher fundraising environment than even a few years ago. Investors, still wary from recent market turbulence, are increasingly risk-averse, with capital consolidating around mature ventures and proven business models.

Key hurdles include:

- Reduced Seed and Pre-Seed Funding: Many traditional early-stage investors have shifted focus to follow-on rounds, resulting in a noticeable dip in seed and pre-seed deals.

- Proof Over Promises: VCs today expect a working prototype, active pilots, or signed letters of intent — even at the earliest stages. Simply having ambitious slides no longer suffices.

- Startups in non-urban regions: face limited pilot opportunities

- Deep tech models: may encounter regulatory ambiguity

Strategies to Stand Out:

- Build credibility by partnering with universities for pilots or lab testing.

- Engage in founder networks and accelerator programs that offer warm introductions to early-stage backers.

- Focus messaging on capital efficiency: demonstrate a clear link between limited initial funds and meaningful milestones.

- Highlight founder resilience and adaptability, investors are looking for tenacious teams able to navigate inevitable setbacks.

The Perfect Mobility Pitch: Crafting a Winning Narrative

Crafting a winning narrative is essential for fundraising for mobility startups aiming to attract top investors. Mobility investors want concise, data-backed, and future-proofed storytelling. Here’s how best-in-class startups structure their pitch:

Open With the Macro Tension

Frame the urgent global or urban problems you solve: traffic congestion, emissions, e-waste, unequal access, or crumbling transit. Articulate the market inflection, a regulatory change, new tech breakthrough, or customer demand shift, that makes now the moment to act.

Prove Practical Traction

Don’t just demo cool tech, show deployment, pilots (“we’ve moved 1.2M riders in 16 months”), customer ROI, and user enthusiasm. Videos, real-time dashboards, or press headlines win where jargon loses.

Quantify Your Moat

Is it data? A multi-city network? Proprietary mapping or fleet optimization? A unique policy relationship? Be specific about what keeps copycats out and what grows over time.

Show Unit Economics and Capital Efficiency

Savvy investors know mobility can burn cash. Break down cost structure (hardware, energy, ops, maintenance), revenue streams, and path to breakeven. Show how margins improve—don’t just chase volume for its own sake.

Highlight Regulatory Foresight and Social Value

Demonstrate anticipatory, not just reactive, compliance, data privacy, safety, emissions reporting. Show community engagement, city partnerships, and accessibility (wheelchair, low-income, etc.) as value drivers, not “PR.”

Team: Mission Meets Grit

Spotlight founders’ track records (urban innovation, autonomy, supply chain, fleet management). Reference relevant advisors (ex-OEM, policy leaders, logistics experts). Culture and speed of learning matter as much as technical chops.

Crystalize the Ask

Close by connecting your ask, stage, amount, and use of funds, to the next major milestones. E.g., “$10M will fund 2,000 additional EVs, double our smart dock coverage in Berlin, and reach positive unit economics in 18 months.”

Corporate Partners, Customers, and Strategic Alliances

1. Forging OEM and Infrastructure Partnerships

Early alignment with vehicle manufacturers, battery providers, and grid operators is essential. Winning startups approach these relationships not only for funding, but to secure:

- Early access to vehicles, parts, and repair networks

- Data sharing and integration, fueling platform or SaaS layers

- Co-branded pilots and PR wins

Be aware of exclusivity clauses, non-competes, and switching costs that could hinder future agility.

2. Selling to Cities and Transit Authorities

Government customers are often slow, but hugely influential. Land a city trial and you gain credibility with investors and competitors alike.

Best practices:

- Speak their language: Public safety, equity, sustainability, economic resilience, congestion reduction.

- Build relationships before RFPs: Engage in urban mobility working groups, hackathons, and policy roundtables.

- Demonstrate regulatory readiness (permits, insurance, accessibility, data localization).

3. Strategic Channel Partners

For B2B/enterprise mobility (e.g., fleet AI, last-mile logistics, EV charging management), strategic channel partnerships are ideal for scaling distribution without building direct sales teams in every market.

