Table of Contents

Raising capital is not just about your pitch deck, traction, or market size. At some point, a serious investor will ask a blunt question: do you have D&O insurance in place?

Directors and Officers (D&O) insurance protects your founders, board members, and key executives if they are personally sued for decisions made while running the company. That could include allegations from investors, employees, regulators, or even customers.

From an investor’s point of view, this is not a nice to have. It is a basic risk control. They are putting money, reputation, and sometimes a board seat on the line. They want to know that one legal claim will not destroy the leadership team or derail the company.

This article explains why investors insist on D&O insurance coverage, what it actually covers, what it does not, and when your startup needs to get it in place.

Understanding Directors & Officers (D&O) Insurance

Directors & Officers (D&O) insurance is a specialized policy that protects organizations and their leadership teams from legal claims and financial losses. By offering protection against legal claims, D&O insurance ensures that decision-makers can focus on their responsibilities without the constant fear of personal liability. Whether it’s a claim of financial mismanagement or a breach of fiduciary duty, this insurance provides an essential layer of security for both individuals and the organization as a whole.

Your understanding of D&O insurance expands when you consider how the broader funding landscape is shaped by insurance startup fundraising strategies, which place risk management at the forefront.

Startups like yours already closed their rounds with us.

Founders across every stage and industry. Here's what it took.

- Raised $7.6M for Swiipr Technologies

- Raised $0.5M for Ap Tack

- Raised €0.5M for Ivent Pro

Why Do Investors Insist on D&O Insurance?

