Back

Back

Table of Contents

Funding a startup often begins with the people closest to you—friends and family. This approach, commonly referred to as FFF (Friends, Family, and Fools), can be a lifeline for entrepreneurs who lack access to traditional funding sources. According to World Business Chicago, nearly 38% of startups rely on FFF as an early-stage financing strategy. While this method can provide essential capital, it also comes with emotional and financial risks that must be carefully weighed.

For those exploring broader funding options, the discussion on types of startup funding offers a comprehensive context, situating friends and family funding alongside other methods. Understanding these dynamics is crucial for making informed decisions about whether FFF is the right path for your venture.

What You Need to Know About Friends and Family Funding

Friends and Family Funding (FFF funding) is often the first financial lifeline for many startups. This informal financing method involves raising capital from personal networks, including close friends, family members, and sometimes acquaintances willing to take a risk.

Why FFF Funding Matters

FFF funding provides entrepreneurs with a straightforward way to secure capital without the complexities of formal investment structures. Unlike traditional funding methods, such as venture capital or private equity, FFF funding is typically based on trust and personal relationships rather than rigid financial metrics. This makes it particularly appealing for startups that lack a proven track record or substantial assets.

An exploration of private equity for startups offers you a perspective on structured investment options that contrasts with the informal nature of raising funds from personal contacts. While private equity involves detailed negotiations and professional oversight, FFF funding allows founders to focus on building their business without immediate pressure from external investors.

Key Considerations for Entrepreneurs

- Risk Awareness: Borrowing from friends and family can blur the lines between personal and professional relationships. Entrepreneurs must ensure transparency and set clear expectations to avoid misunderstandings.

- Documentation: Even informal funding should be backed by basic agreements outlining repayment terms, equity stakes, or other conditions. This safeguards both parties and minimizes future disputes.

- Scalability: While FFF funding is an excellent starting point, it may not be sufficient for long-term growth. Founders should plan for transitioning to more formal funding methods as their business scales.

FFF funding plays a pivotal role in enabling startups to take their first steps. However, balancing trust with professionalism is essential to make the most of this opportunity.

Weighing the Pros and Cons of Friends and Family Funding

Turning to friends and family for funding is a common choice for small businesses, with nearly 38% relying on loved ones for initial financing, according to SCORE. This approach offers a unique blend of accessibility and flexibility, but it also comes with its own set of challenges.

On the positive side, friends and family funding often provides quicker access to capital without the stringent requirements of traditional loans or institutional investments. It can be a lifeline for entrepreneurs who need to act fast to seize opportunities. However, the informal nature of these arrangements can lead to misunderstandings or strained relationships if expectations aren’t clearly defined.

While this funding route can be a stepping stone for growth, it’s essential to weigh the emotional risks alongside the financial benefits. Striking a balance between flexibility and accountability is key to maintaining trust and ensuring long-term success.

Why Friends and Family Funding Might Work for You

Securing early-stage funding can be a daunting task for startups, especially when traditional avenues like venture capital or private equity seem out of reach. Friends and family funding offers a practical alternative, providing access to rare early-stage capital through personal connections. While it may not rival the scale of institutional investments, it can be the perfect solution for entrepreneurs looking to kickstart their ideas.

The Power of Small Investments

A statistic from Silicon Valley Bank reveals that the average friends and family funding amount is approximately $23,000. While this figure may not compete with large venture checks, it’s often enough to jumpstart a prototype or validate a product idea. For many startups, this initial boost can be the difference between stagnation and progress.

Real-World Success Stories

History is filled with examples of businesses that thrived thanks to friends and family funding. Take Apple’s founding loan, for instance. Steve Jobs and Steve Wozniak relied on small personal loans to build the first Apple computers, laying the foundation for one of the most transformative companies in history. Similarly, Spanx’s bootstrapping journey demonstrates how trust capital and a willingness to experiment with new concepts can propel rapid growth. These stories highlight the potential of personal funding to catalyze groundbreaking ventures.

Beyond Financial Support

Friends and family funding isn’t just about money—it’s about relationships. Unlike traditional investors, personal connections often come with mentorship, flexible terms, and lower interest rates. These advantages can help entrepreneurs focus on innovation rather than financial stress. Additionally, the trust and goodwill inherent in these arrangements can foster long-term partnerships that extend beyond the startup phase.

For those exploring alternatives to personal funding, an examination of top private equity firms 2024 highlights key players in the formal investment arena, offering additional insight into structured funding channels.

The Downsides of Friends and Family Funding

Funding a startup through friends and family might seem like a straightforward solution, but it comes with significant challenges that can impact both your business and personal relationships. While this approach is often a lifeline for underrepresented entrepreneurs, as highlighted by the Kauffman Foundation, only 1% of startups successfully secure venture capital. This signals the critical importance of alternative funding avenues like friends and family financing (FFF). However, the informal nature of FFF can create hurdles that are often underestimated.

Risks to Personal Relationships

Borrowing money from close associates introduces emotional complexities. Disagreements over repayment terms or business decisions can strain relationships, sometimes irreparably. Unrealistic expectations from investors who lack business expertise may lead to conflicts, especially if the startup faces setbacks.

Financial Pressures on the Family Unit

FFF funding often places financial strain on the family unit, especially if the business struggles to generate returns. This can lead to guilt or resentment, particularly if the borrowed funds were critical to the lender’s financial stability.

Lack of Legal Protection

Unlike formal funding routes, FFF arrangements often lack structured legal agreements. This absence of protection can result in disputes over equity, repayment terms, or decision-making authority. Entrepreneurs should consult legal experts early to mitigate these risks, especially given the growing enforcement of Regulation D requirements by the SEC. Increased compliance focus has raised legal preparation costs for startups, making it essential to address these issues proactively.

