Table of Contents

Startups juggle loans, venture capital, and grants to fund speedy expansion and often maintain momentum.

Yet lenders demand collateral or personal guarantees, driving up interest rates and financial risk.

Insurance-backed guarantees transfer default risk to insurers, unlocking cheaper credit without tying up assets.

To understand the broader financing challenges startups encounter, you gain a broader perspective by exploring how insurance startup fundraising strategies unfold within the overall landscape of funding challenges for insurance start-ups.

This article explores how these guarantees work, why they save you money, and which startups benefit most.

You’ll also discover how to integrate guarantees with other financing tools for smarter capital strategies.

Let’s jump right in!

Why Borrowing Costs Matter for Funded Startups

High interest rates can quickly drain your runway and stall critical growth plans. Every percentage point in saved interest yields more budget for hiring, marketing, and product innovation. Lenders price unsecured startup debt at 8–15% annually when they perceive high default risk.

Collateral requirements force founders to pledge equipment, real estate, or cash reserves as security.

That constraint limits agility, ties up capital, and hinders rapid scaling when opportunities arise. Venture investors often scrutinize debt terms closely, preferring sustainable financing with manageable obligations.

What Are Insurance-Backed Guarantees?

Insurance-backed guarantees are commitments from insurers ensuring payment to lenders if startups default. These guarantees replace or supplement traditional collateral, letting startups access credit at lower rates. You pay a modest premium to insurers instead of locking up physical assets or personal resources.

Guaranteed amounts can cover loan principal, interest payments, or specific performance obligations. Lenders view these guarantees as equivalent to top-tier collateral, often reducing interest margins. Guarantees come in flexible forms, tailored to contract size, industry sector, and risk profile.

The recovery of the market and renewed investor confidence have further contributed to the appeal of insurance-backed guarantees. As lenders feel more secure, borrowing costs for startups are lowered, creating a more accessible pathway to capital. According to the Global InsurTech Funding report, the industry has seen significant investment growth, reflecting its potential to transform traditional financing models.

This funding mechanism not only benefits startups but also aligns with broader economic trends. As businesses stabilize, lenders are increasingly willing to extend credit under favorable terms, fostering innovation and growth across industries.

Core Benefits of Insurance-Backed Guarantees

Insurance-backed guarantees boost your creditworthiness without overburdening your balance sheet. Lower borrowing costs free up cash for core operations and strategic initiatives. By shifting default risk, you preserve key assets and avoid personal guarantees.

These guarantees also signal maturity to investors, showing robust risk management and fiscal discipline. Banks and alternative lenders often respond with deeper credit lines and more favorable covenants. This dual advantage, cost savings and stronger lender relationships, improves your overall funding ecosystem.

If you're ready to optimize your startup's financing strategy, we at Qubit Capital offer our Fundraising Assistance service to help you secure better loan terms.

