Back

Back

Table of Contents

Venture capital due diligence is a high-stakes process, especially for early-stage founders. The scrutiny can feel intense because investors want a clear, defensible view of every risk they’re taking on, not just what’s in your pitch deck. Increasingly, they lean on insurers’ audits to provide an independent assessment of your risk profile, digging into operational resilience, compliance, and hidden liabilities that can quietly derail a deal.

These audits aren’t a formality. In 2024, over 65% of VC-backed startups reported that insurance audit findings directly affected their funding rounds, shaping valuation, covenants, and key terms. For founders, understanding how these audits work is now part of being fundable: it’s not just about “passing” due diligence, but building a business that stands up to serious scrutiny.

This article breaks down what insurers’ audits actually reveal in VC due diligence, why they matter, which areas they target, and how you can prepare.

How Insurers’ Audits Influence Funding Outcomes

As of Q3 2025, VC deal value reached $109.6B across 69 reported deals. This surge heightens the need for detailed due diligence, with insurance audits increasingly vital for protecting investor interests in major funding rounds. The role of Insurers’ audits in venture funding has grown rapidly. Ten years ago, many VCs barely glanced at insurance policies.

Stages of VC Due Diligence

VC due diligence unfolds in clear stages, and insurance audits now sit inside that process—not beside it. Investors typically move from an initial screening (fit, basic risk, headline metrics), into deeper dives on documentation and operations, and finally to an investment committee that weighs all findings, including insurance audit results, before making a decision. Understanding this structure helps founders anticipate when insurance scrutiny will hit and how much influence it will have on the outcome.

For early-stage founders, the message is straightforward: insurance audits aren’t just about ticking a compliance box. They’re a test of maturity, foresight, and operational discipline. A clean audit signals that your company is ready to scale; serious gaps can translate into lower valuations, delayed closings, or even cancelled deals. Later sections in this guide offer practical guidance on aligning limits, endorsements, and notice periods with investor expectations.

The stakes are real. Recent analysis shows acquisition failure rates can climb to 70–90% when diligence is incomplete, underscoring how thorough insurance audits protect both founders and investors from avoidable deal blow-ups.

Transparent Communication During Diligence

This opportunity is amplified when founders maintain transparent, timely communication with investors throughout the audit process. Proactively sharing updates and addressing questions reduces uncertainty and builds trust. Responsive engagement demonstrates professionalism and can positively influence investor perceptions. Effective communication often distinguishes startups that secure favorable terms from those that struggle.

Recent results show real impact for founders. Groyyo currently operates at a ₹600 crore annual run rate with 6% EBITDA margins and targets ₹25 crore profit for FY26. Sophisticated risk mapping and audit readiness enabled profitable growth and strong negotiation position.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

The Investor’s Perspective

From the investor’s side, insurance audits offer a way to quantify risk. They allow VCs to compare startups on a level playing field. For example, if two AI startups have similar products but one has robust cyber insurance and the other does not, the insured startup is likely to command a premium valuation.

This premium potential is realized in practice. Rebel Fund has invested in nearly 200 top Y Combinator startups, building a portfolio valued in the tens of billions. Their process leverages AI-driven audits to consistently identify risk-managed winners.

The Founder’s Perspective

For you as a founder, the audit is both a hurdle and an opportunity. It’s a chance to show that you’ve anticipated risks and built safeguards into your business model. It’s also a moment to negotiate from a position of strength, especially if your audit uncovers fewer issues than your peers.

How Audits Reshape Investment Terms

Audit findings directly alter deal structures. Consider these impacts:

What Insurers’ Audits Examine: A Deep Dive

Regulatory changes have widened the scope of insurers’ audits. New capital requirements now use supervisory targets divided by 1.5 to set minimum startup standards, and auditors use these thresholds to test whether your company meets current expectations for financial resilience.

