Table of Contents

Launching a new product feels like an exciting leap forward for any startup. It’s proof that your big idea is becoming real. But beneath this excitement lies a reality many founders overlook: the risk of product-related liabilities.

Investors put real money behind your vision. They want assurance that their investment is secure, even if things go sideways. Product liability insurance is one of the smartest ways to protect both your startup and your investor’s capital.

This growing risk shapes a huge global market. In 2024, the global liability insurance market reached $290.5 billion, up from $275.24 billion in 2023. This surge underscores investor and business demand for comprehensive coverage. For startups, understanding this market context helps frame insurance as a long-term asset.

Your examination of product liability insurance expands as you consider insurance startup fundraising strategies, which shed light on the broader challenges faced by insurance start-ups in securing necessary capital.

This blog explores how product liability insurance not only shields businesses but also reassures investors, fostering confidence in product launches.

Let’s jump right in!

What is Product Liability Insurance?

Product liability insurance covers you if your product causes harm, injury, or damage. Think of it as your company’s shield against unexpected legal battles related to product defects or malfunction.

Product liability means a business is legally responsible if its product causes harm or loss. Say your AI-driven insurance platform wrongly rejects claims due to algorithm errors. Users could sue for financial damages. With the right coverage, your insurer steps in, covering your legal defense and any settlements.

In short, product liability insurance prevents one bad lawsuit from bankrupting your startup.

- Identify product risks

- Set coverage limit

- Compare insurers

- Review add-ons

- Get proof for investors

Ready to protect your business? Start by securing a quote for product liability insurance or consult with Qubit for tailored guidance.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

Why Product Liability Insurance Matters for Insurtech Startups

Insurtech companies operate in sensitive territory. Product liability insurance is essential because your products deal directly with people’s finances, personal information, or health.

