Table of Contents

Only a few founders realize how much the fine print in a term sheet can shape their company’s future. Insurance covenants, those clauses that dictate what insurance you must carry, are increasingly common, especially as investors seek to de-risk their portfolios. For a founder like you, understanding these clauses is not optional. They can impact your valuation, your control, and even your ability to attract future investors.

Insurance covenants have become a crucial part of modern venture capital term sheets for startups.

This article unpacks the insurance covenants investors demand in term sheets, why they matter, and how you can use them to your advantage.

Let’s get started!

Why Insurance Covenants Are Now Standard in VC Term Sheets

VC funding trends reinforce investor caution. In 2023, venture capital financings dropped 22%, falling from 17,625 to 13,701 deals. This volume change explains stronger covenant adoption in term sheets. Fewer deals means each surviving check faces tighter diligence scrutiny. Limited partners now expect funds to document downside protection in every investment memo. Covenants give the fund a defensible answer when LPs ask how portfolio risk is controlled. Treat the clause as a board-reporting line item, not legal boilerplate.

The venture capital term sheet is the blueprint for your investment deal. While it is non-binding, it sets the tone for all subsequent legal agreements and negotiations. In recent years, insurance covenants have become a fixture in these documents.

Investors use insurance covenants to guard against operational, legal, and management risks. For you, these clauses can mean the difference between a smooth funding process and a deal that falls apart at the last minute. Founders who anticipate these requirements and address them early are more likely to secure favorable terms and close rounds faster. From a diligence view, missing coverage surfaces as an open item in the data room. Open items delay closing and weaken your negotiating position. At exit, an acquirer's counsel will re-test the same policies during confirmatory diligence. Clean coverage today reduces escrow holdbacks and indemnity caps later.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

How Does Insurance Fit in a VC Term Sheet?

A VC term sheet covers several key areas: economics, control, and investor protections. Insurance covenants typically fall under investor protection clauses, alongside anti-dilution, liquidation preference, and information rights.

Investor protection clauses often go beyond insurance. Many term sheets also require a minimum cash reserve of $1 million, which keeps the company financially stable. For founders, the minimum cash covenant signals that investors price risk management across the whole deal.

Economics

- Pre-money valuation and price per share

- Amount of investment and capitalization

- Dividends and liquidation preference

Control

- Board representation and voting rights

- Reserved matters requiring investor approval

Investor Protections

- Anti-dilution provisions

- Redemption or repurchase rights

- Insurance covenants

Regulatory shifts drive term sheet changes. On October 2, 2025, the NVCA updated model documents to reflect recent legal and market developments. This revision signals ongoing evolution in investor protection standards and covenant language.

What Are Insurance Covenants?

Insurance covenants are clauses requiring your startup to maintain set types and levels of coverage. Common forms include Directors and Officers (D&O) insurance, key person insurance, and cyber liability. From a diligence view, they give investors documented proof that downside risk is controlled before capital goes in.

Why Investors Insist on Insurance Covenants

Investors want to minimize downside risk. Insurance covenants ensure a financial safety net if a founder lawsuit or data breach hits. That safety net matters most in fintech and healthtech, where regulatory and operational exposure runs high.

Typical Insurance Requirements

- D&O Insurance: Protects directors and officers from personal liability in lawsuits related to their management decisions.

- Key Person Insurance: Covers the company if a founder or critical executive dies or becomes incapacitated.

- Cyber Liability Insurance: Shields against losses from data breaches or cyberattacks.

- General Liability and Product Liability Insurance: Covers claims from third parties for bodily injury, property damage, or product defects.