In practice, insurers expect founders to map every meaningful source of liability, from data breaches and IP issues to product failures and operational outages. A strong risk map isn’t a static spreadsheet; it’s a living document that evolves as your business changes.

If you enter a new market, launch a new product line, or handle new categories of data, your risk profile shifts, and insurers expect that shift to be visible in your risk register and supporting documentation. Startups that update these materials proactively, especially in regulated sectors, are more likely to secure funding on stronger terms.

1. Comprehensive Risk Mapping

Insurers want to see that you understand your own risk landscape. This means mapping out every potential source of liability, from data breaches to product failures. They’ll ask for detailed risk registers, incident logs, and evidence of regular risk reviews.

A strong risk map isn’t just a list. It’s a living document that evolves as your business grows. For example, if you’ve recently expanded into a new market, your risk profile has changed. Insurers expect to see that reflected in your documentation. Startups that proactively update their risk registers, especially in regulated sectors, are more likely to secure funding at favorable terms.

If you’re building in insurtech, you may also find our breakdown of insurance start-up funding challenges and strategies useful.

2. Insurance Policy Adequacy and Customization

It’s not enough to have insurance. Insurers will analyze whether your policies are tailored to your actual risks. Off-the-shelf policies often leave dangerous gaps. For example, a generic cyber policy might not cover AI-driven data breaches or third-party integrations.

Insurers will review your policy limits, exclusions, and endorsements. They’ll compare these to your revenue projections and operational footprint. If your coverage is out of sync with your business model, expect tough questions from both the insurer and your investors.

3. Claims History and Incident Response

Your claims history is a window into your risk management culture. Insurers will scrutinize past claims, even minor ones, for patterns. Frequent small claims can be as damaging as a single large one. They suggest systemic issues that haven’t been addressed.

Incident response protocols are equally important. Insurers want to see evidence of rapid detection, clear escalation paths, and thorough post-mortems. Startups with documented incident response drills resolve issues 35% faster than those without.

5. Contractual Risk and Insurance Covenants

Insurers will review your key contracts for risk allocation. This includes customer agreements, vendor contracts, and partnership deals. They want to see clear language on liability, indemnification, and insurance requirements.

Increasingly, investors are inserting insurance covenants into term sheets. These clauses require you to maintain certain types and levels of insurance throughout the investment period. Failing to comply can trigger penalties or even force a buyback of investor shares.

4. Regulatory Compliance and Governance

Regulatory risk is a top concern for both insurers and investors. Audit teams will examine how well you comply with sector-specific rules, GDPR, HIPAA, PCI DSS, and emerging AI regulations. They’ll ask for compliance audits, certifications, policy documents, and proof of ongoing staff training.

Strong governance is a major plus. Insurers want to see an active board, clear lines of accountability, and regular reviews of compliance policies, especially in fast-changing, highly regulated industries. Startups that bake compliance into their due diligence prep are in a much stronger position to negotiate terms and avoid last-minute surprises.

AML (anti–money laundering) oversight is now a critical part of this picture. Starting October 2025, new AML obligations apply to title insurers, and audit methodologies increasingly require startups to show detailed AML protocols as part of their regulatory compliance review.

6. Third-Party Validation and Certifications

Startups with recognized certifications close funding rounds 20% faster and at 10-15% higher valuations, according to a 2024 InsurTech Funding Analysis. External audits and certifications are powerful credibility boosters. Insurers favor startups with recent SOC 2, ISO 27001, or similar certifications. These third-party validations show that your risk controls have been tested by independent experts.

Audit compliance requirements shift annually. The OSFI guideline rollout started in fiscal 2023 with internal audits, moved to senior management oversight in 2024, and external auditor mandates for 2025. Staying ahead of deadlines can streamline audit preparation.

How Audit Findings Shape VC Investment Terms

Insurers’ audits generate findings that have real consequences for your funding journey. Here’s how they play out in practice:

1. Valuation Adjustments

If your audit reveals coverage gaps (uninsured risk areas) or unresolved liabilities, investors will adjust your valuation downward. On average, startups with significant audit red flags see a 20-30% reduction in pre-money valuation.