Unrealistic Expectations

Friends and family investors may expect rapid returns or underestimate the challenges of building a business. This pressure can lead to rushed decisions that compromise long-term success. External criticisms from other family members or acquaintances can further complicate matters, affecting both business operations and personal bonds.

For a more structured approach to funding, consider exploring working with private equity pros and cons, which provides a contrast between the informal dynamics of FFF and the professional rigor of private equity partnerships.

Friends and family funding may seem appealing at first glance, but its downsides demand careful consideration. By understanding these challenges, entrepreneurs can make informed decisions that protect both their business and personal relationships.

Securing initial funding for your startup often begins close to home, with friends and family. While this approach can be less formal than institutional funding, it requires careful planning to ensure success and protect relationships.

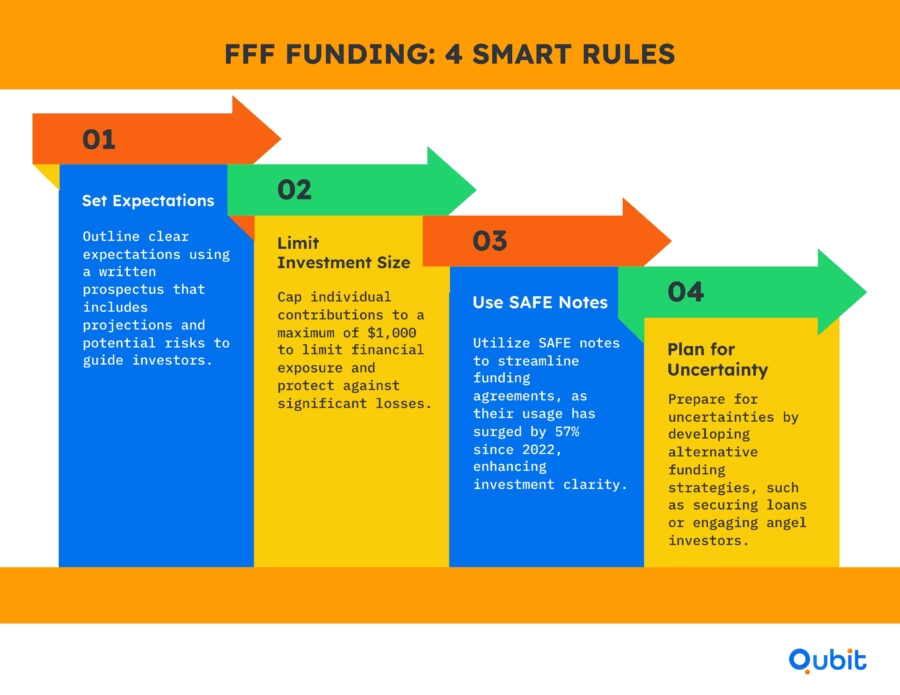

Setting Clear Expectations

Transparency is key when raising funds from personal connections. Begin by drafting a detailed written prospectus that outlines your business plan, financial projections, and potential risks. This document not only standardizes communication but also demonstrates professionalism, helping investors make informed decisions.

Implementing Investment Limits

To safeguard your investors, consider setting a modest cap on contributions. For example, an investment limit of $1,000 ensures that friends and family don’t risk significant savings if your startup doesn’t meet expectations. This approach balances their support with financial prudence.

Offering Structured Agreements

Formalizing agreements is essential to avoid misunderstandings. One effective option is to offer SAFE notes (Simple Agreement for Future Equity), which have seen a 57% increase in usage since 2022. These agreements provide flexibility while maintaining structure, making them ideal for personal investors.

Dealing with Uncertainty Around Your Funding Source

Unpredictability in funding can disrupt even the most well-planned ventures. Entrepreneurs relying on friends and family for financial support often face challenges when personal emergencies or shifting priorities arise. These unforeseen circumstances can lead to inconsistent capital flow, leaving businesses vulnerable during critical growth phases.

To mitigate these risks, it’s essential to explore alternative funding strategies. Diversifying your funding sources—such as seeking angel investors or applying for small business loans—can provide a safety net when traditional support falters. Additionally, maintaining transparent communication with your personal network about your financial needs and timelines can help set realistic expectations.

Entrepreneurs should always prepare for the unexpected. Developing a backup plan ensures your business remains resilient, even when primary funding sources become unreliable.

Conclusion

Raising funds from friends and family offers unique advantages, such as accessibility and trust, but it also comes with challenges like potential strain on relationships and emotional risks. Structuring clear agreements is essential to ensure transparency and prevent misunderstandings. By addressing financial expectations upfront, founders can safeguard both their ventures and personal connections.

Professional guidance can play a pivotal role in managing these dynamics effectively. At Qubit Capital, we understand the importance of balancing relationships while securing capital. If you're ready to explore more structured funding options, we at Qubit Capital can guide you through securing the right investment with our Fundraising Assistance service.

Key Takeaways

Friends and family funding offers quick, flexible capital but comes with significant personal risks.

Real-world examples like Apple’s founding loan and Spanx’s bootstrapping illustrate the potential impact.

Formalized agreements and clear expectation setting are crucial to protect relationships.

Both financial and non-financial contributions from close networks can be extremely valuable.

Frequently asked Questions

What are the disadvantages of friends and family financing?

Borrowing from friends and family can strain relationships if repayment is delayed or expectations aren’t clear. It may also blur personal and professional boundaries, leading to misunderstandings or pressure during business challenges.