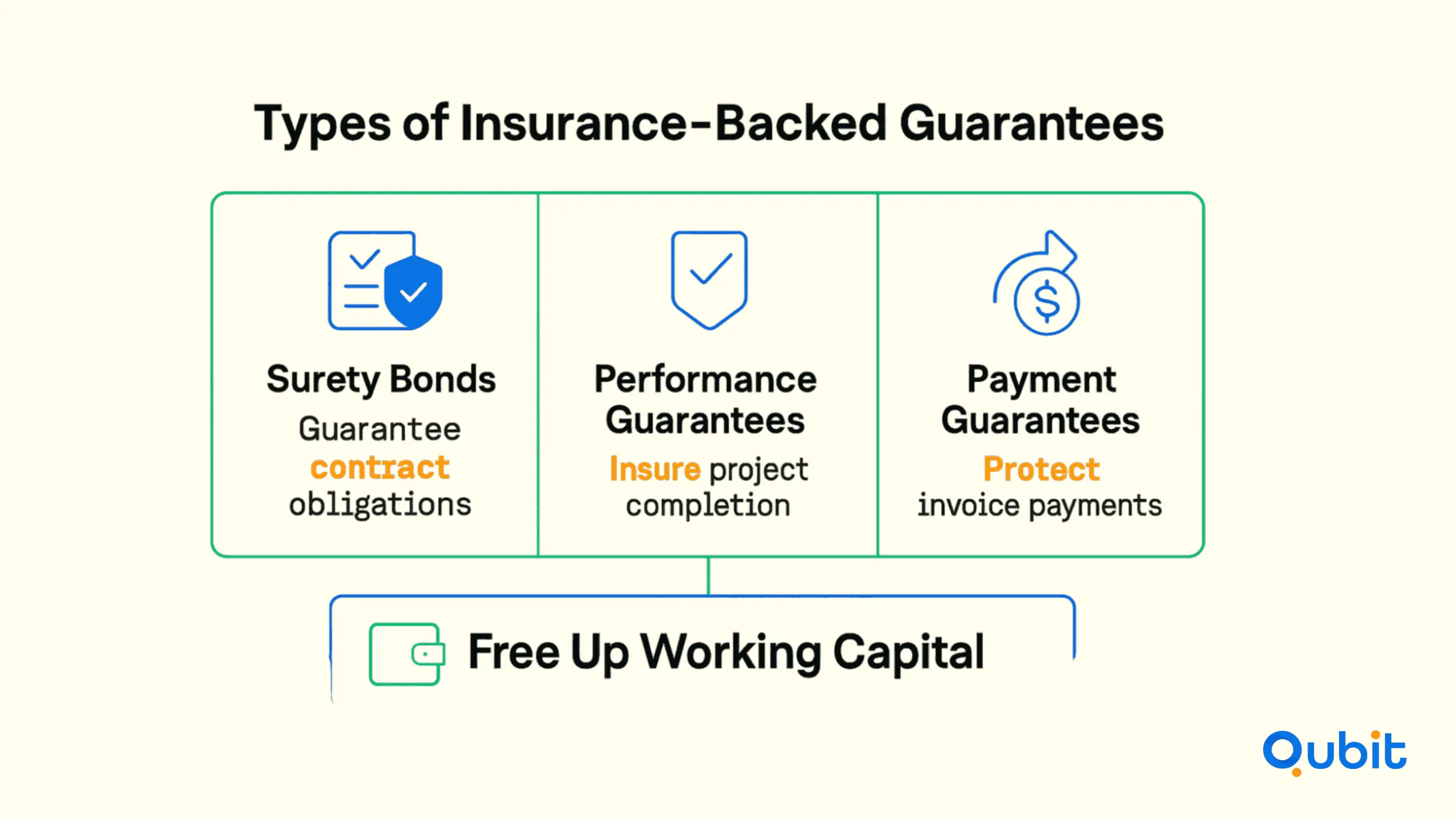

Types of Insurance-Backed Guarantees

Surety Bonds

Surety bonds involve three parties: the startup (principal), the lender (obligee), and the insurer (surety). They guarantee performance, payment, or obligations defined in your credit or contract agreements. If you default, the surety covers the loss up to the bond amount, protecting the obligee.

Startups pay premiums typically ranging from 1–5% of the bond’s total value annually. Insurers evaluate credit history, business track record, and financial projections before offering terms. Strong financials and proven management experience secure better bond rates for growing companies.

Performance Guarantees

Performance guarantees insure project completion, quality standards, or timely delivery of services. Clients and lenders gain confidence knowing insurers cover penalties if service levels slip. These guarantees work well for SaaS deployments, large-scale integrations, and consulting engagements.

Premiums depend on contract complexity, project size, and duration, usually 0.5–2% of contract value annually. Insurers scrutinize vendor capacity, historical performance, and risk mitigation plans during underwriting. Bundling multiple performance guarantees can unlock volume discounts and streamlined policy terms.

Payment Guarantees

Payment guarantees protect against client insolvency or non-payment of invoices and receivables. These guarantees ensure you receive funds owed, even if customers default or face financial distress. Premiums align with buyer credit ratings and total exposure, making costs transparent and risk-based.

Startups with extended payment terms benefit most, as guarantees free up working capital tied in receivables. This liquidity can fund inventory purchases, payroll commitments, or marketing campaigns. International payment guarantees also cover political risks like currency freezes or export restrictions.

How Guarantees Reduce Borrowing Costs

Lenders often reduce interest rates by 1–3 percentage points when guarantees back loans. Insurers with high credit ratings absorb the default risk, giving lenders confidence in repayment. That confidence translates into tighter margins, saving startups substantial interest expenses annually.