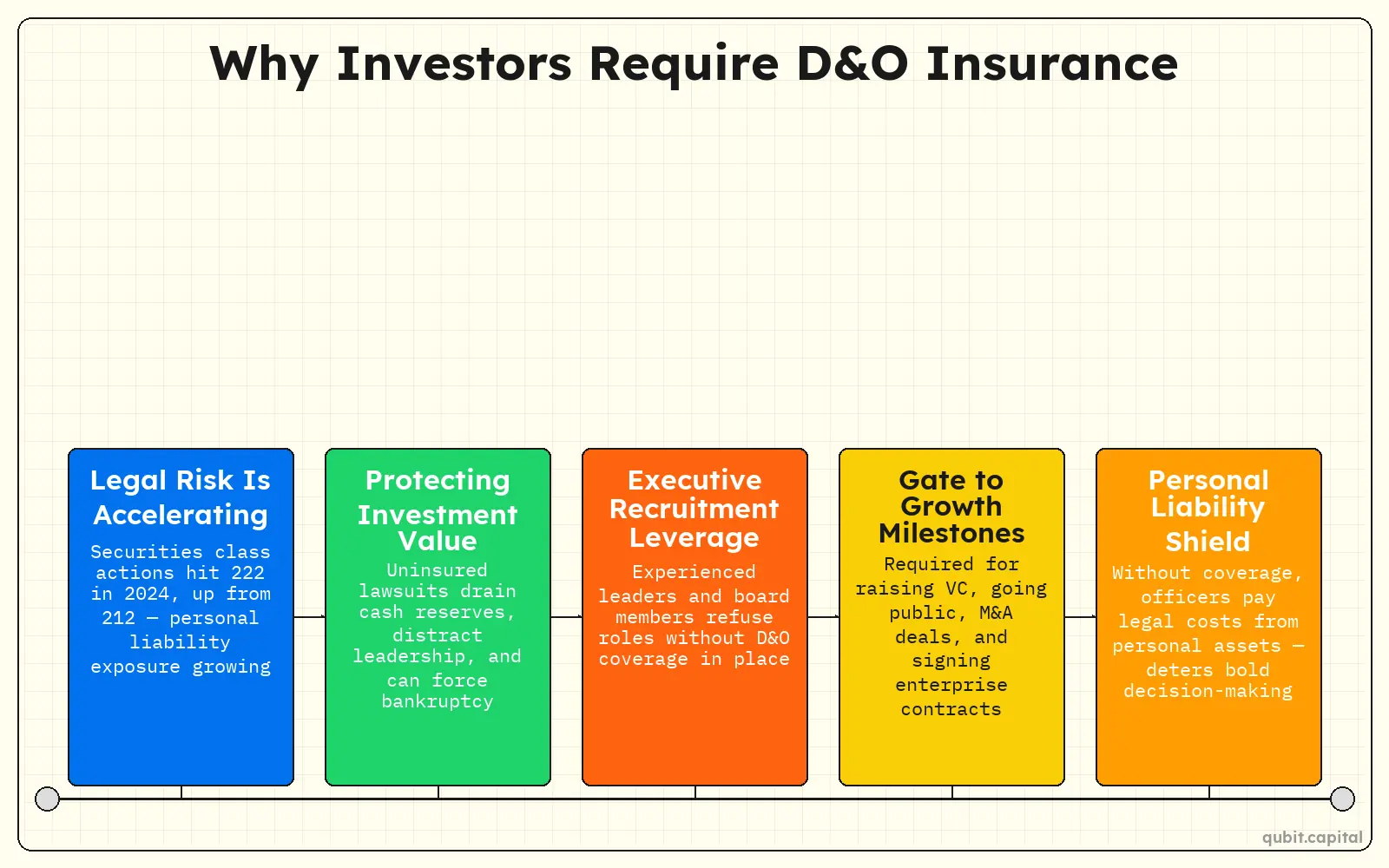

Investors know that talented founders and executives are the backbone of any successful startup. However, these leaders face significant personal liability for decisions made on behalf of the company. If a lawsuit arises, whether from a disgruntled employee, a competitor, a customer, or a regulator, directors and officers can be named personally in the suit.

Legal exposure for corporate officers continues to intensify. In 2024, securities class action filings grew to 222, up from 212 in 2023. This rise highlights increasing risk for company leadership. For startups, it means stronger justification for investor-driven D&O insurance requirements.

Without D&O insurance:

- Directors and officers may be forced to pay legal costs and settlements out of their own pockets.

- The risk of personal financial ruin could deter qualified individuals from joining or staying with your company.

With D&O insurance:

- Leaders can focus on making bold, strategic decisions without fear of personal liability.

- Your startup becomes more attractive to top-tier talent and experienced board members.

1. Rising Legal and Regulatory Risks

The legal environment for startups is more complex than ever. Even the most well-intentioned founders can find themselves facing lawsuits or regulatory investigations for a variety of reasons:

- Alleged mismanagement or breach of fiduciary duty

- Employment practices claims (e.g., wrongful termination, discrimination)

- Shareholder disputes

- Intellectual property challenges

- Cybersecurity incidents

- Regulatory compliance failures

Investors have seen firsthand how quickly legal costs can spiral out of control, and how devastating an uninsured claim can be for a young company. D&O insurance acts as a financial safety net, ensuring that a single lawsuit doesn’t derail your business or destroy the lives of its leaders.

2. Protecting the Value of Their Investment

When investors put money into your startup, they’re betting on your team’s ability to execute and grow the business. A major lawsuit or regulatory action can:

- Drain your company’s cash reserves

- Distract leadership from core business activities

- Damage your reputation in the market

- Force the company into bankruptcy

D&O insurance helps preserve the value of investors’ stakes by protecting the company and its leadership from catastrophic losses. It’s a form of risk management that aligns with investors’ fiduciary duties to their own stakeholders.

3. Attracting and Retaining Top Talent

Experienced executives and board members are unlikely to join a company that doesn’t provide D&O coverage. They know the risks involved in leadership roles and expect to be protected. For startups, offering D&O insurance is a competitive advantage in recruiting and retaining the best people.

4. Facilitating Growth, Partnerships, and Exits

D&O insurance is often a prerequisite for:

- Raising venture capital or private equity

- Going public (IPO)

- Mergers and acquisitions

- Signing major contracts with large customers or partners

Investors, acquirers, and partners want to see that your company has robust risk management practices in place. D&O coverage is a key signal of maturity and professionalism. Start with signals investors trust in insurance startups to see what actually builds credibility.

Covered Expenses: Defense, Settlements, and Judgments Under D&O Insurance

The real shock with D&O claims is not always the headline lawsuit. It is how fast the meter starts running on legal costs.

Today:

- Top defense lawyers can charge up to $1,800 per hour

- Just five years ago, rates were closer to $1,000 per hour

A single complex claim can burn through millions in defense fees before anyone even talks about settling.

Recent trends show settlements fluctuating. In H1 2024, average settlement amount fell to $26 million, down from $35 million in 2023. This drop signals market adjustment but underscores need for adequate coverage as exposures stay volatile.

That drop looks comforting at first, but risk has not gone away. Over time, settlements still average around $34 million, which is enough to seriously damage or wipe out many companies without strong D&O insurance.