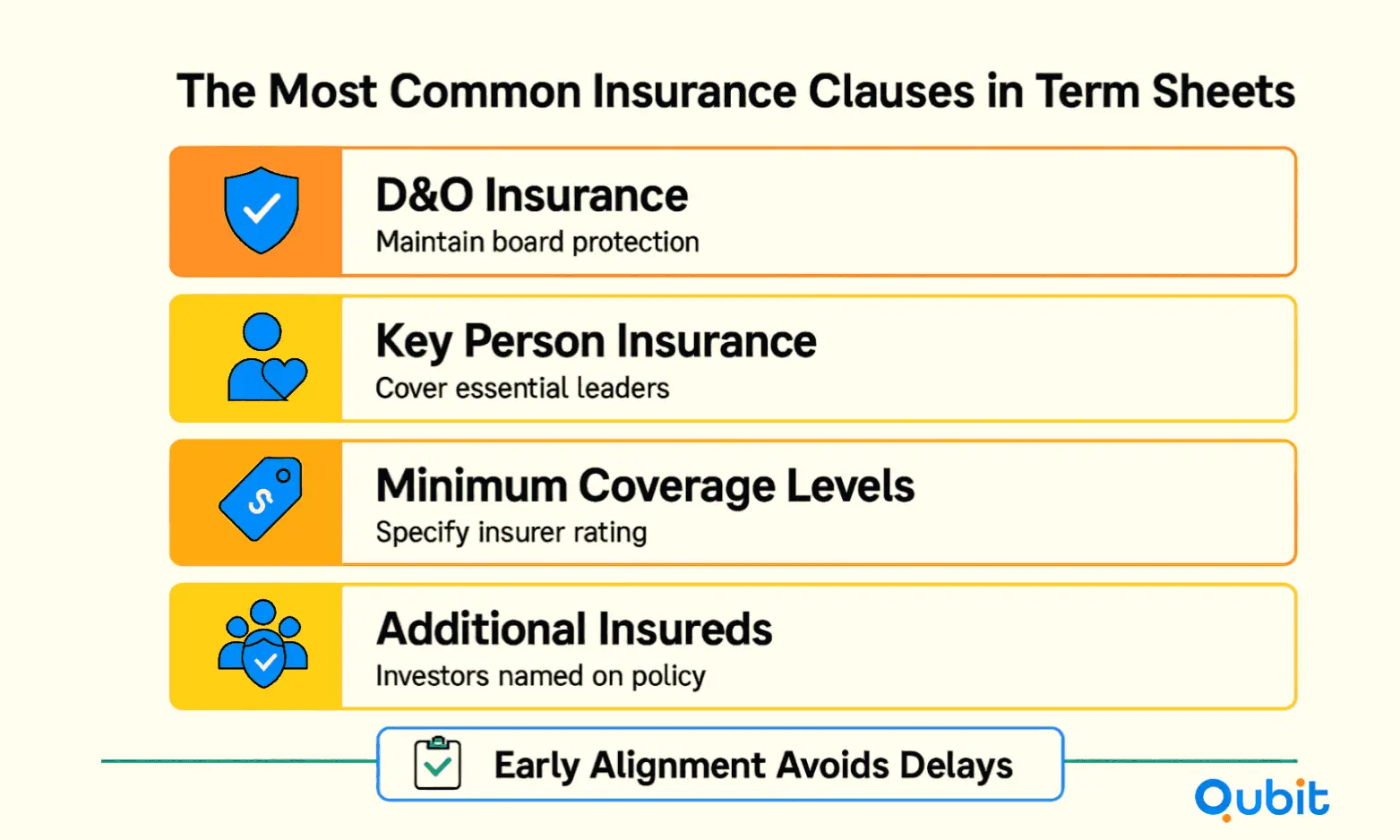

What Insurance Clauses Do Term Sheets Include?

The insurance covenants are frequently included in VC term sheets to protect investors and companies. Let’s break down the key related clauses you’ll encounter as a founder:

1. D&O Insurance Clause

This clause requires you to maintain Directors and Officers insurance at all times. The term sheet will specify the minimum coverage amount and may require you to provide proof of coverage annually. D&O insurance is non-negotiable for most institutional investors, as it directly protects their board representatives. The proof-of-coverage requirement is really an annual diligence checkpoint. Your board can fail it without a cap table change, simply by letting a policy lapse. Track renewal dates in the same calendar as audit and board-pack deadlines. A lapsed D&O policy is the fastest way to scare off a future acquirer.

