- How Venture Debt Helps You Protect Growth and Ownership

- Venture Debt vs. Traditional Financing: Which Is Right for You?

- When Is the Best Time to Use Venture Debt?

- Key Factors to Consider Before Choosing Venture Debt

- Weighing the Pros and Cons of Venture Debt for Your Startup

- Conclusion

- Key Takeaways

How Venture Debt Helps You Protect Growth and Ownership

Securing funding is a critical milestone for startups, but it often comes with the challenge of balancing growth ambitions with ownership retention. Venture debt offers a strategic solution, enabling founders to access capital without diluting equity. This approach is particularly valuable for startups aiming to extend their operational runway while maintaining control over their business trajectory.Preserving Ownership While Scaling

One of the most significant advantages of venture debt is its ability to safeguard founder ownership. Unlike equity financing, which requires giving up a portion of the company, venture debt provides non-dilutive capital. This means founders can secure the funds they need to scale operations without sacrificing their stake in the business. For startups navigating uncertain fundraising environments, this preservation of equity can be a game-changer. Venture debt allows businesses to delay additional equity rounds, ensuring that founders retain control during critical growth phases.Strengthening Credibility with Stakeholders

Beyond funding, venture debt enhances a startup’s credibility with vendors and investors. By demonstrating financial stability and a commitment to responsible capital management, startups can build trust with key stakeholders. This improved creditworthiness can lead to better terms with suppliers and increased confidence from potential investors. An analysis of borrowing is further deepened by the strategies for balancing equity and debt financing, highlighting how a mixed approach can be structured effectively.Extending the Operational Runway

In challenging economic climates, venture debt provides startups with the flexibility to extend their operational runway. This additional time can be crucial for refining products, scaling teams, or entering new markets. By securing capital without immediate equity dilution, startups can focus on achieving milestones that enhance their valuation before pursuing further funding rounds. For founders seeking the best bank for startup business, venture debt offers tailored solutions that align with growth objectives while preserving ownership. This approach ensures that startups can access the resources they need without compromising their long-term vision. Venture debt is more than just a funding mechanism—it’s a strategic tool that empowers startups to grow responsibly while retaining control.What You Need to Know About Venture Debt for Startups

Venture debt is often overlooked, but it can be a powerful tool for high-growth startups. It’s designed for founders who want to raise capital without giving up more equity. In most cases, it’s used alongside an equity round to stretch runway, fund key hires, or bridge to the next milestone. These loans typically come from specialized lenders, private credit funds, or banks that understand startup risk. One of the biggest draws of venture debt is that it's non-dilutive. You keep more control. But that doesn’t mean it’s risk-free. These loans often come with covenants—rules you agree to follow when taking the money.How to Handle Venture Debt Covenants

Covenants might include things like keeping a minimum cash balance or hitting specific revenue targets. If you miss them, lenders can apply penalties or even call the loan. Understanding how to manage covenants means knowing your burn rate, runway, and growth milestones in advance. That’s where the right business banking for startups can help—offering tools to track and forecast. Choosing the best bank for startup business also depends on how they structure debt. Some offer interest-only periods. Others link payments to revenue. These terms matter as much as the loan amount. If you're still weighing whether debt fits your funding mix, it helps to zoom out and compare your options. You’ll find clear contrasts in equity vs debt financing, including what each model expects from you.Venture Debt vs. Traditional Financing: Which Is Right for You?

Venture debt is built for startups. Traditional loans are not. That difference matters. Banks often look for years of revenue, collateral, or profits. Venture lenders look for growth potential and VC backing. That’s why banks that fund startups are usually niche lenders, not big-name institutions.How Interest Rates and Repayment Work in Venture Debt

Interest rates are higher than traditional loans but lower than equity dilution. Repayment can vary. Some loans offer a grace period. Others want immediate principal plus interest.Who Should Use Venture Debt and When?

Startups that just closed an equity round often use debt to extend cash without taking a new valuation hit. It works best when you have VC support, early traction, and a plan to hit the next milestone.Breaking Down Debt Structures and Flexible Covenants

Debt structures differ. Some loans have flat payments. Others link repayment to ARR or revenue. Covenants also vary—some are strict, others adjust based on growth. Using tools like ARR calculators helps model repayment against future income. That’s key for early-stage planning.How to Choose the Right Lender Based on Risk Appetite

Not all lenders think alike. Some specialize in repeat founders. Others focus on underserved sectors. The best match isn’t always the one with the lowest rate—it’s the one that understands your risk profile. Borrowing isn’t just about cash—it’s about control, timelines, and how you plan to grow. Startup loans and debt options gives context to those choices by showing how structure changes with startup maturity.When Is the Best Time to Use Venture Debt?