Then come judgments, the true worst case scenario. In recent nuclear verdicts, judgments have exceeded $14.5 billion.

D&O insurance is designed to pick up these kinds of costs. It helps cover:

- Defense expenses

- Settlement payments

- Court judgments

So leadership can focus on running the company, not on wondering if one lawsuit might sink it. For additional insights into securing investor capital, explore product liability insurance investor capital.

Core Components and How D&O Insurance Operates

Directors & Officers (D&O) insurance provides comprehensive protection through its core components, addressing multiple liability scenarios.

Side A: Personal Liability Coverage

Side A safeguards directors and officers against personal financial loss when the company cannot indemnify (compensate or protect from loss) them. This coverage is crucial in scenarios like bankruptcy or legal restrictions on corporate indemnification.

Side B: Corporate Reimbursement Provisions

Side B reimburses the company for indemnifying its directors and officers. This ensures the organization can cover legal expenses or settlements without straining its financial resources.

Side C: Entity Coverage

Side C extends protection to the company itself, addressing claims directly against the organization. This broader coverage is particularly valuable during securities lawsuits or regulatory investigations.

Outside Directorship Coverage

This component provides additional security for directors serving on external boards, ensuring their liabilities are covered across multiple roles.

Determining Who Requires D&O Insurance

Organizations of all types can face legal claims against their leadership, making Directors and Officers (D&O) insurance a critical safeguard. Publicly traded companies, for instance, are especially vulnerable due to regulatory scrutiny and shareholder expectations. Private firms, while not subject to the same level of public oversight, still encounter risks tied to employee disputes or contractual disagreements.

Nonprofit organizations and startups are also at risk. Nonprofits often operate under tight budgets, leaving them exposed to financial strain from lawsuits. Startups, on the other hand, face challenges like securing funding and navigating early-stage growth, which can lead to legal complications.