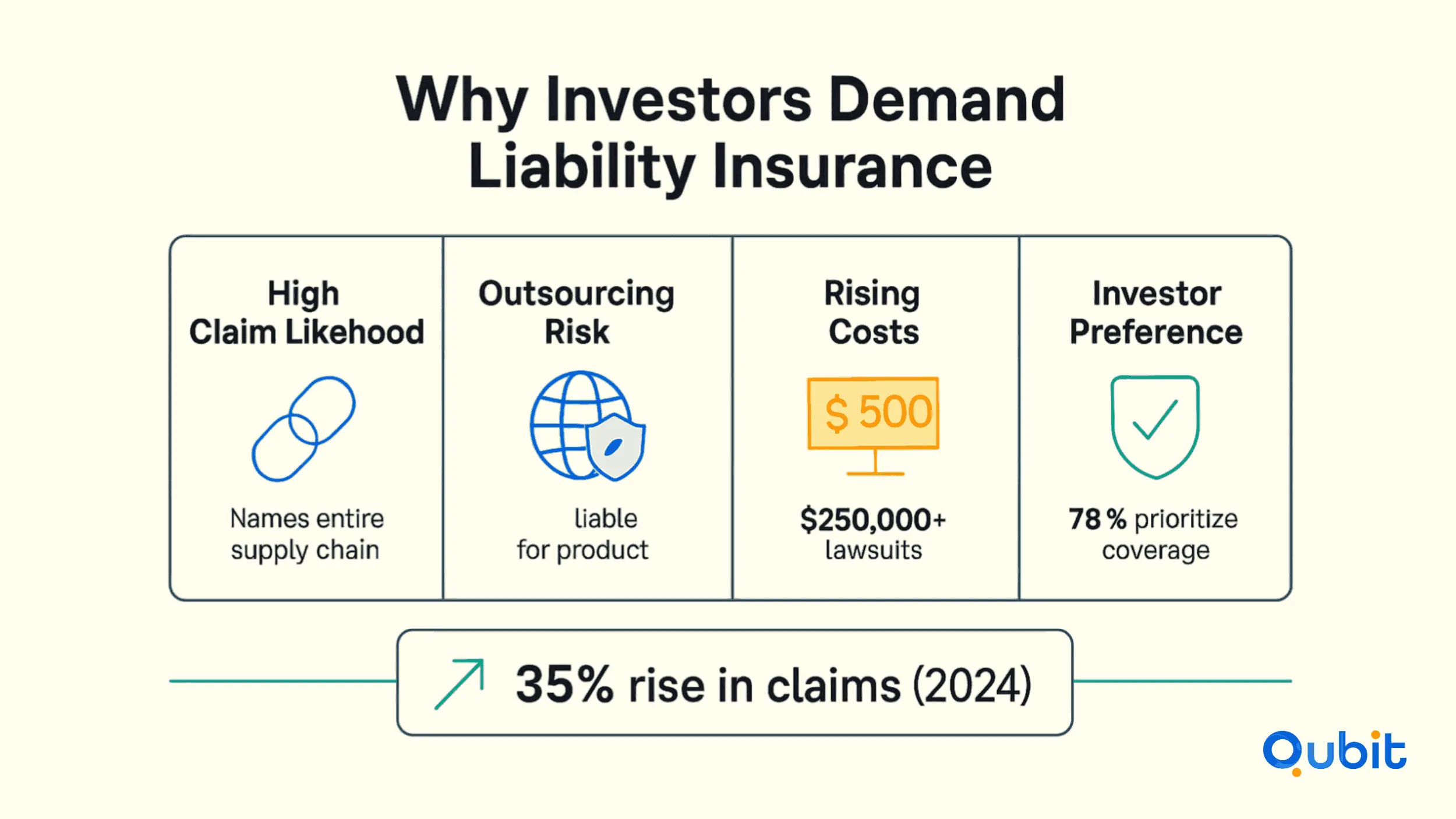

In 2024 alone, claims related to AI bias or inaccurate automated risk assessments rose by over 35%. A single lawsuit related to faulty underwriting can cost over $250,000. Investors know these risks, and they’re increasingly selective. A recent VC survey revealed 78% of investors prioritize startups that actively manage their product risks.

How Much Product Liability Coverage is Enough?

Picking the right coverage level can feel like guesswork. Too little coverage leaves you vulnerable. Too much drains resources better spent on growth.

Start by assessing your product’s real-world risks. For example:

- Could your AI underwriting mistakenly reject critical medical claims?

- What if your customer data handling causes privacy breaches?

- Are there regulatory compliance issues specific to your product?

Most early-stage insurtech startups start with $1M–$2M per claim and $2M–$5M total coverage per year. Adjust this upward as your business grows and risks increase. Remember, higher coverage amounts will increase your product liability insurance cost.

How to Manage Product Liability Insurance Cost Early On

Product liability insurance for small business is essential, even if your startup is just getting off the ground. Insurance premiums can feel heavy for bootstrapped founders. But affordability comes down to choosing coverage wisely.

Here are practical tips:

- Start modular: Choose coverage directly aligned with your product’s core risks. Skip unnecessary add-ons early on.

- Scale progressively: Negotiate with insurers for a lower premium initially, with incremental increases as your product grows.

- Compare wisely: Work with specialized brokers familiar with insurtech. Request a product liability insurance quote to understand your options.

Why Investors Insist on Product Liability Insurance Coverage

Investors consistently require startups, especially those manufacturing, distributing, or selling products, to secure manufacturer product liability insurance. This is usually a condition of funding.

Partnering with a trusted product liability insurance company can reassure investors and streamline the funding process. Their insistence is rooted in both the frequency and severity of product-related claims, the broad legal exposure faced by all parties in the supply chain, and the potentially devastating financial consequences of even a single lawsuit.

Investors require startups, especially those launching physical products, to secure product liability insurance. Their insistence is based on the frequency and severity of claims, broad legal exposure in the supply chain, and devastating financial consequences that can arise from a single lawsuit.

Key Reasons Investors Demand Product Liability Coverage:

- High Likelihood of Claims:

In product liability cases, legal practice is to name every entity in the “chain of distribution”—from manufacturer to retailer, as a defendant. This means that even if your startup outsources manufacturing or is just a distributor, you are still exposed to lawsuits. Legal defense alone can be costly, regardless of actual fault, and settlements or judgments can be financially crippling for a young company. - Outsourcing Doesn’t Eliminate Risk:

Investors know that outsourcing manufacturing, especially to foreign suppliers, does not shield a startup from liability. If your name is on the product, you are often considered the “de facto” manufacturer in legal proceedings. This makes robust product liability coverage essential, regardless of your role in the supply chain. - Severity and Frequency of Claims:

Product liability settlements and judgments can be substantial, often far exceeding the direct costs of injury or property damage. Plaintiffs’ attorneys typically pursue not just actual damages but also lost wages, pain and suffering, and other indirect costs, multiplying potential payouts. The upward trend in settlement sizes over recent years increases the risk for investors, who want assurance that a single claim won’t wipe out their investment. - Financial Protection and Business Continuity:

Product liability insurance protects against the legal, settlement, recall, and compensation costs associated with product defects or failures. Without this coverage, a startup may be forced to deplete its resources, halt operations, or even declare bankruptcy in the face of a major claim. Investors require this protection to ensure the company can survive and continue growing after an incident. - Reputation Management:

Product issues can quickly erode customer trust and damage a startup’s reputation. Product liability policies often include support for public relations and crisis management, helping startups respond transparently and preserve stakeholder confidence, another key concern for investors. - Professionalism and Risk Management:

Requiring product liability insurance signals to investors that founders understand their risk environment and are committed to responsible business practices. This not only protects the company but also enhances its credibility in the eyes of future partners, customers, and acquirers

In particular, many investors insist on complementary coverage like Directors & Officers (D&O) insurance. D&O insurance protects founders and executives personally, not just the company.