For example, a $2M loan at 12% interest drops to 9% with a guarantee, saving $60K yearly. Over a three-year term, a startup could save more than $180K, directly boosting runway. These savings compound as you layer multiple guarantee-backed facilities during successive growth rounds.

Who Should Consider Insurance-Backed Guarantees

Young startups lacking substantial collateral find guarantees especially valuable for unlocking credit lines. Companies with strong revenue growth but limited hard assets can leverage guarantees effectively. High-growth ventures landing large contracts or leases also benefit from performance and surety bonds.

Exporters and companies targeting new markets can use guarantees to cover political and buyer risks. SaaS and service firms with multi-year contracts often secure payment guarantees on recurring revenues. If you plan significant CAPEX investments yet lack equipment to pledge, guarantees fill collateral gaps.

Comparing Guarantees to Other Financing Tools

- Risk Transfer without Asset Sale

Guarantees shift default risk to insurers, unlike factoring, which sells off receivables. - Maintained Ownership

You keep your assets on the balance sheet, rather than handing them over to a factor. - Receivables Protection Options

Trade credit insurance can similarly safeguard invoices and buyer risks. - Complementary Use

Layer guarantees with other financing tools for tailored cash-flow solutions. - Flexible Cost, Control & Access

Each instrument addresses different liquidity needs based on growth stage and appetite.

Explore additional structures in our Insurance-Backed Financing Instruments guide.

Step-by-Step Guide to Obtaining Guarantees

- Assess Your Needs

- Identify your upcoming loan size and any collateral gaps.

- Pinpoint performance or payment obligations to insure.

- Prepare Documentation

- Gather financial statements, revenue forecasts, and key contract details.

- Compile management resumes and operational plans for underwriters.

- Engage a Specialist Broker

- Choose a broker experienced in startup guarantee programs.

- Have them source and compare offers from multiple insurers.

- Negotiate Terms

- Finalize guarantee amount, coverage period, premiums, and deductibles.

- Clarify exclusions, claim triggers, and renewal conditions.

- Secure the Guarantee

- Obtain the formal bond or policy document from your insurer.

- Include it in your lender’s credit application to unlock lower rates.

Case Studies

- A fintech API provider used a $1.5M performance guarantee to secure major banking partnerships. They reduced required deposits by 100% and cut their interest rate by 2.5%, saving over $37K annually. This arrangement accelerated their product roadmap while preserving precious cash reserves.

- An IoT hardware startup placed a payment guarantee on $750K of distributor invoices. That guarantee at a 1.2% premium enabled them to negotiate extended supplier terms and better pricing. They improved gross margins by 3% and accelerated inventory turns, fueling profitable growth.

- A SaaS platform backed its office lease with a $200K surety bond instead of posting a deposit. That move freed up budget for hiring critical engineers, boosting product development velocity. They avoided tying up 10% of their operating budget in real estate deposits.

Measuring Impact on Financial Metrics

Guarantees sit off–balance sheet, preserving asset values without adding reported liabilities. Improved leverage ratios and current ratios enhance your standing with lenders and investors. That stronger balance sheet can unlock lower covenant thresholds and larger credit facilities.

Analysts often apply discounted cash flow models incorporating lower interest expense projections. Reduced financing costs increase free cash flow and drive higher valuations in fundraising rounds. Founders benefit from transparent financial statements that showcase disciplined risk management.

Conclusion

Insurance-backed guarantees deliver powerful cost reductions and collateral flexibility for funded startups.

They shift risk to insurers, freeing founders from pledging valuable assets or personal guarantees.

Lower borrowing rates and stronger lender relationships translate into more runway and growth capital.

By understanding guarantee types, costs, and application steps, you can craft smarter financing plans.

Combine these guarantees with trade credit insurance, receivables financing, and other instruments for balanced capital stacks.

Accelerate your round with our insurance startup financing services, aligning funding strategy to stage, milestones, investor expectations, and sustainable growth. Contact us today to learn more and take the next step toward achieving your growth objectives.

Frequently asked Questions

What are insurance-backed guarantees?

Insurance-backed guarantees are commitments provided by insurers to cover loan defaults. These guarantees reduce the risk for lenders, making it easier for startups to access financing with improved terms.