Timing is everything when it comes to venture debt. For startups aiming to optimize their financial strategy, venture debt is most effective after completing an equity round. This approach allows founders to extend their cash runway without diluting ownership further, making it a strategic choice for early-stage companies with limited revenue streams. By integrating venture debt into their funding mix, startups can bridge the gap between equity rounds and scale operations efficiently.Ideal Scenarios for Venture Debt

Venture debt is particularly suited for startups that have recently raised equity capital. Following an equity round, companies often seek additional funding to maintain momentum without sacrificing equity. Venture debt provides this flexibility, enabling startups to focus on growth initiatives while preserving shareholder value. For early-stage companies, venture debt can be a lifeline. These businesses typically lack substantial revenue streams but possess high growth potential. By securing venture debt, they can invest in product development, marketing, or operational scaling without waiting for the next equity round.Typical Deal Sizes and Emerging Trends

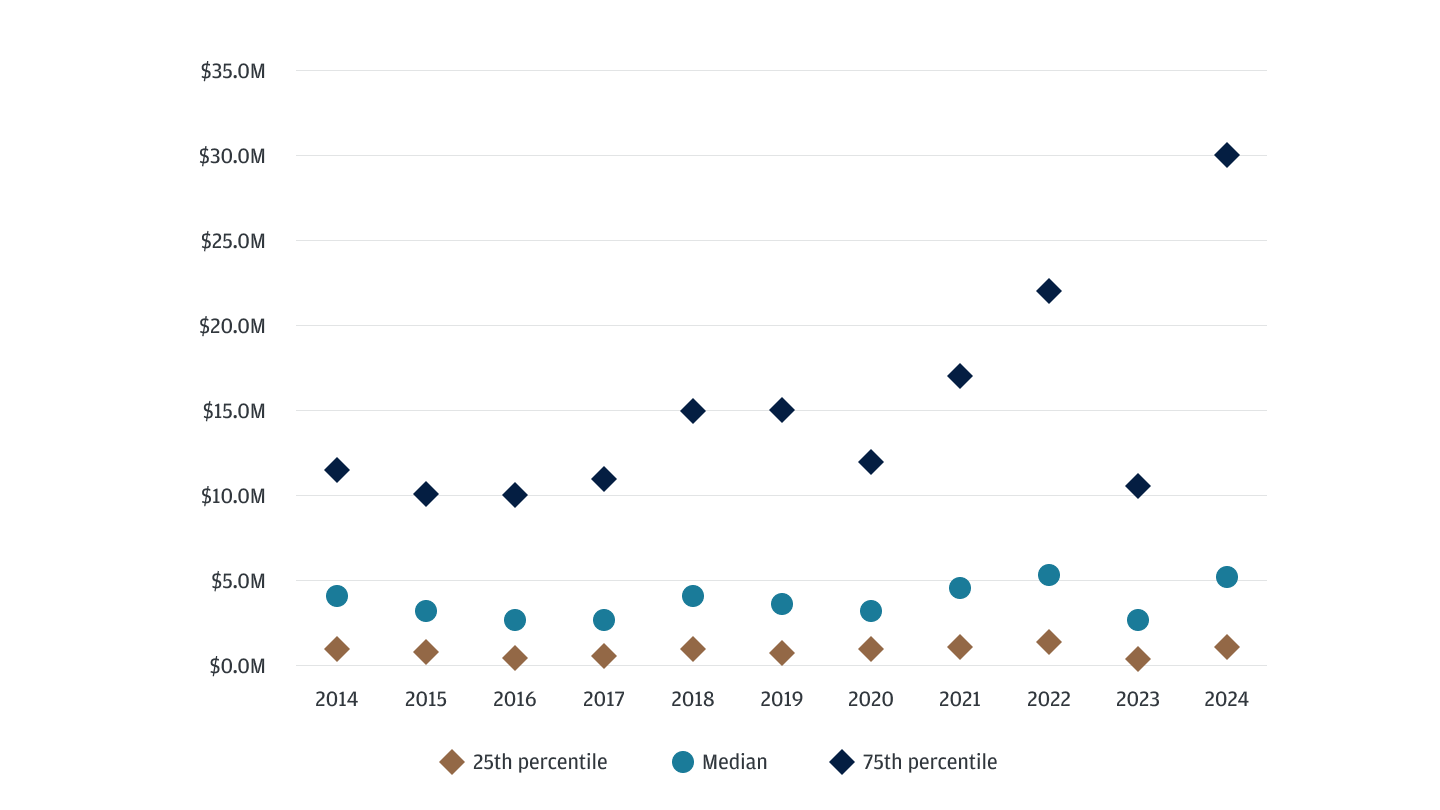

The venture debt market offers a wide range of deal sizes tailored to different growth phases. According to recent data, the median deal size falls between $2.5 million and $5.3 million, making it accessible for startups in Series A or Series B financing stages. Smaller deals, ranging from $500,000 to $1.3 million, cater to companies in earlier stages, while the upper quartile has seen a dramatic surge, with deals reaching $28.9 million as of H1 2024. This trend toward larger deals reflects an increasing appetite for venture debt among scaling startups. As companies mature, they often require more substantial funding to support aggressive expansion plans. This Deal Sizes Infographic illustrates the distribution of venture debt transactions across different quartiles.{kind=link}

Key Considerations for Startups

Before pursuing venture debt, startups should evaluate their financial health and growth trajectory. While venture debt offers numerous advantages, it also comes with repayment obligations that require careful planning. Founders should assess their ability to generate cash flow and meet debt commitments without compromising business operations. Not all debt looks the same. Some founders use short-term credit; others structure long-term loans. The range of types of debt financing for startups reflects just how flexible these instruments can be.Key Factors to Consider Before Choosing Venture Debt

Venture debt can accelerate growth, but it comes with tradeoffs. Here’s a breakdown of what to keep in mind before signing a deal:- Fixed repayments can tighten cash flow—especially if your revenue is still inconsistent.

- Evaluate your burn rate, projected income, and follow-on funding options before committing.

- Debt covenants may restrict hiring, spending, or pivoting without lender approval.

- Some lenders require you to maintain liquidity thresholds or hit revenue targets.

- Choosing a lender familiar with startups often results in more flexible, founder-friendly terms.

- Debt adds liabilities to your balance sheet, which may lower your valuation in future rounds.

- Used well, it helps avoid dilution—Hivebrite grew revenue 40% using a $15M debt deal, without giving up more equity.