Growing investor caution is fueled by industry trends. By 2028, annual litigation funding investment is projected to reach $31 billion. This surge enables more frequent and higher-stakes product liability lawsuits. For founders, anticipating this rising legal funding is central to capital planning.

Advantages of Product Liability Insurance: Mitigating Risks and Bolstering Reputation

Product liability insurance is a critical tool for startups seeking to protect their reputation and financial stability. Industry momentum strengthens these benefits. In 2024, the global insurance industry grew by 8.6%, adding EUR557 billion in premiums. This growth highlights insurer stability and confidence, fortifying the case for robust liability coverage.

Protecting your business from unforeseen challenges is essential, especially when it comes to product-related risks. Product liability insurance offers a robust safety net, shielding companies from financial losses and reputational damage caused by lawsuits or claims.

Long-Term Cost Efficiency

Investing in product liability insurance is a strategic move that saves money in the long run. The proactive mitigation of risks reduces the likelihood of expensive legal battles, ensuring sustainable operations and preserving resources for innovation and expansion.

Common Exclusions in Product Liability Insurance

While product liability insurance offers robust protection, founders must recognize its common exclusions. Coverage typically does not include product recall expenses, employee injuries, or business interruption losses. These exclusions mean startups should consider separate policies or endorsements to address these risks. Understanding these boundaries ensures insurtech founders build a comprehensive risk management strategy that covers all potential liabilities.

Best Practices for Claims Defense

- Maintain detailed records of product development, testing, and quality assurance processes to support claims defense if litigation arises.

- Implement strict quality control measures throughout the product lifecycle to minimize defects and reduce legal exposure.

- Regularly review and update documentation to reflect changes in product features, compliance standards, and risk profiles.

Bundled vs. Standalone Product Liability Coverage

| Feature | Bundled with General Liability | Standalone Policy |

|---|---|---|

| Coverage Scope | Broad, includes multiple risks | Focused, covers product-specific risks |

| Cost Efficiency | Often lower premiums overall | Potentially higher, but customizable |

| Endorsements | Available for recalls and vendors | Requires separate endorsements |

Real-World Scenarios: Learning From Others’ Mistakes

Here are two scenarios demonstrating why coverage matters:

Scenario 1: AI Underwriting Gone Wrong

A promising insurtech firm launched an AI-based underwriting product. A flaw caused hundreds of unjust claim denials, triggering a class-action lawsuit. Without liability coverage, legal costs nearly wiped out investor funds.

Scenario 2: Data Breach Crisis

An early-stage insurtech mishandled sensitive customer health data. A regulatory fine and multiple lawsuits hit simultaneously. Fortunately, their product liability insurance managed costs, saving both investor capital and their market reputation.

Conclusion

Product liability insurance should be a top priority for early-stage insurtech founders. Early-stage insurtech founders juggle countless priorities. Liability insurance might not feel exciting compared to product development or fundraising pitches. Yet, smart insurance coverage directly supports your growth.

Your goal isn't just survival, it's thriving sustainably. By covering your startup against costly risks early, you create a secure foundation for investors, customers, and your team. Product liability insurance is a key part of investor risk protection for startups.

Insurance isn’t just protection, it’s proof you run a disciplined company. Convert that signal into traction with Qubit’s fundraising assistance services for insurance. Get a thesis-led deck, curated investor list, and warm intros, tailored to your stage.

Key Takeaways:

- Product liability insurance shields startups and investor capital from costly legal claims.

- Insurtech startups face heightened risks due to sensitive data handling and algorithm-driven operations.

- Investors strongly prefer startups proactively managing risks through robust liability insurance.

- Coverage limits should realistically match your product's actual risk profile and potential liabilities.

- Complementary insurance like Directors & Officers (D&O) and Key-Person insurance reassures investors.

- Standalone, modular liability policies can offer targeted and cost-effective coverage options for early-stage startups.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Frequently asked Questions

What factors affect product liability insurance cost for startups?

Product liability insurance cost depends on your product type, coverage limits, and claim history. Comparing quotes from multiple providers can help manage costs.