Conversely, a clean audit can justify a premium. Investors are willing to pay more for startups with robust risk management, knowing that their downside is limited.

2.Term Sheet Covenants

Audit findings often lead to new covenants in your term sheet. These might include requirements to upgrade your insurance, implement new risk controls, or report incidents within a set timeframe. While these clauses can feel restrictive, they’re often negotiable—especially if you come to the table with a proactive risk management plan.

3. Board and Governance Rights

Investors may seek additional board seats or observer rights if your audit reveals governance weaknesses. On the flip side, startups with strong audit outcomes can negotiate for more autonomy and faster decision-making.

Audit Impact Across VC Diligence Stages

| Diligence Stage | Audit Influence | Funding Outcome |

|---|---|---|

| Initial Screening | Flags major coverage gaps early | May halt process or trigger deeper review |

| Deep Dive Analysis | Highlights operational risks and compliance issues | Adjusts valuation and term sheet structure |

| Committee Review | Final audit results inform investment decision | Determines deal approval and governance terms |

For example, startups with D&O (Directors and Officers) insurance secure 25% better governance terms. Those lacking cyber coverage face valuation penalties.

Actionable Audit Preparation Framework

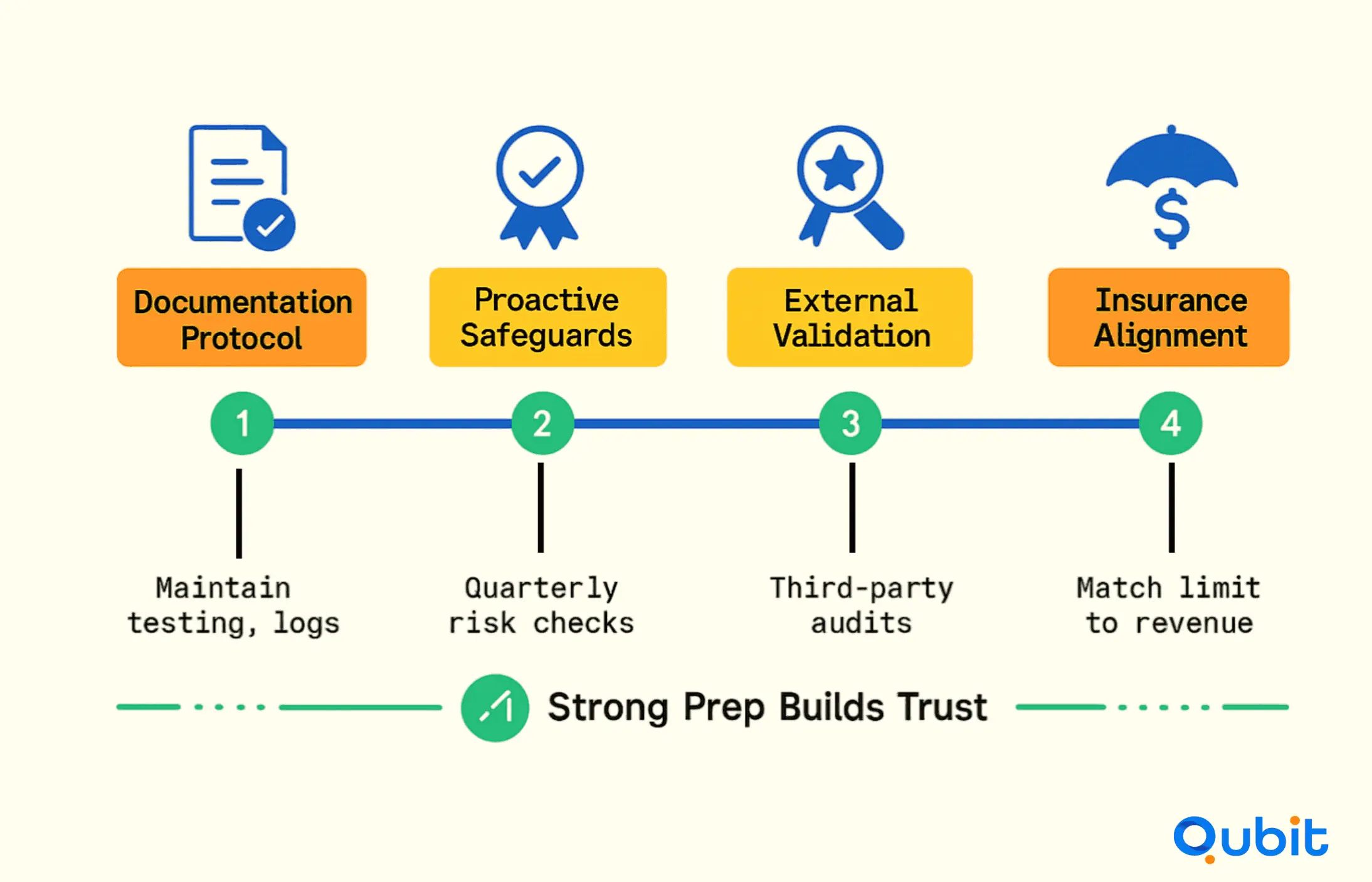

Early-stage founders should implement this 4-phase approach: For example, AcmeAI updated their risk register after a product launch and secured funding efficiently.

Phase 1: Documentation Protocol

Develop living documentation for:

- Data lineage and preprocessing steps

- Model testing results and failure logs

- Deployment safety checks

Phase 2: Proactive Safeguards

- Conduct quarterly risk assessments

- Implement automated monitoring tools

- Train teams on incident response drills

Phase 3: External Validation

- Engage third-party auditors pre-funding

- Obtain relevant certifications

- Benchmark against industry standards

Phase 4: Insurance Alignment

- Match coverage limits to revenue targets

- Prioritize D&O and cyber policies