Government Incentives and Non-Dilutive Funding

Understanding What’s Available

Governments, especially in the EU, India, China, and North America, are pumping billions into mobility innovation through:

- Pilot and deployment grants (urban air mobility, green logistics, e-bike fleets, AV pilots)

- R&D and commercialization grants (battery chemistry, EV manufacturing, smart charging)

- Loan guarantees and tax breaks (facility buildout, fleet conversion, hiring)

- Open data access for smart mobility platforms

How to Win

- Track RFPs and open calls: Most cities and agencies announce competitive opportunities on schedules—plan ahead.

- Collaborate for scale: Form consortia with OEMs, research orgs, and other startups to present a broad solution.

- Get the right paperwork: Compliance, environmental assessments, insurance, and data privacy processes take time.

- Use government wins in your narrative: Each grant or pilot increases investor confidence and can accelerate private funding.

Role of New Funding Mechanisms

Beyond VCs and debt, innovative funding structures are on the rise:

- Tokenization: Startups are experimenting with blockchain-based asset tokenization to finance shared fleets or infrastructure.

- Crowdfunding: Equity and debt crowdfunding, when pursued via credible platforms, can unlock retail investor appetite for mobility projects.

- Impact Grants and Carbon Credits: Funding linked to achievement of emissions reductions or specific social KPIs is an expanding resource, especially for startups with verifiable metrics and impact dashboards.

Global Fundraising Dynamics: Geographic Perspectives

North America

U.S. and Canadian mobility funding is still driven by massive urban markets and public/private infrastructure investment. California, New York, Toronto, and Austin are “super nodes” of both VC and CVC activity. Government policy (federal and state incentives, climate compacts) lowers risk for both founders and VCs.

Europe

Europe’s Green Deal and aggressive urban policy (ultra-low emission zones, e-bike/scooter programs, congestion charging) make EU a global leader in grant-rich, compliance-heavy scaling. Berlin, Paris, London, Amsterdam, and Stockholm are hotbeds for both public and private mobility capital.

APAC

China and India are enormous growth engines, with government-mandated localization (production, supply chain) and aggressive city innovation schemes. Southeast Asia is emerging for shared mobility, e-logistics, and micro-transit—with both family office and government investment.

MENA & LATAM

The Middle East is rapidly onboarding new transport modes (autonomous, shared), often via mega-city developments. Latin America is a growth lab for affordable, accessible two- and three-wheel mobility, supported by a mix of corporate and multilaterals.

Managing Investor Relationships and Board Expectations

Institutionalizing Investor Updates

- Establish monthly or quarterly reporting on KPIs, wins, operational issues, and upcoming capital needs.

- Include a dashboard for utilization, customer growth, geographic expansion, and compliance status.

Handling Strategic Pivots

Be proactive with bad news (delays, regulatory change, supply chain issues), not reactive. Bring solutions and alternate scenarios, not just problems.

Planning for Follow-On Rounds

Refine your “use of funds” narrative at each stage: Tie every new capital raise to specific, value-creating milestones (e.g., “Round will fund Paris, Munich, and Stockholm launches and platform v2.0”). Build FOMO by nurturing multiple investor relationships and leveraging public win announcements.

Exit Pathways and Secondary Markets for Mobility Startups

Mobility’s exit landscape is evolving, providing both rich possibilities and extra complexity for founders and investors aiming for long-term returns.

M&A Landscape:

Traditional auto giants (e.g., Ford, GM, Toyota), global tech leaders (Apple, Amazon, Google), logistics operators (DHL, FedEx), and urban consortiums are now the most common acquirers of mobility startups. Recent years have also seen private equity and sovereign funds step into both growth-stage investments and full buyouts, particularly for infrastructure-heavy players.

SPACs and IPOs:

The initial wave of mobility SPACs (special purpose acquisition companies) generated headlines but mixed long-term outcomes. Pure-vehicle plays (e.g., e-scooters, EV OEMs) often struggled post-listing due to thin margins and operational volatility. However, software or platform-driven mobility firms with robust network effects, SaaS margins, or hybrid recurring business models continue to appeal to public investors, especially when bolstered by anchor transit contracts or large B2B clients.

Employee Liquidity and Secondary Share Sales:

As cycles lengthen, early employees and founding teams increasingly seek liquidity through secondary sales, before full exit or IPO. Investors now routinely scrutinize cap table cleanliness, share transfer restrictions, vesting schedules, and internal buyback clauses well before agreeing to fund or complete a buyout. Transparency and pre-emptive planning can prevent closing delays.