2. Key Person Insurance Clause

Investors may require you to take out life insurance on founders or essential executives, with the company named as the beneficiary. This protects the company’s continuity if a key leader is lost unexpectedly.

3. Minimum Coverage Levels

Other coverage covenants reflect similar rigor. In venture debt, a typical amortization schedule spans 36 to 48 months, sitting alongside minimum insurance and cash coverage. Term sheets typically specify the insurance types, minimum coverage limits, and the insurer’s financial rating.

4. Ongoing Compliance and Reporting

You’ll be required to provide annual certificates of insurance and notify investors of any material changes or claims. Failure to comply can trigger penalties or even give investors the right to accelerate their investment or demand a buyback. An acceleration or buyback right is a board-level event, not an admin slip. Log every certificate and material-change notice in your compliance register. At the next financing or exit, counsel will request that register first. A clean trail turns a covenant from a liability into evidence of operational maturity.

5. Additional Insured and Waiver of Subrogation

Some term sheets require investors to be named as “additional insureds” on your policies. This gives them direct rights under the policy in case of a claim. A waiver of subrogation (a clause preventing an insurer from recovering costs from investors) prevents the insurer from seeking reimbursement from investors if a claim is paid out.

Negotiating Flexibility in Insurance Covenants

Building on these standard clauses, founders should negotiate flexibility in insurance covenants to support operational needs. Strategies include requesting phased implementation for new coverage, setting materiality thresholds for reporting minor incidents, and including cure periods to address compliance gaps before penalties apply. These approaches help balance investor protection with startup agility, reducing the risk of unintended breaches and costly disruptions.

Why Legal Counsel Is Essential for Insurance Covenants

After outlining negotiation strategies, founders should engage legal counsel to review insurance covenants before signing. Experienced attorneys can identify unfavorable terms, recommend customizations, and ensure compliance with industry standards. This proactive step protects founder interests and helps avoid costly legal disputes or operational setbacks.

If metrics look fine but risk flags linger, see how insurer audits shape investor decisions and fix gaps before the call.

How Insurance Covenants Affect Founders and Startups

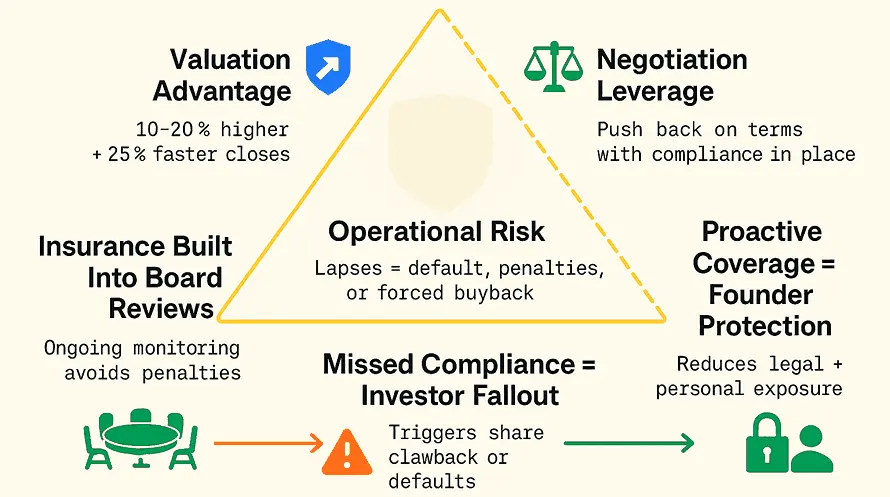

Insurance covenants are not just legal formalities. They have real consequences for your business and your personal risk exposure. For founders, insurance covenants can influence valuation, negotiation leverage, and investor confidence.

1. Impact on Valuation

Startups with complete insurance coverage read as lower risk to an investment committee. Recent data shows companies that proactively meet covenant requirements close rounds 25% faster. They also clear at 10-20% higher valuations than founders who scramble to comply late.