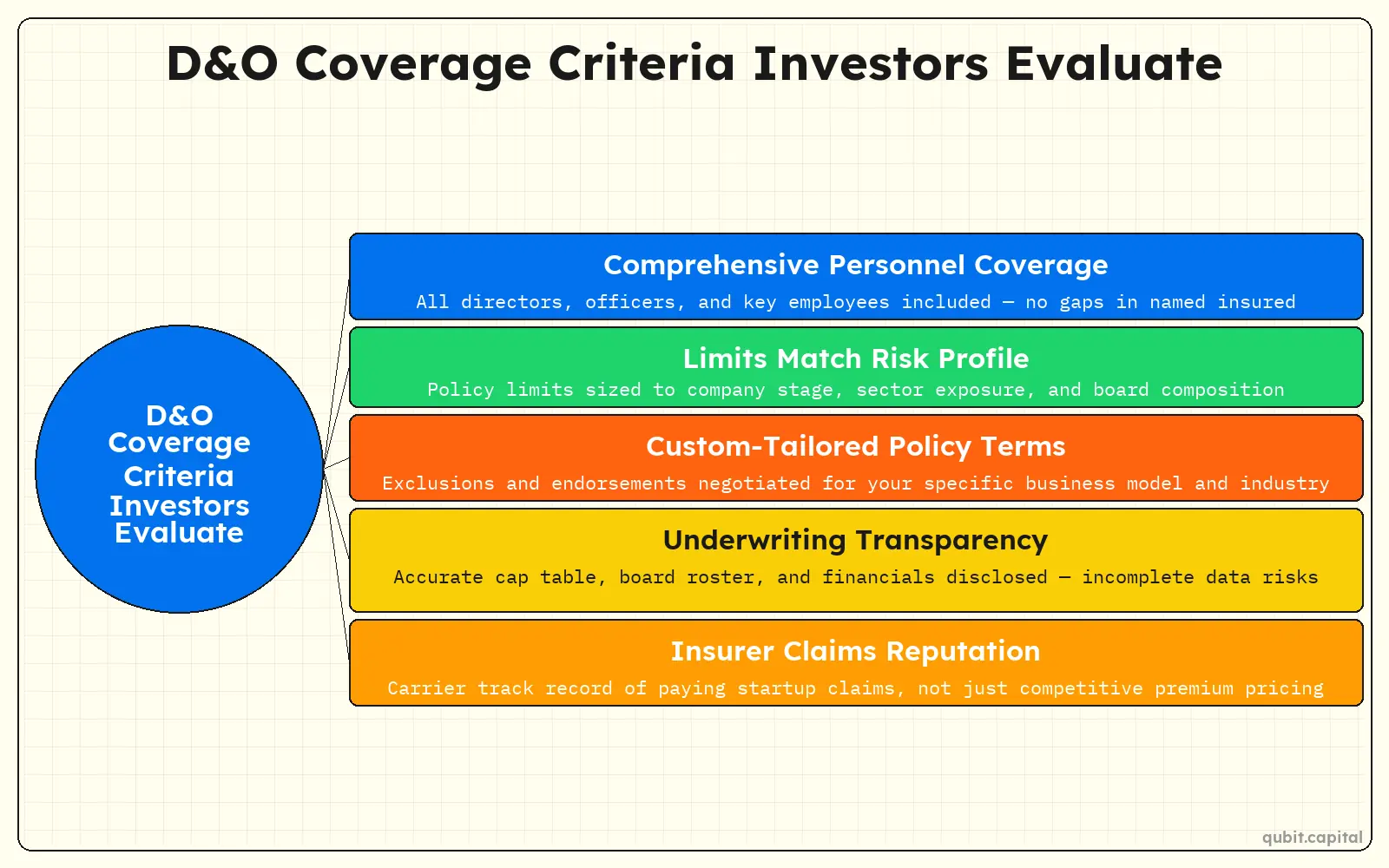

What Investors Look For in D&O Coverage

When investors insist on D&O insurance, they’re not just looking for a generic policy.

The Role of Transparent Disclosures in D&O Underwriting

Building on these expectations, transparent disclosures during the D&O underwriting process are essential for securing optimal coverage. Providing accurate capitalization tables, board member lists, and financial statements enables underwriters to assess risk properly. Incomplete or misleading information can lead to denied claims or unfavorable policy terms. Ensuring full transparency not only builds investor trust but also helps maintain policy continuity as your company evolves.

They want to see that your coverage is:

- Comprehensive: Covers all directors, officers, and key employees.

- Appropriately Sized: Limits are sufficient for the size and risk profile of your company.

- Current: Policy is active and up-to-date, with no lapses in coverage.

- Custom-Tailored: Policy terms are negotiated to fit your business model and industry risks.

- Responsive: The insurer has a good reputation for paying claims and supporting startups.

Checklist for Founders:

- Work with a broker who understands startups and venture-backed companies.

- Share your cap table, business plan, and growth projections with your broker to get the right coverage.

- Review policy limits and exclusions with your board and legal counsel.

- Keep investors informed about your D&O coverage and any changes.

How Much D&O Insurance Do You Need?

There’s no one-size-fits-all answer, but here are some guidelines:

- Seed/Pre-Series A: $1 million to $2 million in coverage is typical.

- Series A/B: $2 million to $5 million, depending on investor requirements and company size.

- Later Stage/Pre-IPO: $5 million to $10 million or more, especially if you have a large board, significant revenue, or operate in a regulated industry.

Factors Affecting Coverage Needs:

- Number of directors and officers

- Amount of capital raised

- Industry sector (e.g., fintech, healthcare, SaaS)

- Geographic footprint (U.S. and international exposure)

- Regulatory environment

- History of prior claims or litigation

Tip:

It’s better to err on the side of more coverage, especially as your company grows and takes on more complex risks.

D&O Insurance: A Must-Have for Private Equity Firms

D&O insurance provides comprehensive protection by mitigating exposure from critical decisions made at the executive level. This ensures that both firm leadership and investors are shielded from the fallout of legal disputes or regulatory challenges. For additional coverage solutions, key person insurance vcs angels can complement D&O measures to reinforce leadership protection.

Frequency of D&O Claims in a Litigious Environment

The prevalence of Directors and Officers (D&O) claims highlights the growing risks faced by corporate leaders. Even when lawsuits don’t result in damages being awarded, defense costs can quickly accumulate, placing a financial strain on organizations. This underscores the importance of robust D&O insurance coverage to mitigate such expenses.

Modern business environments are increasingly litigious, with disputes arising from shareholder actions, regulatory investigations, and employment practices. These frequent claims serve as a reminder that no company is immune to legal challenges. Protecting leadership teams with comprehensive coverage is not just prudent, it’s essential for safeguarding organizational stability.

Litigation impacts are escalating. In H1 2025, Maximum Dollar Loss Index hit $1.851 trillion, a 154% surge over the previous six months. This dramatic rise amplifies urgency for comprehensive D&O coverage.