Debt, Private Credit, and Rescue Buyouts:

The rise of asset-backed lending, venture debt, and structured credit offers new tools for cap table management and interim liquidity, especially as late-stage VC funds get more selective. Founders should weigh debt’s impact on burn, board control, and exit flexibility, consulting both legal and financial advisors before layering new liabilities onto growth-stage rounds.

Detailed Risk Factors

Mobility is high reward, but also high risk. Recent years have seen high-profile failures as well as quiet shutdowns. Lessons learned include:

- Regulatory Inevitability: Over-reliance on government incentives caused some EV startups to collapse when subsidies shifted or expired.

- Supply Chain Vulnerabilities: Startups lacking local or diversified supply sources stalled during global disruptions.

- Pivot Points: Some ventures found success only after significant business model pivots, such as shifting from B2C micromobility to B2B fleet solutions.

Risks of Equity-Only Funding Strategies

These lessons show the risks of relying solely on equity funding for mobility startups. Over-dependence on equity rounds can lead to excessive dilution and limited runway flexibility. Diversifying capital sources, including grants and debt, helps founders manage risk and maintain control. Strategic capital planning is essential for long-term sustainability and investor confidence.

Emerging Trends Shaping Investor Interest

Several trends are shaping the smart mobility market, influencing both funding strategies and investor priorities:

Increased Debt Financing in Europe

Mature mobility ventures in Europe are increasingly turning to debt financing, which tripled between 2023 and 2024, reaching $9 billion. This shift reflects a growing preference for non-dilutive funding options, particularly for companies with established revenue streams.Focus on EV-Related Technologies

Investments in EV infrastructure and battery technology are dominating the market. Startups focusing on these areas are well-positioned to attract investor interest, given the global push for sustainable transportation solutions. For deeper insights into this vertical, examining EV charging startup investor interest can help you understand the continued support for this rapidly evolving sector.Strategic Pitching for EV Infrastructure

Crafting a compelling pitch tailored to EV-specific opportunities is crucial. A review of investor communication strategies includes discussions on how to pitch investors EV charging, reflecting nuanced approaches within the EV infrastructure landscape.

A Practical Example

One example is Moove, a Nigeria-founded mobility fintech that finances vehicles for ride-hailing and delivery drivers using a revenue-based, drive-to-own model. Launched in 2020, Moove first raised venture capital and blended it with debt to fund its vehicle pool, rather than relying purely on equity. In 2022, the company closed a $105 million Series A2 consisting of both equity and debt to scale its model into new regions.

In 2024, it raised a $100 million Series B at a $750 million valuation, with Uber and Abu Dhabi’s Mubadala among the key investors. The round brought Moove’s total equity funding to around $350 million and debt financing to about $210 million, earmarked to expand into 16 markets and significantly increase its EV fleet.

Key takeaways from this:

- You don’t have to choose between only VC or only loans, hybrid capital can work especially well for mobility.

- Strategic investors (platforms like Uber, OEMs, sovereign funds) often come later, once the model is proven.

- Tying each round to clear milestones (new markets, EV rollout, profitability) makes the story much more investable.

Conclusion

Fundraising for mobility startups requires a strategic blend of storytelling, outreach, and campaign execution. By capitalizing on industry trends and tailoring outreach efforts, startups can unlock new opportunities and drive meaningful engagement. A well-rounded approach not only simplifies fundraising but also positions your venture for sustainable growth.

If you are serious about raising capital, our startup fundraising consulting service can work with you to sharpen your story, structure your round and give investors a clear reason to say yes.

Key Takeaways

- Integrated platform features streamline the complex fundraising process for mobility startups.

- A compelling company profile, a curated investor network, and automated campaign management are key to successful funding.

- Non‐dilutive financing options and strategic partnerships enhance market credibility.

- Data‐driven insights, industry case studies, and real-world statistics highlight effective strategies to overcome fundraising challenges.

- Staying ahead with emerging trends such as EV technology focus and increased debt financing is essential for scalable growth.

Frequently asked Questions

What government incentives are available for mobility startups in 2025?

Mobility startups can access grants, loan guarantees, and tax breaks from governments in the EU, North America, India, and China. These incentives often support pilot projects, R&D, and infrastructure expansion.