2. Impact on Negotiation

If you come to the table with insurance already in place, you gain leverage in negotiations. You can push back on excessive requirements or negotiate for higher valuation and more favorable terms. Founders who wait until the last minute often find themselves accepting stricter covenants and lower valuations.

3. Impact on Operations

Maintaining the right insurance is an ongoing obligation. Lapses in coverage can trigger penalties, force a buyback of investor shares, or even constitute a default under your investment agreements. This is why it’s critical to build insurance reviews into your regular board meetings and compliance processes.

What Do Investors Look for in Insurance Covenants?

Insurance covenants sit at the center of the due diligence process. California’s Assembly Bill 1415, signed October 11, 2025, now requires pre-transaction clearance and detailed data reporting from private entities. Each new statute adds another compliance line your diligence file must answer.

Before signing a term sheet, investors will want to see proof of existing policies, claims history, and risk management protocols. Treat that request as a dry run for exit diligence. Assemble a single binder with every policy, endorsement, and claims summary. Acquirers and their insurers will demand the same binder, often under tighter deadlines. Building it once now saves weeks during a future transaction.

What You’Ll Need to Provide

- Copies of all current insurance policies

- Claims history for the past three years

- Risk management and incident response plans

- Evidence of compliance with policy requirements

To understand how insurance fits into investor conversations and legal documents, see insurance in due diligence and term negotiation for clear context. It breaks down coverage expectations, risk allocation between founders and investors, and how these insurance clauses are structured in final transaction documents.

Red Flags That Delay or Kill Deals

- Lapsed or insufficient coverage

- Unreported claims or ongoing litigation

- Policies with excessive exclusions or low coverage limits

How Can Founders Use Covenants as a Strategic Advantage?

Founders who treat insurance covenants as a strategic priority, not just a checkbox, stand out to investors.

- Assess insurance needs before fundraising

- Document policies and claims

- Review covenants quarterly

- Negotiate coverage limits proactively

1. Start Early

Begin reviewing your insurance needs before you start fundraising. Work with a broker who understands your industry and can recommend the right policies and coverage levels.

2. Customize Your Coverage

Off-the-shelf policies rarely fit high-growth startups. Tailor your coverage to your business model, industry risks, and investor expectations. For guidance, see insurtech fundraising strategies.

3. Build Insurance Reviews into Board Meetings

Make insurance a standing agenda item at your board meetings. Regular reviews ensure you stay ahead of covenant requirements and can address issues before they become problems.

4. Document Everything

Keep meticulous records of your policies, claims, and compliance efforts. This will make due diligence smoother and give you leverage in negotiations.

5. Negotiate Smartly

Push back on insurance requirements that don’t fit your business. If an investor insists on unusually high coverage, ask for data to justify it or propose a phased approach as you scale.

Conclusion

Insurance covenants are now a fixture in the modern VC term sheet. Prepare early and they become evidence of operational maturity instead of a diligence liability. The strongest founders use them to protect their boards and negotiate from a position of confidence.

Make insurance a core part of your fundraising strategy, and you’ll be better positioned to close deals quickly, retain control, and scale with confidence. You’ll stand out in a crowded market our startup capital raising services. Schedule a call with Qubit Capital to review your term sheet insurance covenants.

Key Takeaways

- Insurance covenants are now standard in VC term sheets and can shape your valuation and control.

- D&O, key person, and cyber liability insurance are the most common requirements.

- Proactively addressing insurance needs gives founders leverage and speeds up funding.

- Lapses in coverage can trigger penalties or even force a buyback of investor shares.

- Customizing your coverage and documenting compliance are essential for smooth negotiations and due diligence.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Frequently asked Questions

What are the most common insurance covenants in VC term sheets?

The most common covenants require directors and officers (D&O), critical-person, and cyber liability insurance. D&O coverage protects leadership against management claims. Critical-person insurance covers the loss of a vital founder or executive. Cyber liability addresses data breaches and digital risk. Most term sheets list these under investor protection clauses.