- Update policies after product changes

If you cannot access an insurance advisor, use industry benchmarks or consult sector-specific online resources.

Founder Pitfalls and Solutions

Avoid these common missteps:

- Underestimating AI Liability

Problem: 68% of early-stage founders overlook AI-specific risks.

Solution: Implement explain ability frameworks and error tracking. - Generic Insurance Templates

Problem: Off-the-shelf policies leave 40% coverage gaps.

Solution: Customize policies with industry-specific endorsements. - Compliance Procrastination

Problem: Regulatory updates cause 6-month funding delays.

Solution: Assign dedicated compliance officers early. - Audit Remediation Delays

Problem: 70% of startups miss critical remediation deadlines.

Solution: Implement 30-day resolution sprints post-audit.

Conclusion

Insurers’ audits are a critical part of the VC due diligence process and can shape a founder’s funding journey. For founders, they represent both a challenge and an opportunity. A well-prepared audit can unlock better valuations, smoother negotiations, and faster funding. The key is to approach audits with the same rigor you bring to product development or go-to-market strategy.

By building robust risk management systems, customizing your insurance, and staying ahead of compliance, you can turn audits into a strategic asset. Remember, investors are looking for startups that can withstand scrutiny and scale with confidence.

You’ll stand out in a crowded market with our insurance startup financing services. Schedule a call with Qubit Capital to review your term sheet insurance covenants.

Key Takeaways

- Insurers’ audits examine AI integrity, risk controls, and compliance.

- Documentation gaps cause 20-30% valuation reductions.

- Third-party validations accelerate funding by 30+ days.

- Tailor insurance to your startup's specific risk profile.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Frequently asked Questions

What role do insurers' audits play in VC due diligence?

Insurers’ audits provide investors with detailed risk assessments, ensuring startups meet compliance standards and helping VCs make more informed funding decisions.