- OpenAI secured $500M in venture debt to fund infrastructure, delaying another equity raise.

- Tailored debt structures can support growth without forcing control concessions, if aligned with your strategy.

Weighing the Pros and Cons of Venture Debt for Your Startup

Why Venture Debt Could Be a Smart Choice for Your Startup

Venture debt lets you raise capital without giving up ownership. That’s the headline advantage. It’s non-dilutive, meaning you keep more of your company. For startups with steady growth and strong investor backing, it’s often a smart bridge between equity rounds. Interest payments may also be tax-deductible. That adds value on the margin, especially when you're managing a tight budget. Timely repayments can also build credibility with lenders and improve your ability to access larger facilities in the future.Potential Downsides to Venture Debt You Should Know

Repayment is mandatory, whether your product has found market fit or not. That creates pressure, especially if cash flow slows down. And because most loans include covenants tied to growth milestones, you’ll be held to targets whether the market cooperates or not. Some lenders may charge high interest or include strict penalties for missed benchmarks. That’s why it’s worth looking into the best banks for start up businesses that understand startup volatility and are willing to offer more adaptable terms. Like any funding source, venture debt has trade-offs. It’s not about whether it’s good or bad—it’s about whether it fits your plan right now.Conclusion

Venture debt gives startups a way to grow without giving up more equity. When used well, it extends runway, supports key hires, and adds flexibility between funding rounds. But it’s not just about getting capital. You need to understand what comes with it. That means knowing your repayment schedule, watching your covenants, and being honest about your cash flow. This kind of financing isn’t for every stage or every startup. The right time—and the right lender—makes all the difference. Use what you’ve learned here to ask better questions, evaluate smarter deals, and choose funding that fits where you are now—not just where you want to be. That’s how you build with confidence and stay in control. As you explore funding options, remember that preparation is critical. A clear, strategic fundraising approach can significantly enhance your ability to secure the right financing. At Qubit Capital, we specialize in guiding startups through the entire capital-raising process. Explore our Fundraising Assistance service to take the next step toward sustained growth.Key Takeaways

-

VC funding fuels high-growth startups with both capital and strategic mentorship.

-

Familiarity with each structured stage of venture capital—from seed rounds to late-stage investments—is crucial.

-

Alternative financing options can be just as effective, depending on a startup’s specific circumstances.

-

Regulatory shifts have historically been major catalysts for growth in the VC market.

-

Founders can better navigate the complex VC landscape by applying actionable strategies grounded in academic research and industry best practices.

Frequently asked Questions

Can startups get debt financing?

Yes, startups can access debt financing, which provides non-dilutive capital to extend their operational runway. This option is particularly viable for businesses demonstrating strong growth metrics and backed by recent equity rounds.