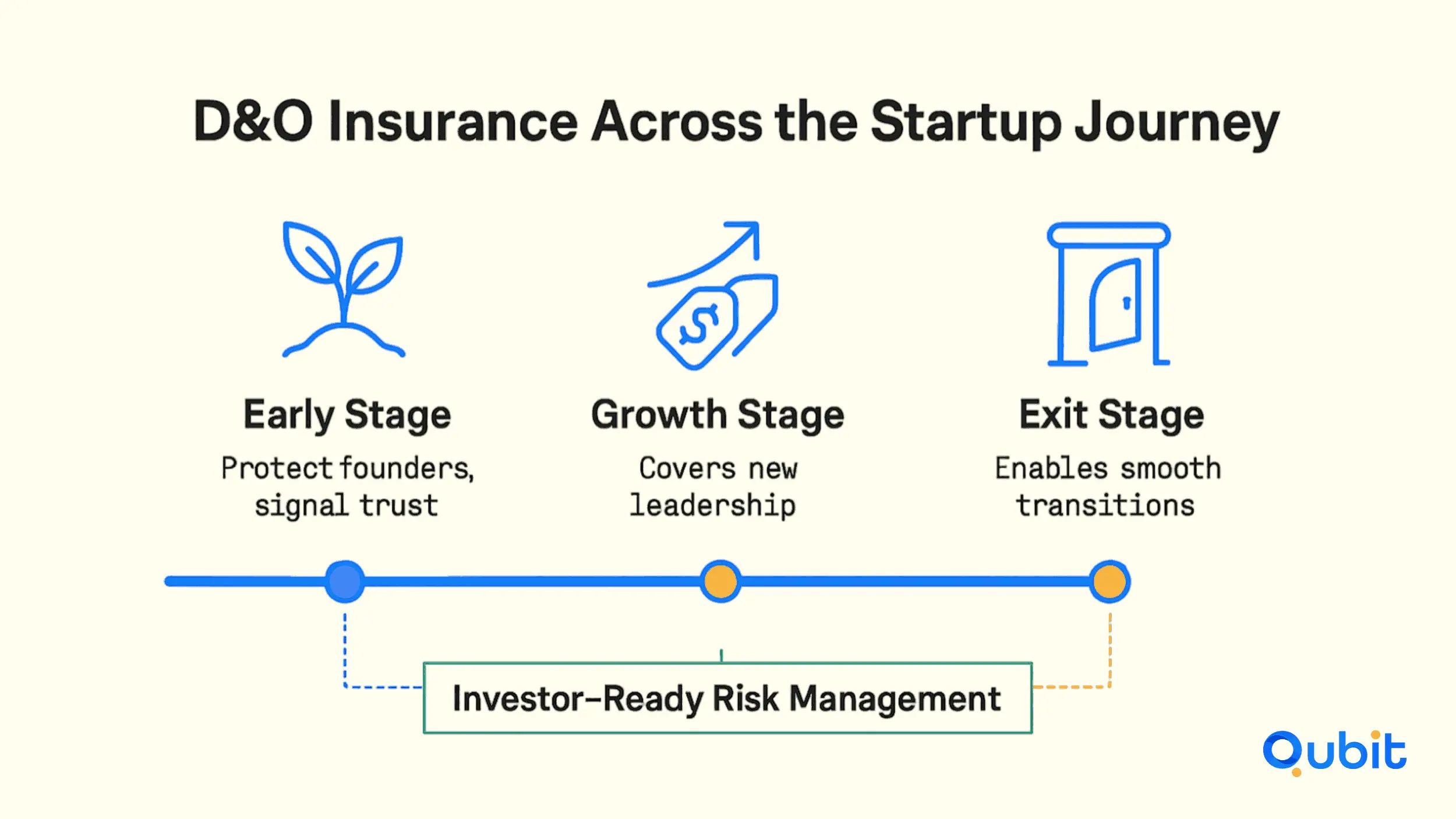

How D&O Insurance Supports Your Startup’s Growth Journey

Early Stage: Building the Foundation

At the seed or pre-Series A stage, D&O insurance helps you:

- Protect founders and early board members from personal liability

- Demonstrate professionalism to investors and partners

- Attract experienced advisors and executives

Growth Stage: Scaling Up

As you raise larger rounds and expand your team, D&O insurance:

- Covers new directors and officers as your board grows

- Provides peace of mind as you enter new markets or launch new products

- Satisfies investor and partner requirements for risk management

Exit Stage: M&A or IPO

When you’re preparing for an exit, D&O insurance:

- Reassures acquirers or public investors that leadership is protected

- Covers claims arising from pre-transaction actions (with “tail” coverage)

- Facilitates a smooth transition and maximizes deal value

Evaluating the Cost Factors of D&O Policies

The cost of Directors and Officers (D&O) insurance is shaped by multiple variables, each reflecting the unique risk profile of an organization. Factors such as company size, annual revenue, and claims history play a pivotal role in determining premium rates. Larger firms with higher revenues often face steeper premiums due to their increased exposure to litigation risks. Similarly, a history of frequent claims can signal higher risk, leading to elevated costs.

Premium ranges also offer valuable insights into potential financial exposure, helping businesses anticipate their insurance expenses. By understanding these determinants, organizations can better assess their coverage needs and budget accordingly. Tailoring policies to align with specific risk profiles ensures both cost efficiency and comprehensive protection.

Common Mistakes Founders Make with D&O Insurance

- Waiting too long to buy coverage:

Don’t wait until you’re closing a funding round or facing a lawsuit. Get D&O insurance early, ideally before your first institutional investment. - Underinsuring:

Don’t skimp on coverage limits to save money. Legal costs can escalate quickly, and underinsurance can leave you exposed. - Ignoring policy exclusions:

Read the fine print. Some policies exclude key risks (e.g., prior acts, certain regulatory claims) that could leave you vulnerable. - Not updating coverage:

As your company grows, your D&O needs will change. Review and update your policy annually, or whenever you raise a new round, add board members, or enter new markets. - Failing to educate the board:

Make sure your directors and officers understand what the policy covers (and doesn’t), and how to access coverage if needed.

D&O Insurance and Other Essential Startup Policies

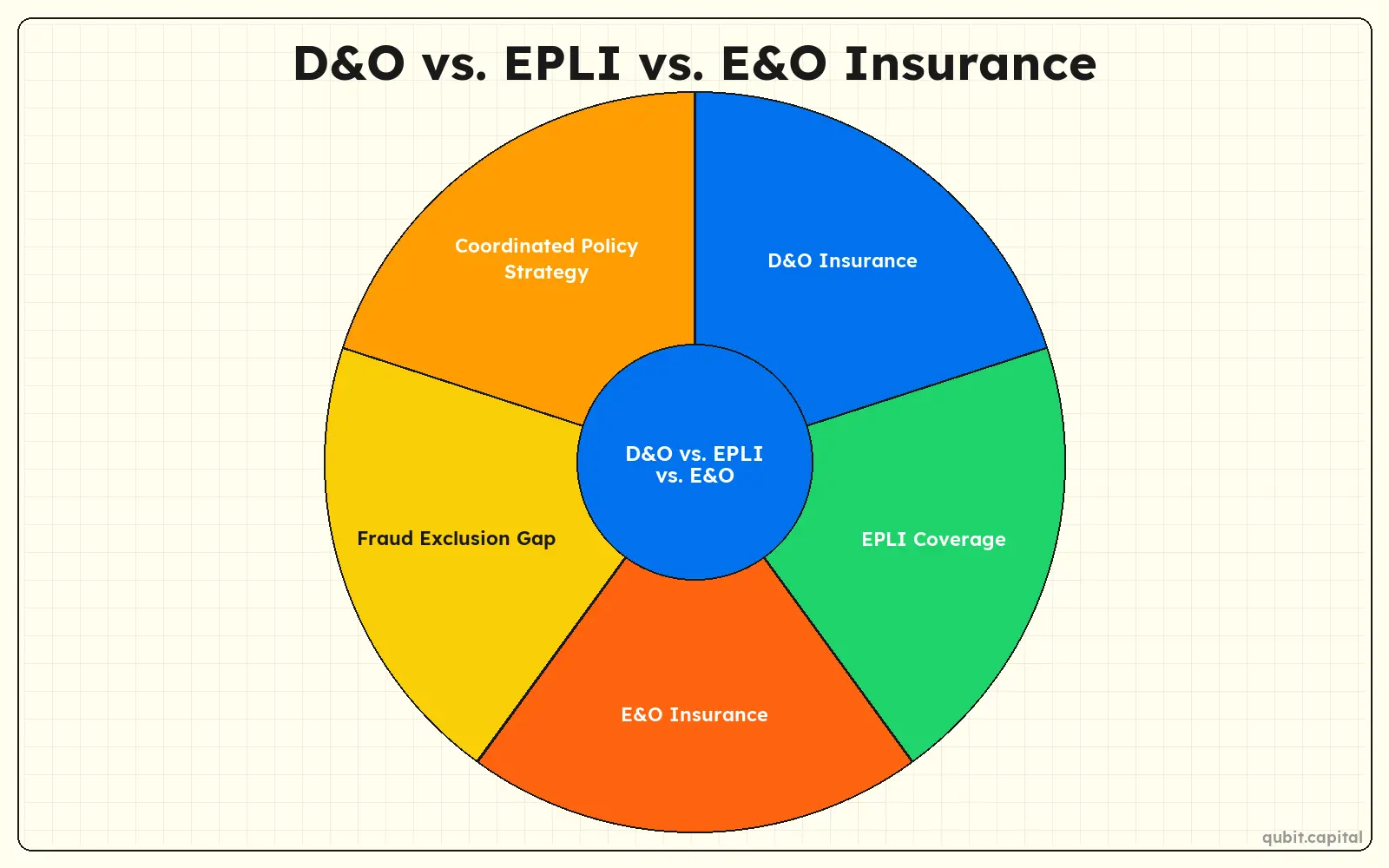

D&O insurance is just one piece of a comprehensive risk management strategy. While it protects your leadership team from personal liability, startups face numerous other risks that require dedicated coverage, from cyber threats and professional errors to employment disputes and general business liabilities. Understanding how these policies work together ensures you’re not left exposed when challenges arise.

Coordinating D&O with Other Key Policies

Integrating D&O insurance with related policies like Employment Practices Liability and Errors & Omissions coverage strengthens your overall risk management. This approach helps close protection gaps that could arise from overlapping exposures or policy exclusions. Coordinated insurance strategies ensure that leadership and the business are covered across a wider range of scenarios, reducing the chance of costly surprises.

D&O vs. EPLI vs. E&O Insurance: Key Differences

| Coverage Focus | D&O Insurance | EPLI | E&O Insurance |

|---|---|---|---|

| Who is protected | Directors and officers | Company and employees | Company and professionals |

| Typical claims | Mismanagement, fiduciary breaches | Discrimination, harassment, wrongful termination | Professional errors, client disputes |

| Common exclusions | Fraud, prior acts | Intentional wrongdoing | Intentional misconduct |

Conclusion

Directors & Officers (D&O) insurance is a strategic necessity for protecting both corporate leaders and investors. Proactive risk management is essential in tailoring insurance policies to meet specific needs. Consulting with experts can help identify potential vulnerabilities and craft a plan that aligns with organizational goals. As businesses evolve, assessing insurance requirements regularly ensures comprehensive protection.

Ready to convert strong governance into momentum? Tap our capital-raising services for insurtech startups for a tighter deck, investor-fit targeting, and a disciplined process that keeps your round moving.

Key Takeaways

- Investors push for D&O because lawsuits can name founders and board members personally, not just the company.

- D&O is a funding enabler because it reduces “key-person risk” and makes board seats easier to accept.

- D&O typically covers defense costs, settlements, and judgments tied to leadership decisions and alleged mismanagement.

- D&O does not cover everything. Fraud, intentional misconduct, and some regulatory or prior-acts issues can be excluded.

- The structure matters: Side A protects individuals, Side B reimburses the company, Side C covers the entity.

- Timing matters: get coverage before institutional rounds, major hires, or adding independent directors.

- Underinsuring is common and expensive. Legal fees can burn through small limits very quickly.

- Clean underwriting matters: accurate disclosures reduce claim denial risk and improve pricing and terms.

- D&O should be reviewed after every round, major board change, or expansion into new markets.

Get your round closed. Not just pitched.

A structured fundraising process matched to your stage and investor fit.

- Fundraising narrative and structure that holds up

- Support from strategy through investor conversations

- Built around your stage, model, and timeline

Frequently asked Questions

What is directors and officers (D&O) insurance?

D&O insurance is a specialized policy that protects company leaders and board members from personal financial losses caused by legal claims tied to their business decisions. It covers defense costs, settlements, and judgments arising from lawsuits related to mismanagement, regulatory violations, or breach of fiduciary duty.